Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineMore upgrades send Luceco shares soaring

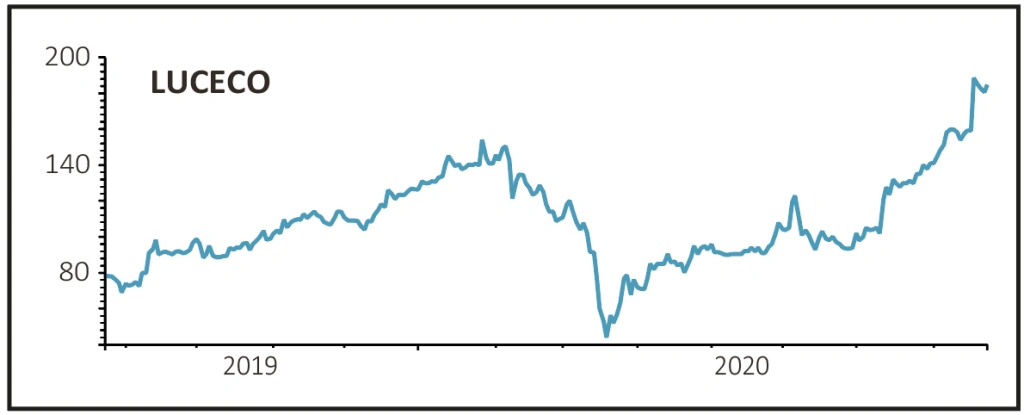

LUCECO (LUCE) 186.5p

Gain to date: 60.1%

Original entry point: Buy at 116p, 19 December 2019

If February and March provided some pain for investors who followed our Luceco (LUCE) investment idea, they’re certainly getting rewards now. The stock has gone bananas, shooting to levels not seen since 2017, and delivering a 60% gain since we said to buy last December.

The recovery in the LED lighting and portable power products maker from the worst of the pandemic shutdown has been astonishing, clearly catching management and analysts out in equal measure. This was a real bolt from the blue, with an update on 19 August coming barely a month after Numis had to rethink its 2020 estimates for the second time.

The latest forecast revision is significant, with Numis analyst Kevin Fogerty hiking his adjusted earnings before interest and tax (EBIT) and earnings per share (EPS) by 22% and 29% respectively above the July-issued estimates. His forecasts for 2021 were given a similarly marked upgrade.

What this means is that 2020 EPS of 11.6p per share is now anticipated, where 9p was predicted just a month ago. EPS of 12.1p has been pencilled in for 2021. So even after the stock’s soaring run it remains undemanding in valuation terms, on a price-to-earnings multiple of 16, falling to 15.4 next year.

SHARES SAYS: Stick with the shares as Luceco clearly has

positive sales momentum.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Editor's View

Feature

Great Ideas

News

- BT takeover hopes shot down by analysts

- Balfour Beatty's £2bn contract win fails to move its shares

- BlackRock World Mining’s ’decade of lost returns’

- Analysts say Greencoat Renewables cannot justify premium rating

- M&A revival predicted after worst first-half for deals since 2010

- Investor hopes raised over Covid treatments