Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineCan Ashtead maintain its stellar growth record?

In any table of UK ‘quality growth’ companies or ‘compounders’, equipment hire firm Ashtead (AHT) is usually somewhere near the top if not the top-ranked stock.

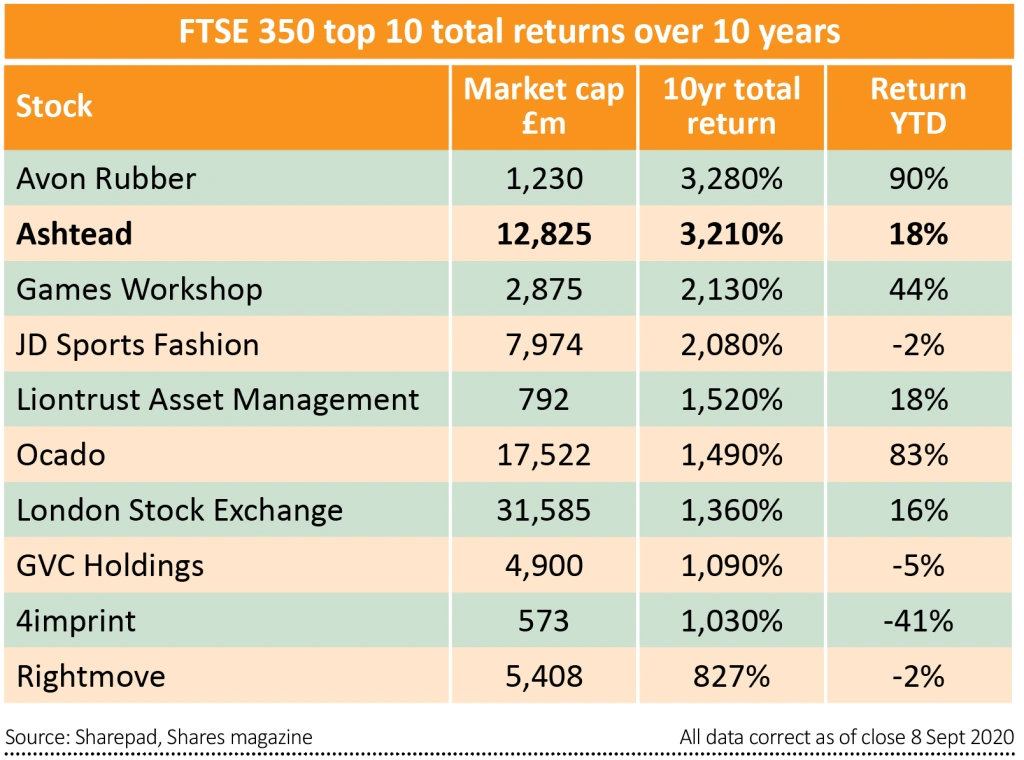

By way of illustration, a simple screen of the FTSE 350 index for 10-year total returns – in other words capital gains plus reinvested dividends – puts Ashtead second with an astounding 3,210% return.

This is partly thanks to the firm’s remarkable earnings growth – reported earnings per share have risen 268 times from 2010 to 2020, or a compound annual growth rate of 75% – and partly to its policy of rising dividends, which have gone from 2.0p per share in 2010 to 40.65p this year.

This growth is thanks to consistent double-digit increases in annual revenue, although that may be coming to an end. From increases of 20% or more from 2013 through 2019, revenue growth slowed to 11% in the year to 30 April 2020 and is forecast to be no more than mid-single digits for each of the next three years.

After such substantial gains, can the firm continue to deliver? Are analysts being too cautious with their revenue forecasts, or is the firm priced for perfection?

