Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineSoftcat investors rewarded with rising share price and dividends

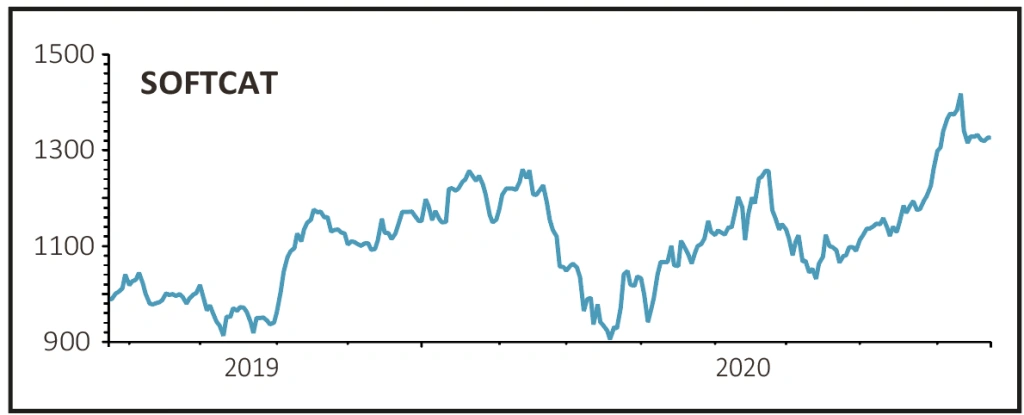

SOFTCAT (SCT) £13.20

Gain to date: 37.5%

Original entry point: Buy at 959.5p, 1 August 2019

Our returns have doubled on software reseller and IT advisor Softcat (SCT) since we last updated on the stock two months ago, demonstrating how this technology enabler has been able to capitalise on Covid-19.

Its latest trading update (19 Aug) emphasised its reputation as a fine growth business. The company flagged the return of a dividend that was originally cancelled in response to the Covid-19 outbreak while adding that full-year operating profit would be ‘slightly ahead’ of expectations.

Worth noting was the strong cash generation, an important factor in its decision to recommit to pay the dividend. Full-year results to 31 July 2020 will be released in late October.

‘This is another robust performance bearing in mind estimates were never downgraded for the pandemic,’ says Numis analyst Tintin Stormont. We can only agree given the firm’s ongoing excellent performance both operationally and in share price terms.

Peel Hunt analyst James Lockyer upped his own earnings estimates for year to 31 July 2020 and 2021 by 4% to 6%, thanks to good cost management.

SHARES SAYS: Softcat continues to repay the faith of investors during a testing time. Still a buy for the longer-term.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Editor's View

Feature

Great Ideas

News

- BT takeover hopes shot down by analysts

- Balfour Beatty's £2bn contract win fails to move its shares

- BlackRock World Mining’s ’decade of lost returns’

- Analysts say Greencoat Renewables cannot justify premium rating

- M&A revival predicted after worst first-half for deals since 2010

- Investor hopes raised over Covid treatments