Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineThe investment trust that says ditch growth stocks and buy value

Growth has been all the rage with investors for the past decade but there could be change ahead. Henderson European Focus Trust (HEFT) says it is time to sell growth and buy value.

Co-manager John Bennett believes inflation is coming which will drive a contraction of price to earnings (PE) multiples. ‘And when that happens, you’ll want to own a completely different kind of stock, and it is not growth stocks,’ he insists.

Bennett says Henderson European Focus has never positioned itself as either a ‘full fat’ growth or value trust, commenting: ‘We’ve always been a bit of a blend manager. We tilt to growth, or we tilt to value. The clear and increasing tilt from the second quarter of this year was to value and all we’ve done ever since is harden that stance.’

While the fund manager’s latest conviction about the value style has yet to feed through into positive returns this year, the longer track record is encouraging.

SEEKING INFLEXION POINTS

Henderson European Focus has a concentrated portfolio of between 35 and 45 European companies, scouring the continent for inflexion points where companies or sectors are set for a period of growth. The trust has a strong bias towards large cap companies, namely market price tags of €1 billion and above.

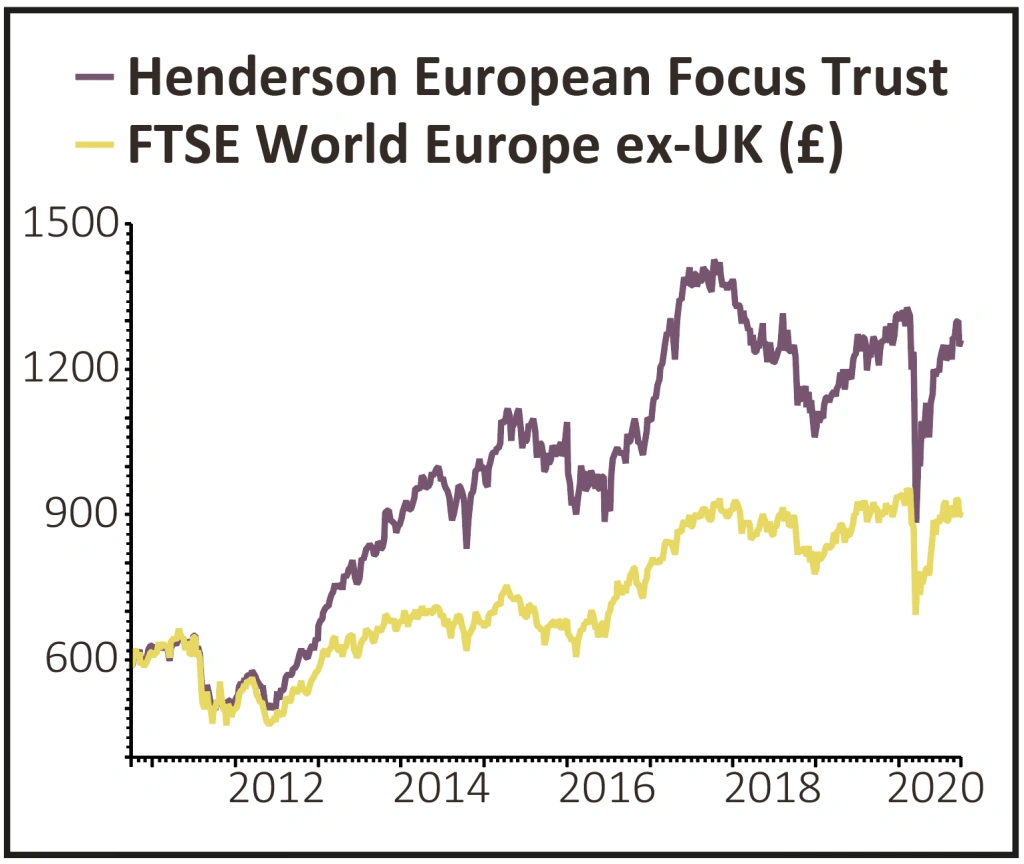

It has comfortably outperformed the FTSE World Europe ex-UK index over the past decade, returning 188.2% versus 119.2% for the benchmark.

It outperformed in seven of the 10 years to the end of 2019, but 2020 has been a tougher period where a 5.8% loss to 30 September compares with a mere 0.5% decline for its benchmark. That’s left the trust trading at a 12.6% discount to net asset, versus a 10.9% average discount over the past 12 months according to Morningstar.

This wider discount does come with some benefits though. It means investors can access a portfolio of household names well below their market value including food giant Nestle, German enterprise tech sector titan SAP, drug maker Roche and paints and coatings maker Akzo Nobel.

PORTFOLIO CHANGES

‘We’ve been selling the winners of the last decade or more to buy the losers,’ says Bennett, ‘but we hope they are the past losers, not the future losers. We’ve bought autos, so our portfolio now owns Daimler and Peugeot – I’ve spent a career avoiding those names, so this is a very fundamental change.’

"We’ve bought autos, so our portfolio now owns Daimler and Peugeot – I’ve spent a career avoiding those names, so this is a very fundamental change"

– John Bennett, Henderson European Focus Trust

The stock picker has sold down consumer staples such as Unilever (ULVR) and Danish brewer Carlsberg, as well as pharmaceutical stocks including Novartis, while also reducing its exposure to the technology sector.

The manager believes this is a ‘game on’ V-shaped recovery in which many European businesses are participating, particularly in sectors such as capital goods. Bennett, who also bought back into European banks in early June, concedes that ‘as we’ve gone more value, we’ve deliberately gone down the quality curve a bit’.

Yet he is adamant Henderson European Focus hasn’t bought hyper-leveraged companies. He says: ‘We’ve bought stuff with strong balance sheets and strong or changing management. That’s why we bought Daimler, that’s why we bought French construction materials group Saint Gobain. I love to invest in management change.’

He highlights the holding in LafargeHolcim, the world’s largest cement maker, where new management have been ‘gripping that big underperforming empire’. He’s convinced they are going to turn it around.

Bennett believes we are living through what will be looked back upon as a seismic shift geopolitically, economically, and for markets and the kind of assets and stocks investors want to own.

‘We’re coming to the end of a 40-year regime in financial markets and we’re coming to the end of the American century and handing over to the Asian and Chinese century, so not tactical but very, very strategic.’

THE INCOME CHALLENGE

Europe hasn’t been able to avoid the wave of dividend cuts and suspensions triggered by the Covid-19 pandemic, but Bennett points out 2.8% yielding Henderson European Focus Trust held the payout for the half year to 31 March at 9.6p, and has ample revenue reserves to ‘tide us over while we await the return of dividend growth to the portfolio’.

At the interim results, chairman Robert Jeens also said the trust was well-placed through its revenue reserves to smooth dividend payments.

However, he added: ‘It will be important to assess the likely longer-term revenue impact of this crisis. The board will consider what final dividend to propose at the end of the year in the light of the relevant evidence available at that time.’

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Editor's View

Feature

First-time Investor

Great Ideas

- Novacyt still looks really cheap despite share price rally

- Panoply busy signing new contracts and buying businesses

- Premier Foods poised for Hovis windfall

- Don’t miss out on this high-quality European growth company

- Take profits on gold miner Centamin

- Shares in AG Barr start to pick up after reassuring results

Investment Trusts

Money Matters

News

- How Trump’s Covid-19 diagnosis has impacted stock markets

- The options for Rolls-Royce shareholders as £2 billion rights issue looms

- What Asda’s sale means for supermarket rivals

- Cineworld faces liquidity crunch as cinemas close again

- Housebuilders rally on Boris Johnson’s bid to help first-time buyers