Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

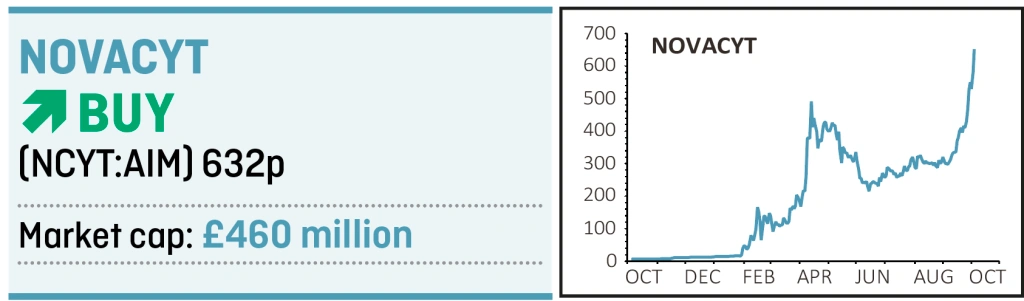

magazineNovacyt still looks really cheap despite share price rally

There aren’t too many firms which have delivered a 10-fold increase in first-half revenues to €72.4 million and a 13-fold increase in gross profits to €60.3 million in 2020, all from organic sources. This makes diagnostics firm Novacyt (NCYT:AIM) pretty unique.

But the excitement has arguably only just begun with the latest contract win (29 Sep) to supply the Department for Health and Social Care (DHSC) potentially worth £250 million for phase one over the next six months and phase two worth considerably more.

Unsurprisingly the shares have been on a tear, recently hitting a new all-time high of 652p, and the shares are up 90-fold over the last year. However, even before the latest contract win the company indicated that full-year revenue and EBITDA (earnings before interest, taxes, depreciation and amortisation) would exceed €150 million and €100 million respectively.

Given the year-end is only three months away the stock is on a cheap 4.5 times EV/EBITDA. We believe this is a great opportunity to get on board an exciting growth business.

It isn’t without risks given the early stage nature of the company and lack of broker coverage, meaning there are no earnings estimates in the market.

And prospective investors should be aware that the current boom for Covid-19 testing may well peak at some point over the next year and a half, creating a cliff for Novacyt’s earnings. Therefore this may be a stock to own short-term rather for years to come, unless it can successfully diversify its source of earnings.

Novacyt development timeline

In response to the Covid-19 emergency, Novacyt made the strategic decision to develop a diagnostic test in early January 2020.

The company launched the test in late January 2020 and subsequently received clinical use approval from a number of leading global regulatory authorities, including CE Mark accreditation and Emergency Use Authorisation (EUA) from the US Food and Drug Administration (FDA) and the World Health Organisation (WHO).

This rapid development of a test for Covid-19 positioned Novacyt at the forefront of the global response to the spread of the virus.

This included increasing the company’s own production capacity at its wholly-owned Primerdesign site in Southampton, as well as entering into contract manufacturing partnerships.

The firm also beefed up its supply chain capacity by expanding the key raw material supplier base to develop a long-term and sustainable high volume supply of its tests.

The company operates from three manufacturing sites occupying 40,000 square feet.

In July 2020, Queen Mary University of London announced the initiation of a 2,000-patient clinical trial using Novacyt’s innovative near-patient testing system, which can deliver a result within an hour.

New Strategy

Management is aware of the need to offset future reductions in Covid-related revenues and recently presented a clear and ambitious new strategy.

Novacyt aims to leverage its reputation, market intelligence and relationships developed during the Covid-19 response to commercialise new products. It wants to expand its presence in respiratory and transplant clinical diagnostics to become a leader in the field.

The company will supplement its product portfolio and expand capabilities through selective and earnings-accretive mergers and acquisitions.

In the short-term it is looking for strategic targets which will increase the vertical integration of the group. Longer-term the focus will shift to bigger opportunities to deliver revenues and profitability in key infrastructure markets.

Organically the firm will build its own direct sales force in the EU and US while continuing to develop its successful distributor and partnership sales model in the rest of the world.

Market opportunity

The market for in-vitro diagnostics (blood-based samples used to provide diagnosis or treatment monitoring) is growing at around 5% annually and is expected to be worth $110 billion by 2030 according to some forecasts.

The growth is underpinned by an ageing world population and an expected increase in the incidence of chronic and infectious diseases.

The company believes that one of the lessons learned from the pandemic is that it exposed the limitations of relying on closed systems with few suppliers providing testing equipment. Increasing use of open systems and multiple suppliers will play into the hands of the partner network that Novacyt has created.

With the launch of Novacyt’s near-patient testing system in July 2020, the company looks well positioned to address this drive towards rapid, decentralised testing.

Financial overview

There aren’t any broker estimates available but we do know that revenue growth has been strong and June sales amounted to €25.4 million, around a third of first-half sales. It’s likely that management guidance of at least €150 million for the full year is very conservative before taking account of the DHSC order.

Net cash generation in the first-half was strong reaching €24.6 million, allowing the company to repay a €5 million bond subscribed by Harbert European Growth Capital. It also converted a Vatel €4 million bond into equity.

The company was debt free as of 30 June with cash in hand of €19.7 million compared with €1.8 million in December 2019.

We acknowledge that the shares have already gone up by a large amount. However, the DHSC order on 29 September represents a significant change in the company’s fortunes.

So many small caps claim they are going places but often disappoint. In contrast, Novacyt is actually achieving tremendous sales numbers meaning the market excitement is justified. It’s in a sweet spot and investors should get on board now.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Editor's View

Feature

First-time Investor

Great Ideas

- Novacyt still looks really cheap despite share price rally

- Panoply busy signing new contracts and buying businesses

- Premier Foods poised for Hovis windfall

- Don’t miss out on this high-quality European growth company

- Take profits on gold miner Centamin

- Shares in AG Barr start to pick up after reassuring results

Investment Trusts

Money Matters

News

- How Trump’s Covid-19 diagnosis has impacted stock markets

- The options for Rolls-Royce shareholders as £2 billion rights issue looms

- What Asda’s sale means for supermarket rivals

- Cineworld faces liquidity crunch as cinemas close again

- Housebuilders rally on Boris Johnson’s bid to help first-time buyers