Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineThe real reason why Fundsmith has done so well

Terry Smith, founder of asset manager Fundsmith, has built an excellent track record since launching the business a decade ago.

According to Morningstar the Fundsmith Equity Fund (B41YBW7) has delivered five-year annualised returns of 20.4% compared with 15.4% for the MSCI ACWI Growth index.

Since inception in 2010 the fund has delivered a compound annual growth rate (CAGR) of 18.3% a year after fees, which means investors have seen the value of their investment go up more than five-fold.

A STRAIGHTFORWARD STRATEGY

Smith has boiled down his investment process to the bare essentials which he eloquently describes in the firm’s owner’s guide. That would get the approval of Albert Einstein who once remarked, ‘if you can’t explain it to a six year old, you don’t understand it yourself’.

Here, we take a closer look at the Fundsmith Equity Fund as it approaches its 10-year anniversary to see how the strong performance has been delivered and highlight some of the key drivers.

While we don’t know the precise purchase and sale prices for the fund’s holdings, the dates when the fund first purchased its holdings are publically available which have been used to estimate which shares may have had the biggest impacts on fund performance since inception.

We only focus on those shares which have been held for at least five years and we have not taken account of any dividend payments.

WHAT IS DRIVING PERFORMANCE?

Some investors may take it for granted that good performance is a direct result of devising a superior investment strategy and executing it well, but that isn’t always the case. Other factors outside the manager’s control can also have an impact.

Fundsmith’s stated goal is to invest in what the managers consider are the best global businesses and hold on to them for a long time and in so doing benefit from a compounding of business value.

The best companies are defined as those which achieve sustainably high returns on operating capital and reinvest earnings in order to grow the business.

Accordingly, the fund’s ‘buy and hold’ strategy is predicated on share prices moving up with rising earnings.

The other driver of share performance is the valuation that investors are willing to pay for future earnings which can move up and down depending on investor mood. The manager says the fund does not explicitly rely on an increase in valuation in its investment decisions.

That’s because Smith believes share valuations matter less than business fundamentals saying: ‘Provided you have the patience, quality stocks do tend to produce the sort of performance over long periods of time that makes their valuation fade into insignificance.’

AMPLIFYING RETURNS

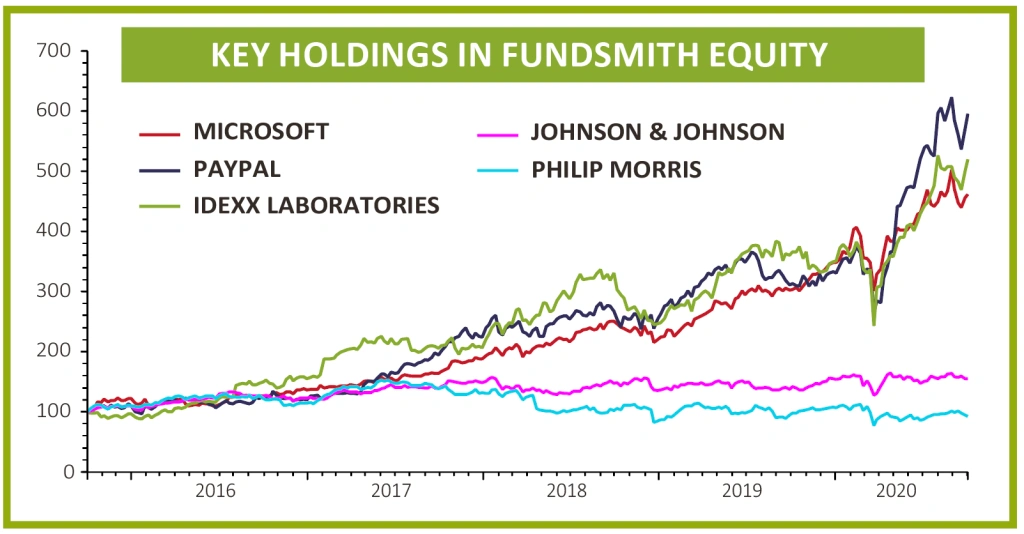

While that’s great in theory, in practice share prices can be driven by sentiment for quite a long period. A good example is Microsoft which has become one of the fund’s largest holdings, driven by strong share price performance.

The shares have risen 11-fold since 2013, when the fund first started buying. This is equivalent to a compound annual growth rate of 39%. A significant part of the return has been down to a re-rating of the shares.

Enterprise value to EBITDA (earnings before interest, tax, depreciation and amortisation) has increased three-fold to 22.3 times from 7.25 times while the PE has increased by 2.6-fold. If the business were valued today at the same PE as 2013 the stock price would be $77 compared with the current price of $206.

Arguably it’s not a concern if some of the stocks the fund owns get driven up by increasing investor sentiment. Focusing purely on fundamentals, the underlying CAGR of earnings at Microsoft has been a very respectable 15% a year, satisfying the manager’s expectations of a high quality growth company.

On the other hand, the performance of Microsoft has probably had a disproportionately positive impact on the fund’s overall performance. A falling PE would damage the fund’s performance irrespective of the fundamentals of Microsoft’s business. Valuation expansion and shrinkage is always at the mercy of febrile investor sentiment.

Another top 10 holding, payments business Paypal has seen its shares rise at a CAGR of 39% a year since the fund first started purchasing shares in July 2015, equating to a five-fold increase. Despite earnings growth of 22% a year the shares have also benefitted from a valuation tailwind, without which the shares would be trading at half current levels.

Diagnostic test instruments company Idexx Laboratories is another fund holding which has seen its share price increase five-fold over the last five years, in part driven by an expansion of the PE multiple that investors have been prepared to pay for the business.