MARKET DYNAMICS

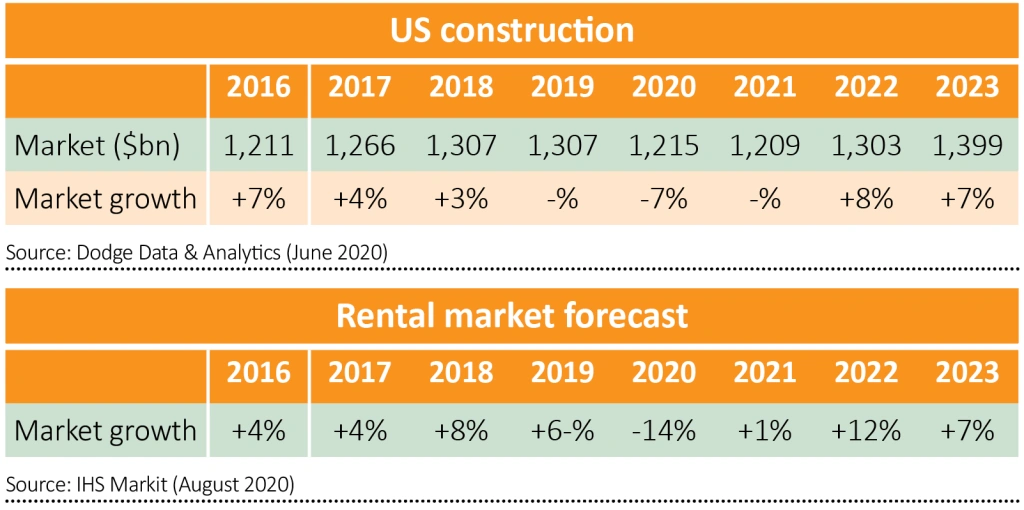

Ashtead makes the bulk of its earnings in the US through its Sunbelt rental business. Roughly half of its US turnover comes from the construction market and half from markets such as infrastructure, facilities management, air quality management and emergency response.

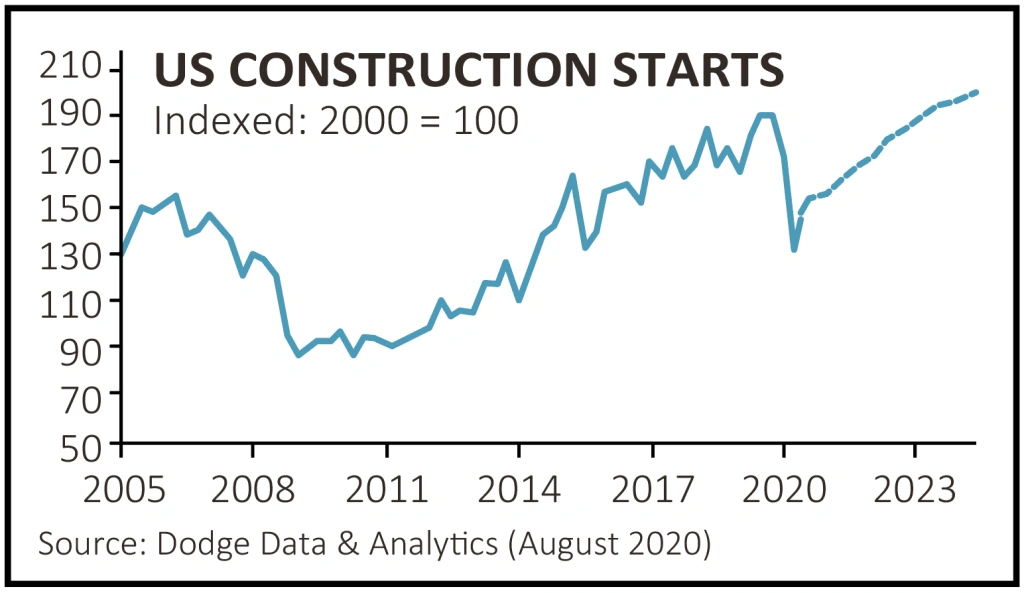

The US construction market is mind-bogglingly big – each year somewhere in the region of £1.3 trillion of work is put in place – although figures from consultant Dodge Data suggest that the market didn’t grow in 2019 and due to Covid-19 it could take until 2022 to get back to a similar level of turnover.

The equipment rental market, which had been growing by mid-single digits up until last year, is forecast to shrink by as much as 14% this year before recovering slowly through 2021 and beyond, according to IHS Markit. Clearly there are headwinds.

