Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineLow growth, recovery or second wave: the investments to own in each scenario

We see three different scenarios for markets going into 2021 and inflation will play a key role.

First is strong economic recovery with rising inflation and this scenario favours cyclical stocks. For example, this might be commodity producers who would sell their metals for higher prices. Banks would be another beneficiary as rising inflation can drive up loan rates and demand for credit may also increase if the cost of living goes up.

Second is a weak growth environment with low inflation, which would favour quality companies that can deliver growth. This has been the winning trade for many years and investors would have to be prepared to pay high ratings to own growing businesses.

Third is a severe second wave of coronavirus which is when you want to own gold. A heightened level of infections and deaths would cause upset among the markets and investors would probably flock to safe-havens, with gold being a natural place to park money in times of trouble.

Inflation matters

Inflation has a major influence on financial markets. It affects all aspects of the economy, from consumer spending, business investment and employment rates to government programs, tax policies and interest rates.

Having collapsed in March at the height of the coronavirus pandemic as lockdowns and travel bans came into force around the world, five-year forward inflation expectations in the US have since picked up again and are almost near all-time highs according to Federal Reserve Economic Data (FRED).

US inflation is seen as the world’s most important economic variable, given the American economy is the largest of them all and the country’s central bank, the Federal Reserve, tends to set the tone for other major central banks around the world when it comes to monetary policy.

We’ll now go into each scenario in more detail.

SCENARIO 1: STRONG ECONOMIC RECOVERY, RISING INFLATION

Analysts at Morgan Stanley believe inflation is back, and on a global level they think the world economy is reflating quicker than anticipated. They see a synchronised global economic recovery from the second quarter of 2021 onwards.

This view is shared by BlackRock, which thinks the likelihood of higher inflation is not yet reflected in market prices, opening a window of opportunity for long-term investors. But they warn that once higher inflation appears, it’s likely to be too late for investors to react – markets will have already moved to price in higher inflation expectations.

SWITCH TO CYCLICAL STOCKS

Investments that would do well in this scenario are cyclical stocks, like mining and construction companies, as well as financial stocks and emerging market stocks – all of which, in relative terms, have struggled in recent years.

In the investing world, cyclical stocks are those whose fortunes swing depending on the business cycle of an economy. A cyclical stock typically goes up in the boom years of the economy and down when the economy is lower.

DEPENDENT ON VACCINE

It’s important to note the scenario of strong economic growth and higher inflation assumes coronavirus vaccines are successfully developed and made broadly available within the first three months of next year.

But various high-profile figures in the medical community have warned the public, and indeed governments, against seeing a vaccine as a panacea.

They argue that some of the experimental approaches being taken in developing a coronavirus vaccine have never been mass produced before. There are also questions about the length of immunity to Covid-19 after being vaccinated and the preparedness of supply chains to mass manufacture and distribute enough vaccines at the scale and speed required.

FORCES AT PLAY

In BlackRock’s view, there are some significant forces at play. Firstly, due to the Covid-19 fallout higher global production costs are likely.

Deglobalisation and the remapping of supply chains will be accelerated by the post Covid-19 desire to achieve greater resilience against a range of potential shocks, it says, adding that reduced global competition in economies may embolden companies to hike prices when domestic cyclical pressures rise.

Selected large companies have more pricing power than ever to pass higher labour costs on to customers.

Secondly, major central banks are evolving their policy frameworks and explicitly intend to let inflation overshoot their targets.

BAD FOR GROWTH STOCKS

According to AJ Bell investment director Russ Mould, a strong recovery with this type of rising inflationary environment would be bad for growth stocks, such as all the tech names which have soared this year.

This is because a lot of growth stocks trade on a big premium to wider markets as growth is seen to be scarce.

Mould explains: ‘In an inflationary recovery growth wouldn’t be scarce at all, you’d be able to pick it up in the street. You’d get it from cyclicals, financials and emerging markets, all of which are bombed-out, having performed badly, and all of which are in the value bucket.

‘They’re all a lot cheaper and therefore if you got a strong inflationary recovery, it would potentially be the catalyst for value after a decade or more in the doghouse.’

Here are two stocks worth buying if you think this scenario will happen.

INVESTMENTS TO MAKE IN THIS SCENARIO

CRH (CRH) £27.97

Construction materials group CRH (CRH) has a measure of insulation from fluctuations in the economy thanks to its diversification and exposure to infrastructure spending – with governments likely to spend big in this area to help kick-start the recovery from Covid-19.

That said, construction in the round remains a highly cyclical sector and a material rebound in the economic outlook would substantially improve the prospects of CRH after it saw revenue dip 3% in the first half of 2020 to €10.9 billion.

As it currently stands, CRH is forecast to see pre-tax profit drop to €1.78 billion this year before bouncing back to €2.1 billion in 2021 – in line with 2019’s result. For 2022, analysts forecast €2.4 billion pre-tax profit. A pick-up in economic activity could easily result in these forecasts being lifted.

