Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineBeyond Brexit: the outlook for UK stocks and the pound

While the coronavirus pandemic has been the dominant story of 2020 for global markets, ever-present in the background for UK investors has been the long and torturous road to Brexit, which is rapidly coming to a head with the UK needing to strike a trade deal with the European Union (EU) before 1 January 2021.

Despite having had more than four years to prepare for a deal, both sides have taken it down to the wire and both still claim the other needs to give ground.

Before we examine the chances of a deal, the implications of no deal and the potential impact of both scenarios on the UK market and the pound, it’s worth recapping the events which brought us to this point and the issues at stake.

A POTTED HISTORY

In a referendum held in June 2016, the majority of those who voted chose to leave the EU, after which began what was meant to be a two-year countdown to the UK leaving the EU.

However, instead of leaving the EU at the end of March 2019, the UK asked for two extensions to Article 50, first until 30 June 2019 and then until 31 October 2019.

A fortnight before the new deadline new prime minister Boris Johnson’s Brexit deal was lost on amendment in the House of Commons and the UK sought yet another extension to Article 50, with the EU agreeing a date of 31 January 2020.

On 23 January 2020, the EU (Withdrawal Agreement) Act received Royal Assent, forming the basis of the legislation for implementing the Withdrawal Agreement negotiated by the UK and the EU. On 31 January 2020 the UK officially left the EU and entered a transition period due to run until the end of this year.

So far so good, until in September this year the UK tabled the Internal Market Bill, giving ministers the power to unilaterally make secondary legislation overriding elements of the Withdrawal Agreement including the Northern Ireland Protocol, which became law on 1 February, thereby breaching its legal obligations with the EU.

BREAKING THE LAW

After four years of trying to reach a Brexit deal, the response from Brussels was understandably terse. ‘This bill is, by its very nature, a breach of the obligation of good faith, laid down in the Withdrawal Agreement. Moreover, if adopted as is, it will be in full contradiction to the protocol on Ireland and Northern Ireland,’ said EU Commission president Ursula von der Leyen.

The UK admitted the Internal Market bill was intended to allow it to override elements of the Withdrawal Agreement, despite there being no such provision in the agreement, claiming in its defence the bill would breach international law only in a ‘very specific and limited way’.

Since then, a game of bluff has developed with the EU launching legal action against the UK for contravening the Withdrawal Agreement and the UK saying it is prepared to abandon trade negotiations and leave on ‘Australia-style’ terms if needs be.

It should be said that while the EU and Australia have been negotiating since July 2018, there is currently no full free trade deal between them and most commerce is done under World Trade Organisation (WTO) rules so an ‘Australia-style’ deal is simply code for no deal.

Factors that could encourage a re-rating of UK equities: the view from investment bank Stifel

Trade deal with the EU: The reaching of a deal would provide clarity for business and could be helpful for the UK stock market.

Vaccine discovery: The development of a viable vaccine could give the UK stock market a boost given that it would hopefully provide a route out of the current stop-go business closure cycle.

The UK is particularly sensitive to sectors including tourism and hospitality which are being badly hit with international travel and other restrictions, so any mean of easing these would be helpful for the economy.

Dividend recovery: The UK market has traditionally had some significant support from yield-seeking investors. An improvement to the corporate background and lifting of dividend suspensions could therefore be helpful for the UK stock market.

IMPACT OF NO DEAL

No deal wouldn’t just impact the trade in goods, it would mean cutting all formal bilateral ties with the EU including areas such as judicial, scientific and energy cooperation. Ironically, the only bilateral agreement left between the UK and the EU would be the Withdrawal Agreement.

WHAT HAPPENS IF THERE IS NO DEAL?

– UK consumers and businesses face higher costs

– The pound could weaken in value

– Inflation could rise

Just days before the prime minister’s self-imposed deadline of 15 October (the date of a summit for EU leaders) to reach a deal, Johnson repeated his threat to walk away if there was ‘no clear progress’. Meanwhile the EU has said progress on key issues was ‘still not sufficient’ for talks to enter the intensive final stage of negotiations.

If a deal can’t be agreed, millions of UK consumers and businesses face higher costs due to trade disruption and the reintroduction of tariffs. Also, as in 2016, the pound would probably slide which will further increase the cost of imported goods and contribute to a rise in inflation at the same time as the economy shrinks.

