Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazinePredictions for a FTSE 100 earnings rebound look shaky

No-one can agree upon the origins of the quote, ‘hope is not a strategy’. This column cannot be sure and a trawl of the internet sees commentators attribute to everyone from former US president Barack Obama to film director James Cameron to former New York City mayor Rudi Giuliani to one-time Green Bay Packers American football coach Vince Lombardi.

One thing is certain however – hope is not a strategy when it comes to investment. Any selection should be made with downside protection in mind first, followed by a clear assessment of potential returns, with a set price target or overall gain, to ensure that possible rewards more than compensate for the possible dangers.

At the moment, it seems as if fears of an extended economic downturn thanks to a prolonged pandemic are being offset by investors’ hopes for more fiscal and monetary stimulus, which they feel in turn will stoke a sharp recovery in profits, dividends and – presumably share prices and asset valuations – in 2021 and beyond.

This scenario could yet pan out and it is unlikely that central banks and governments will stop running quantitative easing schemes, racking up budget deficits or even experimenting with new ideas such as Modern Monetary Theory or Universal Basic Income if the economic outlook becomes any more uncertain.

They do seem to be underpinning hopes for a rapid recovery in UK plc’s earnings power, at least if trends in FTSE 100 earnings forecasts are any guide.

Trio of tests

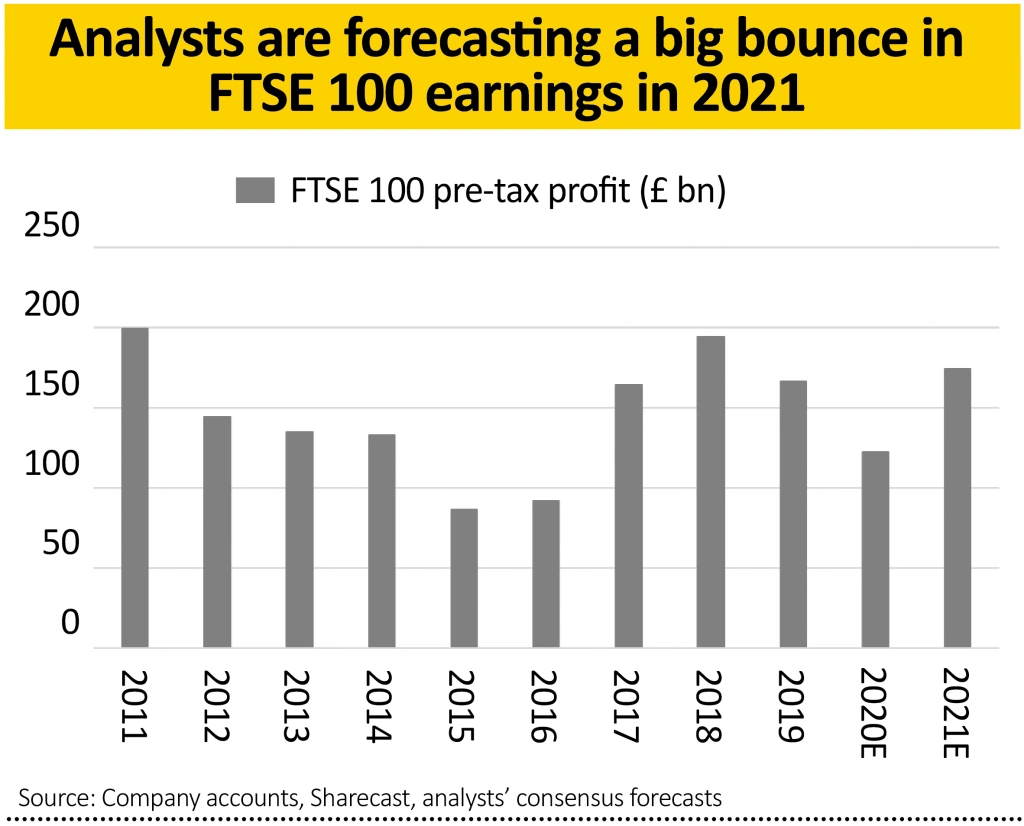

Taking an aggregate of the bottom-up forecasts for all 100 members of the UK’s premier index, analysts are currently expecting a sharp rebound in pre-tax profit to £174.2 billion in 2021, from 2020’s £122.2 billion.

To test the reliability of such an estimate – and whether it is a safe assumption upon which to base an assessment of the valuation of the UK market (since the FTSE 100 represents over 80% of its market cap and earnings power) – investors can look at three barometers.

The first is how the 2021 forecast compares to recent history.

An outcome of £174.2 billion in 2021 would take next year’s pre-tax profit total for the FTSE 100 to a level 5% above that of 2019 and one just 10% below 2018’s all-time high. Investors must weigh the effects of the pandemic, the efficacy of policy response and how corporate and consumer behaviour may (or may not) change as part of their analysis here.