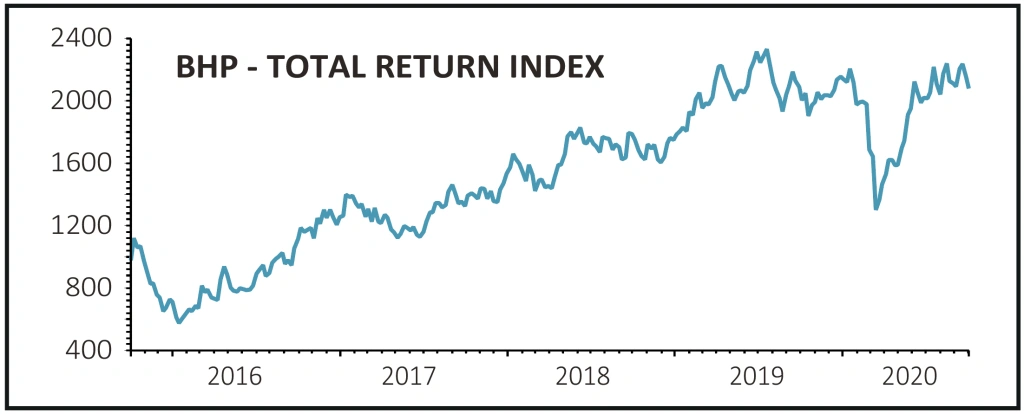

BHP (BHP) £16.45

According to Morgan Stanley, metal prices could rise in the 12 months following an increase in inflation expectations, potentially by as much as 50%.

An increase commodity prices would be good for miners, particularly the big diversified ones which dig lots of different metals out of the ground.

Among the major diversified miners on the London market, BHP (BHP) stands out due to its attractive commodity mix.

The miner produces copper and iron ore – two metals which typically do well in a strong economic recovery – and it also has big exposure to nickel, a metal set to be increasingly important in the electric vehicle revolution.

Unlike Rio Tinto (RIO) and Anglo American (AAL), BHP has no exposure to the diamond market, which is in structural decline and has been significantly affected by the pandemic.

SCENARIO 2: WEAK ECONOMIC RECOVERY, LOW INFLATION

The second scenario is that we see weak economic activity with low levels of growth and little inflation, something it is argued we’ve had for the last 10 years anyway.

This scenario would benefit growth stocks, many of which have done well as the coronavirus pandemic accelerated certain trends.

Working from home and the faster shift to online shopping have benefitted the big tech firms and online retailers.

Healthcare stocks have also outperformed. Having been out of favour with investors for the last few years they’ve become hot property with some remarkable share price performances since the pandemic started.

For example, respiratory drug development company Synairgen (SNG:AIM) soared as much as 430% a single day following a major breakthrough in treating hospitalised coronavirus patients.

The share price rally of such stocks is getting increasingly harder to justify, particularly as the underlying landscape in the sector has become a lot more competitive, which raises the risk that perceived financial benefits could quickly disappear if another firm finds a better or cheaper solution.

But on a broad sector basis some analysts see growth stocks continuing to do well, as guidance from the major central banks for low interest rates to continue for the foreseeable future continues to push investors towards growth companies.

WHY GROWTH STOCKS?

Growth stocks have typically done well in a low interest rate environment compared to value stocks.

Investors have been happy to pay any price to own a company that is growing its earnings, as that should also fuel the share price.

Central banks are currently looking to keep rates low because in theory the lower the interest rate, the more willing people are to borrow money to make big purchases, such as houses or cars. It is hoped this will create a ripple effect of increased spending throughout the economy.

WHAT ABOUT BONDS?

Along with growth stocks, bonds are the other asset class seen to do well in a weak economic recovery where interest rates are low and there’s little sign of inflation picking up.

Morningstar investment analyst Nicolo Bragazza says this is because it comes down to duration, both for growth stocks and bonds.

Bragazza explains: ‘Academic studies show there are shorter duration and longer duration stocks, value being shorter duration and growth longer duration.

‘Value stocks, which tend to be companies in traditional sectors, have cash flows and pay dividends and their benefit for investors is short-term, but for growth stocks investors rely on the future prospects and the benefit of big cash flows in the future.’

He adds: ‘There is a unifying view with bonds. A weak economic environment where interest rates are low is positive for longer term bonds and long duration stocks. But shorter duration bonds, like shorter duration value stocks, have underperformed.’

But Bragazza also points out there is a distinction in corporate bonds between investment grade bonds and junk or high yield bonds, with high quality bonds more likely to do well in a weak environment as those with a lower rating are more sensitive to economic activity.

Here are our two investment ideas if you think we’re in for weak economic recovery with little inflation.

INVESTMENTS TO MAKE IN THIS SCENARIO

AstraZeneca (AZN) £85.10

Pharmaceutical giant AstraZeneca (AZN) has built a strong cancer drug franchise over the last few years and offers investors a robust growth outlook supported by a healthy pipeline of new drugs.

In addition, any positive news flow in relation to its Covid-19 vaccine candidate in collaboration with the University of Oxford should have a major influence on the share price. The European Medical Agency (EMA) has just started a review with the aim to speed up any future approval process.