The only positive sign, if it can be called that, is that the two sides are using similar language, with cabinet minister Michael Gove telling a House of Lords committee that while the UK was keen to do a deal, ‘we will not do a deal at any price’, echoing comments from European Council president Charles Michel that ‘Europe prefers a deal, but not at any cost’.

DICTUM MEUM PACTUM

The Latin phrase ‘dictum meum pactum’ meaning ‘my word is my bond’ isn’t just an old stock market adage, it’s emblazoned on the coat of arms of the London Stock Exchange itself, symbolising the importance of trust in commerce.

By showing its willingness to breach international law, the UK – regarded globally as a strong proponent of the rule of law and the legal order – has raised serious questions about whether it has become an unreliable partner in international negotiations.

Trade negotiations are two-fold – they not only establish the rules governing future commercial relationships between the UK and the 27 EU member states, they also include rules on oversight.

Even if a trade deal can be negotiated, the EU now has reason to doubt that the UK will stick to the rules after implementation if it thinks it can somehow break them in a ‘specific and limited way’.

STATE AID POLICY

A key area where the UK has yet to compromise is the so-called ‘level playing field’ for businesses including setting out its policy on state aid.

Ironically, the UK has always opposed state aid in Europe, yet it now wants to be able to set its own conditions for financial assistance. The EU wants to lock in joint rules to prevent the Government giving UK firms an unfair advantage over their European rivals by moving the goalposts once a deal is agreed.

The view of the US is also crucial, with both Republicans and Democrats criticising the UK for going back on its word, particularly over rules regarding the Northern Ireland Protocol.

Moreover, House speaker Nancy Pelosi has questioned whether UK food and drug standards will meet those of the US and whether the UK Government would seek to manufacture and export a Covid vaccine which, no longer being EU-approved, may not comply with the FDA’s standards.

THE IRISH QUESTION

The position of Northern Ireland in trade talks has been a thorny issue since day one. The Protocol agreed by the UK and the EU as part of the Withdrawal Agreement was meant to avoid the need for any form of checks on goods along the 310-mile physical border between Northern Ireland and the Republic of Ireland, thereby safeguarding the Good Friday Agreement.

However, it still requires Northern Ireland to continue to enforce the EU’s product standards and customs rules. This means safety checks and customs duties will have to be applied to goods brought into Northern Ireland from elsewhere in the UK from 1 January next year which are ‘at risk of subsequently being moved into the EU’, meaning there needs to be a regulatory and customs border in the Irish Sea, despite UK Government assertions to the contrary.

Even if the UK and the EU can negotiate a deal which eliminates tariffs on each other’s goods and keeps checks to a minimum, the Northern Ireland Protocol is still necessary because EU law requires some product-standard checks.

The UK now claims the EU is trying to prevent the movement of goods between Great Britain and Northern Ireland and says it needs a ‘safety net’ to prevent the EU establishing an internal border between them, despite the Protocol ensuring ‘unfettered access’ for goods moving to and from different parts of the UK internal market without border checks.

For Europe, the issue of honouring checks and tariffs as per the agreement is fundamental, while for the UK it is political as it could be fined by the EU or called before the European Court of Justice, whose legitimacy it contests, should the EU decide it is not applying the rules correctly.

THE PRICE OF FISH

Alongside the Northern Ireland issue and state aid, another stumbling block to a trade deal is fish. Despite the relative lack of size and importance of the fishing industry to the UK economy, fishing rights have become one of the sticking points to a wider trade deal.

The issue comes down to whether the EU will give up a sufficient proportion of its quota share to allow the UK to grant a level of access for foreign boats to UK waters and to sign a deal.

‘Conventional wisdom would suggest a split the difference approach could resolve the matter, but that would be to miss the essential point,’ says Barrie Deas, chief executive of the National Federation of Fishermen’s Organisations. ‘The two sides are approaching it from different angles.

‘For the EU this about quantum – how much access their vessels will have to fish in UK waters and how much of their advantage on quota shares can be retained,’ add Deas.