LOW GROWTH STOCKS

These examples illustrate that a re-rating combined with double digit earnings growth can really turbo-charge shareholder returns. Sometimes even low growth is rewarded. Take the fund’s long term holding in Finnish lift company Kone, which has seen earnings growth average a lacklustre 4% a year.

Despite this the shares have seen a big re-rating over the last nine years resulting in the share price going up 3.5-fold.

However this hasn’t been the case in tobacco stock Philip Morris International, first purchased by Fundsmith in 2011. The shares have only delivered a CAGR of 2% a year.

The main reason for the lacklustre performance is because the price to earnings ratio is virtually unchanged over the last nine years, which means the value of the fund’s holding has grown in line with the growth in earnings.

RECURRING THEME

These examples illustrate a recurring theme played out across markets since the financial crisis of 2008, with investors paying up for earnings growth and quality shares which are seen as relatively resilient.

A good example of a low growth, but high quality share which has re-rated is healthcare stock Johnson & Johnson which the fund first purchased in May 2014. The shares have since gone up around 43% which is equivalent to a CAGR of 6% a year.

However, without the benefit of a re-rating the shares would only have delivered a return of 14%, or a CAGR of 2% a year, the same underlying growth in earnings for the company.

Factors outside the manager’s control have so far had a net positive impact, but that doesn’t mean it will remain or recur in future periods.

PORTFOLIO CONCENTRATION

The fund manager isn’t fixated on benchmarks when building the portfolio which means it can end up highly concentrated in certain markets or sectors. That said 29 holdings are generally accepted as sufficient to achieve the benefits of diversification.

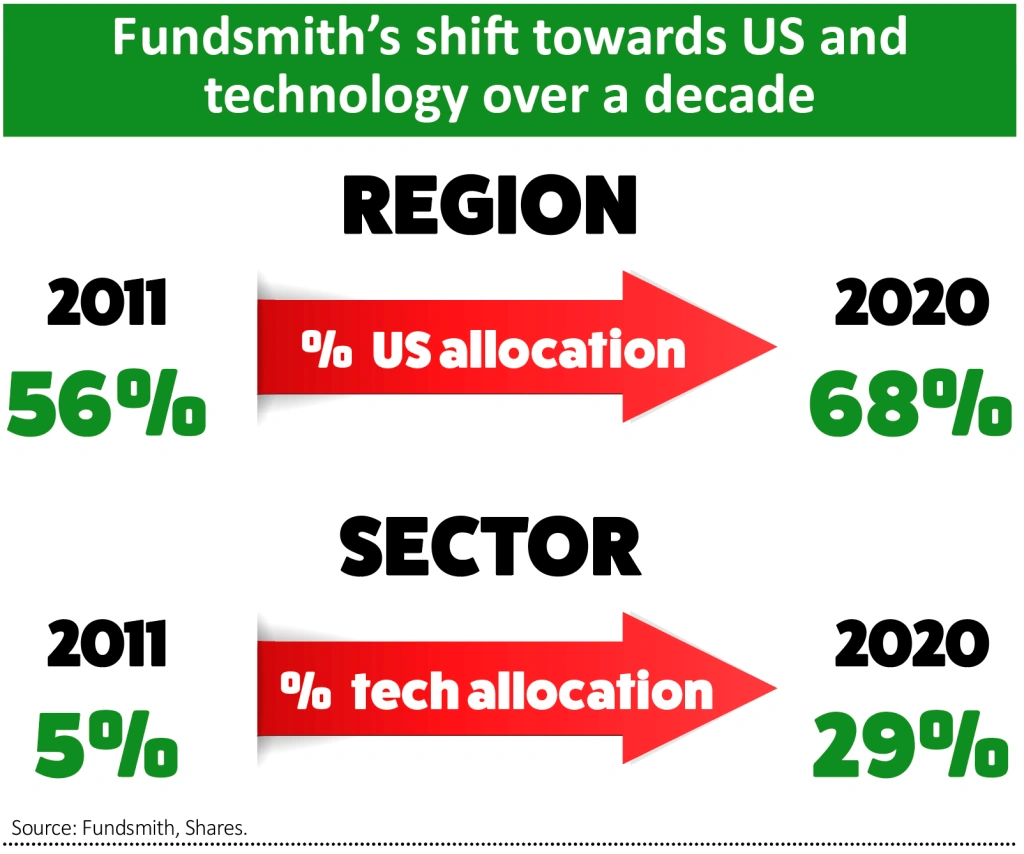

Around two thirds of the portfolio is exposed to US firms and 30% is invested in the technology sector. This is quite a change from just after inception when only 56% was invested in US shares and technology was a mere 5% of the fund.

Strong performance of US markets and technology in particular has been a factor in the changing composition of the fund.

DISCLAIMER: Editor Daniel Coatsworth has a personal investment in Fundsmith Equity

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Editor's View

Feature

First-time Investor

Great Ideas

- Novacyt still looks really cheap despite share price rally

- Panoply busy signing new contracts and buying businesses

- Premier Foods poised for Hovis windfall

- Don’t miss out on this high-quality European growth company

- Take profits on gold miner Centamin

- Shares in AG Barr start to pick up after reassuring results

Investment Trusts

Money Matters

News

- How Trump’s Covid-19 diagnosis has impacted stock markets

- The options for Rolls-Royce shareholders as £2 billion rights issue looms

- What Asda’s sale means for supermarket rivals

- Cineworld faces liquidity crunch as cinemas close again

- Housebuilders rally on Boris Johnson’s bid to help first-time buyers