Near-term earnings momentum and an amply covered 2.6% dividend yield should remain attractive in a low growth, zero interest rate environment. The shares are not expensive on a price to earnings ratio of 19.6 for 2021 and 16.3 for 2022.

Henderson Diversified Income Trust (HDIV) 88p

If economic growth becomes anaemic and interest rates remain at historically low levels for an extended period, investors are likely to favour resilient businesses which have strong balance sheets. There are plenty of equity funds to choose from that focus on quality investments, but in the bond fund world they are relatively scarce.

Among the bond fund names that do have a quality focus is the £165 million Henderson Diversified Income Trust (HDIV), managed by industry veteran John Pattullo and Jenna Barnard. It has a policy of lending to good quality businesses and a tight focus on strong free cash flow generation.

This strategy allows the fund to provide relatively safe income with a current yield of 5.1%. The fund has net gearing of 15%, ongoing management charges are 0.9% and it is trading on a 4% discount to net asset value.

SCENARIO 3: SEVERE SECOND WAVE OF CORONAVIRUS

The third scenario is a severe second wave of coronavirus cases, with the ensuing hit to the economy and further stimulus from governments and central banks to try to steady the ship.

In this scenario it’s also likely there would also be a further debasement of paper currency, as one of the impacts of measures like quantitative easing is that it can devalue the country’s domestic currency.

The expectation is that this would be beneficial for gold, which historically has done well in such scenarios and among other things is seen as a hedge against currency debasement.

Gold is typically viewed as one of the ultimate safe-haven assets because it is one of the very few assets which acts as a true store of value and has maintained its purchasing power over the years.

For example, if you put a stash of 500,000 Italian lira and a one ounce gold coin in your attic in 1990, and then found it 30 years later, that wad of lira would now be worthless but the gold coin – which back then would’ve been worth just under $400 – would’ve grown in value almost five-fold and now be worth $1,900.

HANG ON A MINUTE

However, Michel Perera, chief investment officer at Canaccord Genuity Wealth Management, points out that gold has been ‘behaving erratically’ this year and won’t immediately correlate in the way people expect.

He explains: ‘Gold is behaving a little like a risk-on asset at the moment, not risk-off. It’s correlating a lot more with oil, copper and equities, and I’m not sure gold will react as expected (in another downturn). It will eventually fall in line, but it won’t do it immediately.’

Perera also thinks growth stocks will continue to outperform in this scenario, as the trends we’ve adopted over the past few months – working from home, more video calls via a computer, higher spending with regards to our health – are likely to continue, again benefitting the tech and healthcare names which have done well in the year to date.

GOLD MINERS

If gold does eventually perform as expected in the event that a severe second wave of coronavirus cases causes another big hit to the economy, then gold miners – a leveraged play on the gold price – should do well.

But in this case, picking the right gold miner is crucial as any operational issues or setbacks could hold them back from joining in the wider rally.

As well as our suggestion for a gold mining stock to buy if you believe there will be a severe second wave of coronavirus, we also suggest a financial trading platform provider which could do well if markets become really choppy again. Read on to get the details.

INVESTMENTS TO MAKE IN THIS SCENARIO

Hummingbird Resources (HUM:AIM) 37.9p

Like most gold miners, Hummingbird Resources (HUM:AIM) has had a good 2020 as reflected in its share price, yet it still trades on less than five times forecast earnings and has a more than reasonable price to book value of 1.14 times, according to Stockopedia.

The firm has paid down a chunk of its debt and reiterated its commitment to having no borrowings by July 2021.

Analysts appear to be excited by the company and Canaccord Genuity’s Sam Catalano says that the Kouroussa gold project it recently bought could help generate further value for shareholders with the potential to double Hummingbird’s production output.

A key risk to the share price is that one of its mines is in Mali, where there has recently been unrest, but political risk comes with the territory of investing in any mining stock.

Plus500 (PLUS) £15.32

Heightened market volatility earlier this year was music to the ears of Plus500 as more people tried their hand at trading stocks.

Plus500 advertised heavily to make sure its name was in front of people looking to take advantage of big swings in the market. This strategy worked, leading analysts to upgrade earnings forecasts several times in 2020.

Its shares have risen 76% year to date and the company has delivered a stream of good news.

Another market wobble caused by Covid-19 becoming more severe would be a tailwind for Plus500. As such, we believe this stock would significantly outperform the market in the event of a bad second wave.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Editor's View

Feature

First-time Investor

Great Ideas

- Novacyt still looks really cheap despite share price rally

- Panoply busy signing new contracts and buying businesses

- Premier Foods poised for Hovis windfall

- Don’t miss out on this high-quality European growth company

- Take profits on gold miner Centamin

- Shares in AG Barr start to pick up after reassuring results

Investment Trusts

Money Matters

News

- How Trump’s Covid-19 diagnosis has impacted stock markets

- The options for Rolls-Royce shareholders as £2 billion rights issue looms

- What Asda’s sale means for supermarket rivals

- Cineworld faces liquidity crunch as cinemas close again

- Housebuilders rally on Boris Johnson’s bid to help first-time buyers