When fishing rights were included in the conditions for the UK joining the ‘common market’ as it was known in the 1970s, the industry was considered ‘expendable’ and the UK agreed quotas based on the number of boats. The Dutch and French promptly expanded their fleets as quickly as possible to ensure as big a quota as possible.

While for the UK a deal is partly about quantum, it’s also about principle and the UK’s ability to act as an independent coastal state after the end of the transition period.

Unlike other aspects of the UK’s exit from the EU, which may not become apparent for years, whether the Brexit deal is a good one or not will become apparent very quickly from 1 January. ‘Fishing has a political immediacy,’ says Deas.

Annual EU revenues from fishing in UK waters are around €650 million, compared with €150 million for UK fishing in UK waters, and observers believe some in Brussels, including the EU’s chief negotiator Michel Barnier, German chancellor Angela Merkel and Dutch prime minister Mark Rutte, are ready to put pressure on France to compromise having enjoyed such an advantage for over 40 years.

A ‘Norway-style’ deal, which sees quotas agreed annually with minor tweaks based on scientific advice and sustainability concerns, is the most hoped-for outcome among UK fishermen and ultimately the most likely model if a deal is going to be struck.

‘It would be crazy for the outside world if the UK and the EU will not be able to come to an agreement. I think it’s in both our interest economically and geopolitically to get to a deal,’ says Rutte.

CITY OF LONDON TO LOSE OUT?

Even with a negotiated deal on the trade of goods between the UK and Europe, trade in services – including financial services – is excluded.

For the City of London this could be a major headache as more than half of the daily volume of shares traded in London is in European companies, a business which is at risk of migrating back to the EU unless a separate deal can be reached.

Of the €12.5 billion of shares which changed hands in London in August, €7.2 billion or 58% was in the shares of EU companies according to Cboe Global Markets. Keeping this business depends on the EU agreeing that UK regulations meet its own standards, a finding known as ‘equivalence’.

Striking an agreement is by no means guaranteed and there is little time left. Last year the EU withdrew equivalence from Switzerland, putting an end to the trading of European stocks on Swiss exchanges.

Alasdair Haynes, chief executive of Aquis Exchange (AQX:AIM), a pan-European share trading platform, is worried about the impact on liquidity: ‘I’m concerned for the industry, it’s bad for the end investor and it will make markets worse.’ Haynes estimates up to a third of trading now going through London could move to Europe, and Aquis has set up a new platform in Paris.

Considering the size and importance of financial services to the UK economy, compared with say fishing, this issue has received very little airplay but it could mean higher costs and less liquidity for investors.

INVESTMENTS TO MAKE OR AVOID IF THERE IS A DEAL

Our sense is that there is a willingness on both sides to ‘get a deal done’ which will satisfy Europe and allow Boris Johnson to appease the Leave contingent with a totemic if economically insignificant win, such as a better deal on fishing.

Karen Ward, chief European market strategist at JPMorgan Asset Management, believes sterling will rally around 5% to $1.35, limited by the fact any deal is likely to be ‘skinny’ and the UK economy will continue to underperform its global peers.

A strong pound would negatively impact the FTSE 100 index, where over 75% of company revenues are generated outside the UK but could be good for the FTSE 250 index whose constituents generate almost 40% of their revenue in the UK.

Investors seeking to position themselves for this outcome could buy Vanguard FTSE 250 ETF (VMID) which has a low 0.1% annual charge to track the performance of the FTSE 250 index. For example, if the index went up by 5% then this ETF should in theory do the same before charges.

At the time of writing, the biggest companies in the FTSE 250 index were cruise ship operator Carnival (CCL), investment trust Pershing Square (PSH) and precision engineer Renishaw (RSW), all of which are predominantly overseas earners or invest in foreign companies.

More relevant to the index from a UK earnings perspective would be stocks such as kitchen seller Howden Joinery (HWDN), insurer Direct Line (DLG) and retailer Games Workshop (GAW).

Investors wanting to back a UK stock rally via actively managed funds should look at Franklin UK Mid Cap (B7BXT54) which has a good track record of outperforming the FTSE index.