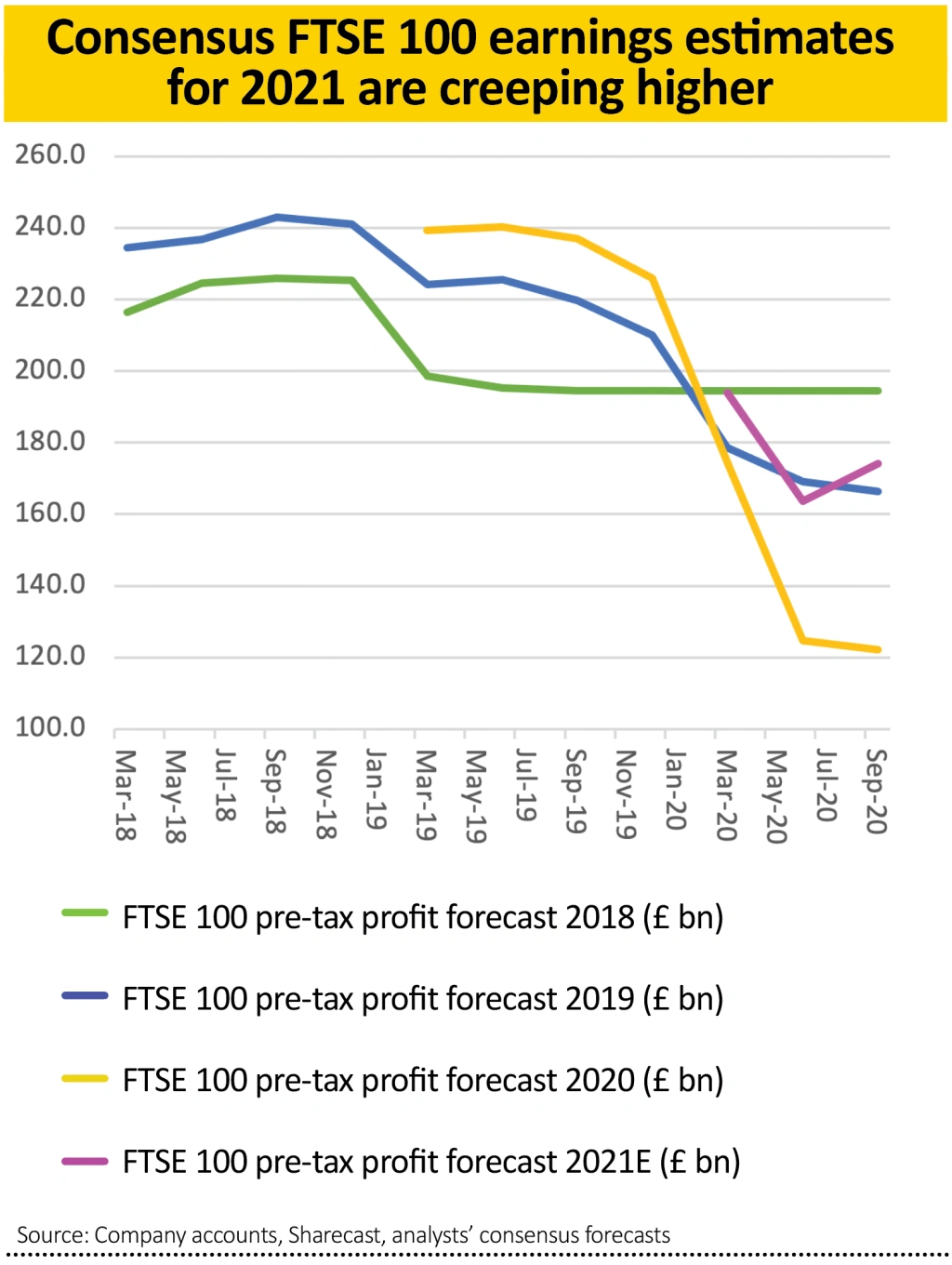

The second is to gauge analysts’ confidence in their own forecasts. This can be done by tracking momentum in the estimated aggregate profit totals.

The bad news is that estimates for 2020 are still sliding lower, as the pandemic refuses to go away and the Government juggles policies designed to protect the public’s physical health with the need to manage its financial health.

The good news is that estimates for 2021 have started to creep higher. A 6% upgrade in analysts’ earnings forecasts since July offers some encouragement.

The third is to look at the mix of the earnings recovery, by sector and stock.

In terms of sectors, oil and gas is expected to generate nearly a third of the FTSE 100’s £52 billion jump in pre-tax profits on its own. Another quarter of the increase is seen coming from financials (banks and insurers) and another quarter from consumer discretionary and industrial stocks.

This picture is confirmed by the company-by-company breakdown of forecast FTSE 100 profit growth. BP (BP.) and Shell (RDSB) top the list, with four banks also in the top 10, alongside two miners – Glencore (GLEN) and Anglo American (AAL) – as well as British Airways owner International Consolidated Airlines (IAG) and aerospace supplier Rolls-Royce (RR.).

It seems fair to say this is a high-octane mix. If there is a strong global economic recovery, thanks to a vaccine, fiscal and monetary stimulus or the virus simply becoming less potent, then the UK could well be a very interesting place to invest. Consensus forecasts put the FTSE 100 on 13.6 times earnings for 2020 with a prospective yield of 4.2% and sentiment on cyclicals – and especially oils and banks – is washed out.

If the opposite happens, and the pandemic lingers and drags the economy down, it would be unwise to put too much faith in forecasts of a rip-roaring earnings recovery, or that 4.2% dividend yield for that matter (although that still comes in at 3.7% if you assume the banks pay nothing again, thanks to regulatory or economic pressures).

The drive away from hydrocarbons and toward renewable energy could also hold back BP and Shell, and thus the FTSE 100, in the near term.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Editor's View

Feature

First-time Investor

Great Ideas

- Novacyt still looks really cheap despite share price rally

- Panoply busy signing new contracts and buying businesses

- Premier Foods poised for Hovis windfall

- Don’t miss out on this high-quality European growth company

- Take profits on gold miner Centamin

- Shares in AG Barr start to pick up after reassuring results

Investment Trusts

Money Matters

News

- How Trump’s Covid-19 diagnosis has impacted stock markets

- The options for Rolls-Royce shareholders as £2 billion rights issue looms

- What Asda’s sale means for supermarket rivals

- Cineworld faces liquidity crunch as cinemas close again

- Housebuilders rally on Boris Johnson’s bid to help first-time buyers