However, even in 2019 when the US construction market stagnated, Ashtead still grew its rental revenues by 10% thanks to 6% organic growth – through the addition of 85 new stores – and 4% growth from bolt-on acquisitions.

Meanwhile its non-construction business boomed with total rental revenue growth of 9% or three times that of the market thanks to specialty areas such as power, heating, ventilation, air conditioning, climate control and air quality.

In an indication of the size of the market for specialty equipment, Sunbelt currently has over 5,000 portable air quality units on rent in the US.

The Canadian rental market is considerably smaller than the US but it offers significant growth potential. Sunbelt Canada’s rental-only revenues last year were C$420 million in a market that reached C$7.4 billion, meaning it had just over a 5% share.

However, sales grew at a 30% clip thanks to organic growth of 8% plus bolt-on acquisitions and there is clearly scope to continue consolidating and gaining share.

The third leg of the business is the UK, where 20 separate brands have recently been consolidated under the Sunbelt banner and which makes up less than 10% of group turnover. Given the highly competitive nature of the market, management has been realigning the business, reducing the amount of fleet on hire and trying to improve returns.

STRONG MARGINS

One of the most outstanding features of Ashtead’s business is its high returns on capital. Operating or EBITDA (earnings before interest, tax, depreciation and amortisation) margins are consistently high, even in the UK business which lags the group average.

Despite the sudden Covid-driven fall in activity in the final quarter of the last financial year, which made a significant dent in profit given that a large proportion of short-term costs are fixed, group EBITDA margins were still 47% and US margins were almost 50%. UK margins were lower but still topped 30% as they did a year earlier.

This ability to generate high returns and to keep reinvesting in the business to create value for shareholders is one of the main reasons why the company is so popular with long-term investors.

‘Management have huge experience of operating through different economic cycles and have a very strong track record of shareholder accretive capital allocation,’ says Trevor Green, head of UK institutional equities at Aviva Investors.

‘As their recent results showed, even in slower periods for their end markets they are prodigious generators of cash. Being the market leader they benefit from periodic sector consolidation and invariably extract economies of scale from their acquisitions,’ adds Green.

Commenting on the firm’s latest results, Numis analyst Steve Woolf flagged Ashtead’s ‘ability to navigate a period of extreme market volatility, while maintaining a focus on cost, cash generation and high levels of customer service’.

In the three months to 30 June, when all three of its major markets suffered a sharp contraction in activity, the company still managed to outperform with group revenues down just 6% as its specialty business stepped up by supplying essential equipment to government and private firms.

The company observed that activity levels had ‘increased consistently through the quarter’ such that as of the end of June it had almost as much fleet on rent in the US and Canada as last year and slightly more in the UK.

As trading improves, Ashtead should emerge with even greater market share says Woolf, ‘further highlighting its competitive advantage’.

CONTRARY VIEW

Yet not everyone agrees with this bullish view. Analysts at investment bank Berenberg believe Ashtead’s shares are ‘defying the softness in lead indicators and enjoying the propulsion of the recurring narrative of a still elusive US infrastructure bill’.

Central to their negative argument is that ‘a combination of reduced asset utilisation, softer used equipment pricing, and renegotiations of rental rates on equipment coming off-hire between cancelled or postponed projects’ will lead to margin weakness.

While the latest results and outlook comments from management seem to have reassured investors, the analysts believe consensus cash flow forecasts are too high and remain ‘cautious about the prospects for medium-term profitability’, while warning that ‘these risks are not adequately discounted in the share price’.

Liberum analysts Charlie Campbell and Marcus Cole point to Ashtead’s financial solidity and cash generation and expect the firm ‘to continue gaining share through its superior service offer, and to enjoy structural growth from increasing exposure to new markets’.

However, like Berenberg they believe the shares are over-priced in the short term and struggle to see much upside after a strong performance and with its fairly full valuation.

Long-term investors are more interested in the firm’s well-documented ability to keep compounding its earnings. ‘Its markets have the tailwind of steady structural growth,’ says Green. ‘Even though the share price is hitting all-time highs, investors shouldn’t be put off as the valuation remains compelling with past share price appreciation matched by strong earnings growth.’

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.