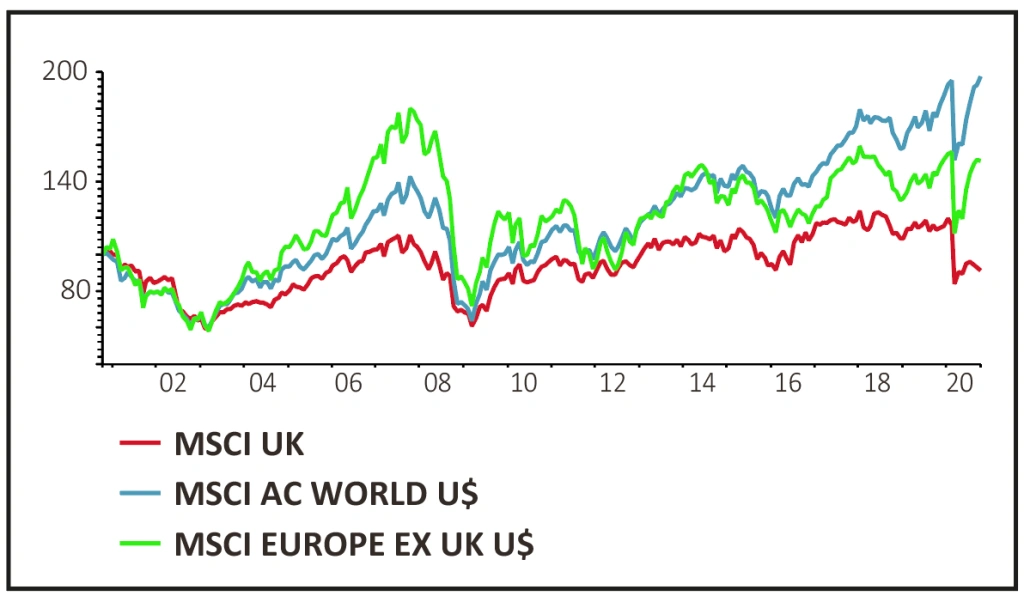

Given how underweight the UK market global investors have been since the referendum, a deal could see a wave of money come into UK stocks. Also, the UK has been one of the worst-performing equity markets this year losing 23% up to the end of September – only emerging markets like Brazil, Russia and Turkey have performed worse – so optically at least it looks cheap.

With more clarity on their trading arrangements, firms which suspended their dividends may feel encouraged to restart them. There may also be a wave of mergers and takeovers as pent-up demand is unleashed.

INVESTMENTS TO MAKE OR AVOID IF THERE IS NO DEAL

If there is no deal, sterling could easily slide up to 10% against major currencies but the reaction of the UK stock indices could be more nuanced.

FTSE 100 stocks with global revenues could increase in price due to the effect of a weak pound on earnings but the hit to the economy – estimated by the Bank of England at 5.5%, with unemployment rising to 7% – would likely weigh on domestic-facing stocks.

Given that approximately three quarters of the FTSE 100 earns money outside the UK, it would be fair to suggest a rally in the index on no deal. If you think no deal is the most likely outcome, buy a FTSE 100 tracker fund such as iShares FTSE 100 ETF GBP Acc (CUKX) which has a 0.07% charge.

On a positive note, UK firms have had several trial runs at Brexit so they should at least be prepared for a worst-case scenario. Also, the UK already trades on WTO rules with the US, China, Russia and Australia so companies are familiar with the process but adding Europe to the list would be a major blow as the zone accounted for 43% of UK exports and 51% of imports last year.

In terms of policy support for the economy, the UK’s public sector debt has already ballooned with short-term cyclical borrowing thanks to Covid and the Treasury will be reluctant to add further to its long-term structural debt.

The Bank of England has sounded out the banks on the potential use of negative interest rates, and it could expand its asset purchase programme which has so far been largely concentrated on the government bond market.

A combination of negative rates and lower yields would be disastrous for earnings in the banking sector and could likely see lending curtailed, including mortgages, which would have a knock-on effect on housebuilders and consumer stocks.

DISCLAIMER: Editor Daniel Coatsworth owns shares in Vanguard FTSE 250 ETF

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Feature

First-time Investor

Great Ideas

- The UK stock market has a new gold giant in town

- More to come from Touchstone despite doubling in price since the summer

- Very large earnings upgrades for Kainos

- Luceco knocks the lights out

- Ford shares start to motor after impressive third quarter trading

- This trust offers big potential if you believe value investing will thrive