Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWhat the race to the White House means for investors

Milwaukee, Wisconsin and Jacksonville, Florida are home to two of America’s National Football League’s 32 teams, the Green Bay Packers and the Jacksonville Jaguars.

Owing to the pandemic, it is not clear at the moment whether gridiron fans will be allowed into their stadia at any stage this season to watch the games, which are due to begin in September.

But two other important events in these cities have already fallen foul of Covid-19. The recent Democratic Party convention, slated for Milwaukee, became a virtual affair as the majority of speakers stayed away, even while Joe Biden and Kamala Harris punched their ticket as the party’s chosen pairing for the next US Presidential election, which is due on 3 November.

Meanwhile, the Republican incumbent in the White House, Donald Trump, had already cancelled his planned convention in Jacksonville, although a pared-down affair took place in Charlotte, North Carolina on 24 August as he and vice-president Mike Pence prepared to run for a second term in office.

The race is now on between the Trump/Pence and Biden/Harris teams, to give investors something else to mull over as they continue to wrestle with how the pandemic will affect the world’s largest economy.

The political temperature will only rise from here, with three presidential television debates scheduled for 29 September, 15 October and 22 October and one vice-presidential contest on 7 October before Americans head to the ballot box.

Voting patterns

In admittedly very crude terms, you might expect the US stock market to prefer a Republican president to a Democrat one, with the Grand Old Party generally seen as being in favour of small(er) government and less inclined to interfere in business matters and free markets than the Democrats.

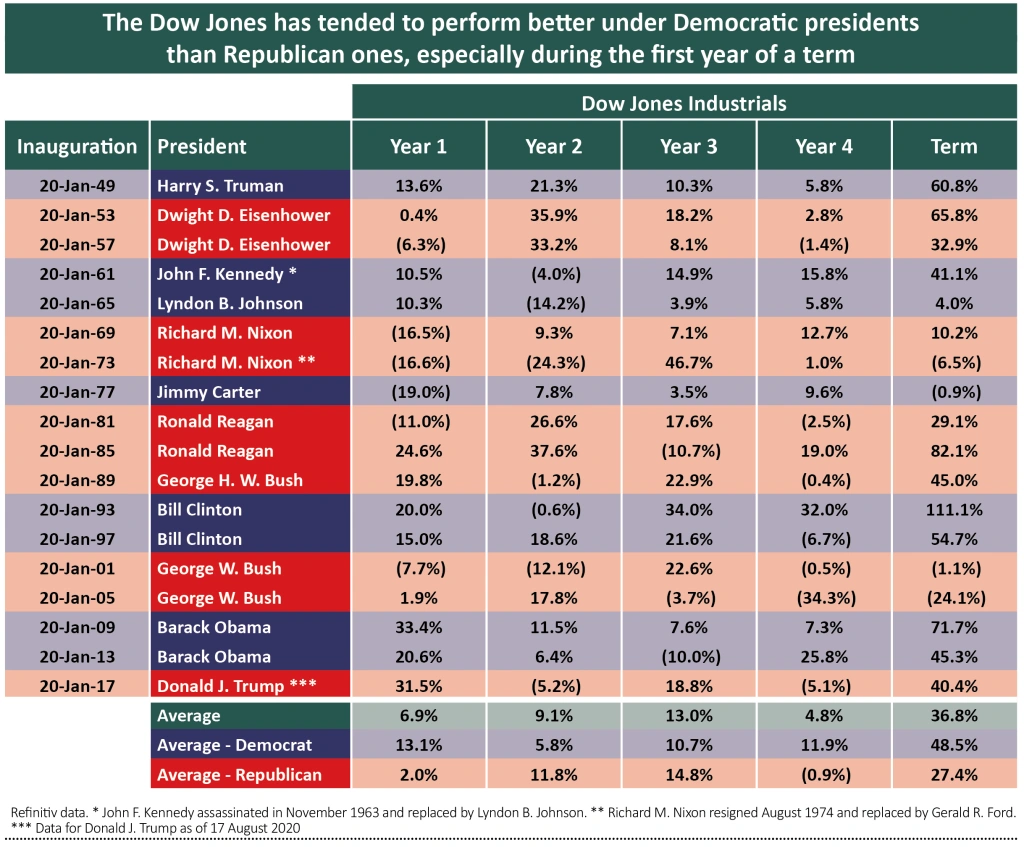

However, it generally has not worked out like that, at least not in modern times. Over 18 presidencies since the election of Harry S. Truman in 1948, the Dow Jones Industrial Average index has, on average, done better under Democratic presidents than it has Republican ones.

Even more intriguingly with 2021 in mind, the Dow has done much better in the first year of a Democratic term than it has a Republican one, with an average gain on 13.1% compared to 2% from their rival incumbents.

A long time ago

It therefore is not as simple as ‘Republicans good, Democrats bad’ when American politics is assessed through the very narrow prism of the US stock market.

This is particularly the case now when the Republicans were running up the sort of budget deficits that would make even the most ardently pro-spending Democrat blush, even before the pandemic forced an emergency fiscal response.

Moreover, if investors cast their minds back four years ago, the Democrats’ Hillary Clinton was then seen as a bit of a shoo-in for the 2016 election, as the Republican’s Trump had surprised everyone by winning the Grand Old Party’s nomination.

Trump was also widely perceived as a potentially negative result for markets, thanks to his sabre-rattling on issues such as diplomatic relations with China, Iran and Mexico and desire to rip up several trade agreements, including the North America Free Trade Agreement (NAFTA).

But that isn’t how it turned out. The Dow Jones is up by some 40% since Trump’s inauguration on 20 January 2017, thanks to what had been a steady economic expansion, tax cuts and an accommodative US Federal Reserve, which had pretty quickly backed away from raising interest rates and sterilising quantitative easing, even before Covid-19 swept around the globe.

This suggests that there is more than just politics at play when it comes to how a stock market performs, with monetary policy, economic performance and the possibility of exogenous shocks (such as a pandemic) all factors to be considered, among others, even before we get to the vexed issue of valuation.

That said, Trump has undeniably been influential, from his market-pumping tweets to his economy-pumping tax cuts. How much bearing November’s winner has upon financial markets’ performance will to a degree depend upon which party wins the House of Representatives and the Senate, so investors will need to consider this too.

The tricky thing is sorting out the policies that are just electioneering and slogans from the plans that may actually be enacted. As the economist Robert Sowell once noted: ‘Economists are often asked to predict what the economy is going to do – but economic projections require predictions what politicians are going to do and nothing is more unpredictable.’

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Editor's View

Feature

Great Ideas

News

- BT takeover hopes shot down by analysts

- Balfour Beatty's £2bn contract win fails to move its shares

- BlackRock World Mining’s ’decade of lost returns’

- Analysts say Greencoat Renewables cannot justify premium rating

- M&A revival predicted after worst first-half for deals since 2010

- Investor hopes raised over Covid treatments