Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineNew-look Witan moves away from cyclical firms

After enduring a tough period through the Covid-19 crisis, investment trust Witan (WTAN) has rung the changes.

At first glance it looks like the trust has moved away from value investing and towards growth. We talked to investment director James Hart to discuss why this isn’t necessarily the case.

MULTI-MANAGER STRATEGY

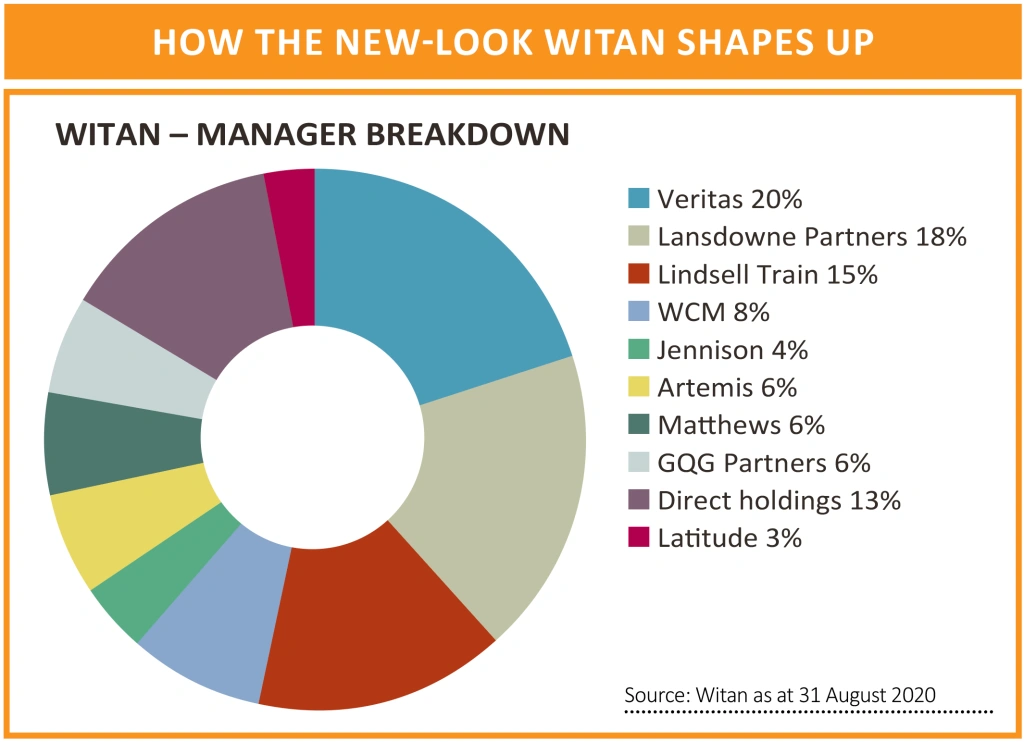

Witan’s investment strategy involves the use of a panel of third-party managers, as well as running a small part of the portfolio itself.

It adopted a ‘new and simpler benchmark’ from the start of 2020, with a lower UK weighting (19%, down from 30%) and a higher footprint in the US (46%, up from 25%).

But as a legacy from its previous benchmark, at the beginning of the year its portfolio was heavily biased to the UK and Europe and under-allocated to the US.

Witan took a decision, which with the benefit of hindsight turned out to be a bad move, of only gradually aligning manager allocations to reflect the global structure of the new benchmark.

This was based on last December’s definitive election result in the UK and an apparently improved picture for economic growth outside of the US.

In the trust’s own words this ‘proved costly’, with markets in the UK (-19% to the end of May) and Europe (-7%) performing much worse than the US (+2%). The substantial overperformance of the US reflected its heavy allocation to technology – perceived widely as a coronavirus winner as reliance on the internet in all sorts of areas increased.

RESHAPING THE PORTFOLIO

Stocks from Witan’s Europe ex-UK mandates run by Crux Asset Management and SW Mitchell were eventually sold by June. Witan also offloaded a holding in the global systematic value portfolio managed by Pzena, with the proceeds initially held in a US equity index ETF.

On 4 September the trust appointed WCM Investment Management and Jennison Associates as its new global growth managers. Both specialise in faster growing companies.

WCM, located in Laguna Beach, California, has been allocated $200 million to manage, or 8% of Witan’s assets, while New York-based Jennison has been allocated $100 million, or 4%. The move was funded by selling the aforementioned US equity index ETF.

Hart tells Shares the changes don’t so much represent a move away from value as they do from cyclical to non-cyclical stocks. Though as he admits ‘there is definitely crossover between cyclical stocks and value’.

He adds: ‘Those companies which are more cyclical tend to be at the value end of the spectrum because of the fragility of the economic recovery all the way back to the global financial crisis.’

A MOVE TO ‘A-CYCLICAL’ BUSINESSES

Hart explains that the trust is moving towards what he describes as ‘a-cyclical’ companies which are set to grow their earnings over time regardless of the sector they are in.

‘This is a recognition that life is becoming increasingly difficult for managers whose structural process always takes them towards deep value companies.

‘Often these companies operate in sectors at risk of disruption whether for technological reasons or due to regulation or because of an increased focus on ESG (environmental, social, governance) factors.’

Hart cites the examples of fossil fuel and tobacco stocks and adds he would expect the managers appointed by Witan to have low exposure to these areas.

One danger of moving towards growth companies is that valuations have become more stretched and Hart admits he and the team are cognisant of this risk.

For this reason, the allocation to WCM and Jennison, at 8% or 4% respectively, is lower than Witan would typically employ with a new manager. Hart says this leaves room to add positions over time – potentially when valuations are less stretched.

JUDGING PERFORMANCE OVER THE LONG TERM

Stifel analyst Ian Scoulter says: ‘The Witan team has explained clearly what the problems have been, and we hope that the changes in the managers employed by the trust start to deliver better performance over the next six months. To narrow the discount (it trades at 8.4% below net asset value), we think Witan will need to deliver better performance in order to get more investors on board.’

The market remains sceptical as the discount to NAV has widened since the latest manager changes were announced.

Not unfairly Hart expects to judge the managers Witan employs over a longer timeframe of five to 10 years – noting that it will typically have around 10 managers on the roster and change around one a year.

In Shares’ view the same logic should be applied to Witan itself and although we are somewhat wary of the decision to chase growth this remains a well-balanced portfolio, it charges a reasonable fee of 0.79% and is a good option for genuinely long-term investors.

As Hart observes: ‘We had an awful couple of months but are hopeful that won’t be repeated, and we are now looking to rebuild.’

WITAN: JAMES HART’S VIEW ON SOME OF ITS MANAGERS

Veritas: ‘Essentially this team looks for growth at a reasonable price.’

Lansdowne Partners: ‘Flexible, they include some cyclical value on the basis that in a return to normality there will be out-sized returns on the way up for these stocks.’

Lindsell Train: ‘Targets rare and beautiful brands.’

WCM: ‘Buys and holds companies with strong corporate culture and increasing competitive advantages.’

Jennison: ‘Focuses more on disruptive and innovative businesses with exceptional growth rates.’

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.