Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazine5 great stocks to buy now

Many people are prepared to pay a high price for growth in the current market. Indeed, Shares has been keen to extol the virtues of quality businesses capable of growing despite a troubled backdrop.

However, we sense growing interest in the market for value opportunities and our research shows it is currently possible to find decent companies trading at attractive prices.

Warren Buffett famously said: ‘Whether we’re talking about socks or stocks, I like buying quality merchandise when it is marked down.’ Investors should certainly follow his words.

We also note that Bank of America last week declared the last leg of the recovery rally is set to be driven by value stocks, helped by rising bond yields.

SCANNING THE MARKET

To help find opportunities, Shares has employed several different measures of value including the relatively simple price-to-earnings (PE) ratio, through to price-to-earnings growth (PEG) and price-to-book.

Identifying genuine bargains is much more than just a data crunching exercise as stocks can be cheap for a reason. A business with lots of debt on the balance sheet may look optically attractive on a PE basis but a lot of its earnings will have to go towards servicing debt which means the financial risks are significantly higher, particularly at a time when the economic outlook is so fragile.

For example, according to SharePad data roadside assistance provider AA (AA.) trades on a forward PE of just 3.5 but its £2.65 billion worth of debt comes in at seven times its earnings.

There are other reasons why stocks trade at a discount such as scepticism over the sustainability, transparency and reliability of its earnings. A firm might have a patchy track record or a history of corporate governance failings. Or its entire business model might be structurally challenged.

Newspaper publisher Reach (RCH), for example, trades on a PE of just 1.9 for 2020. It doesn’t have lots of debt to worry about (although it has significant pension liabilities) and it is cash generative but the major sticking point for investors is the consistent decline in earnings from its core newspaper business.

LOOK AT BOTH SIDES OF THE STORY

If you think you’ve spotted a value opportunity, make a list of all the reasons not to buy it. If this list is longer than one or two items or if one issue is so acute that it keeps nagging away at you, then chances are you could be walking into a value trap.

You also need to identify potential catalysts which can change the market’s perception of a share, leading it to trade on a higher valuation. This might be evidence of an improvement in trading, a change in management or a shift in sentiment toward the sector in which it operates. Read on to discover five stocks we think look great value and have lots of positive attributes.

B.P. Marsh (BPM:AIM) 226.5p

Market cap: £85 million

Specialist investment firm B.P. Marsh (BPM:AIM) offers individual investors the opportunity to gain exposure to early-stage financial businesses which would normally be beyond their reach.

Since it was founded in 1990 the firm has invested in 50 businesses including financial advisers, insurance companies, wealth and fund managers, and specialist consultancy firms across the globe.

It typically invests up to £5 million in the first round of fund raising, and target companies range from complete start-ups to more developed businesses. Initially it only takes a minority stake, but it works alongside management to maximise value as the business develops.

The current portfolio is strongly weighted towards insurance with all but one company operating in this sector, although given its targeted approach it has exposure to a wide variety of specialist classes of insurance. As a group, its gross written premiums topped $1 billion in the year to January.

In its last financial year the firm posted an 8.5% increase in net asset value (NAV) to £136.9m, net of dividends, meaning an increase of 29.8p in per-share NAV to 380.1p. Including the dividend paid last July, total shareholder returns increased by 9.8%.

Most of the gains were driven by Marsh’s two biggest insurance businesses, UK-based underwriter Nexus and US-based underwriter XPT Group, which accounted for 35% and 9% of group NAV respectively, and by its investment in UK financial adviser LEBC which accounted for 22% of group NAV.

It first invested in Nexus in 2014, taking a 5% stake. Since that time, the investee firm has bought six businesses including the global flying book of British insurer Hiscox (HSX). Marsh now has a 17.6% shareholding and since its first investment the value of Nexus has grown from £31 million to £228 million.

With Marsh’s help, Nexus has grown its gross premiums from £31m to £325m and its adjusted earnings before interest, tax, depreciation and amortisation (EBITDA) has gone from £2.3m to £15m.

This growth has come from new product lines such as trade credit underwriting as well as small bolt-on acquisitions.

Meanwhile, from a standing start in 2017, XPT is expected to write $300m of gross premiums this year, yet Marsh’s cost of investment for a 29.9% stake was just over £7m. Just last month XPT announced it had made a seventh acquisition and beefed up its senior management team to aid further growth.

Some of Marsh’s smaller investments have done even better. Its 38% stake in UK insurance brokerage CBC, which cost just £4000, is now worth over £7m.

While the pandemic carries a potential impact on the carrying value of the firm’s investments, chief investment officer Dan Topping believes it is ‘unlikely to negatively influence the portfolio as a whole in a material fashion’.

ELECO (ELCO:AIM) 77p

Market cap: £63.6 million

We think Eleco (ELCO:AIM) could be in an interesting position as the wider construction industry embraces digitisation. Until recently known as Elecosoft, the company has been in business for more than 100 years but turned itself into a construction industry technology supplier when it sold its physical building operations in 2013.

These days it provides specialist software solutions that cover the core elements of a construction project, such as computer-aided design and visualisation, engineering resource planning, cost estimation/tracking, site operations/maintenance, plus building information management which acts as the glue connecting all the various modules.

It sells primarily in the UK, Sweden and Germany, with earnings also coming from the Benelux region and the US through reseller partners. The software is used by some big industry players, including international building firms Skanska and Mace and global wood flooring supplier Boen, and has been used on some landmark projects such as The Shard, the BBC Television Centre, Hong Kong International Airport and Berlin’s Reichstag Dome.

Like many software businesses that have been around for a while, Eleco is gradually transitioning to the cloud and a software-as-a-service model of recurring annual subscription revenues. About two-thirds of last year’s £25.4 million revenue was recurring, the rest is multi-year licences with servicing/maintenance on top.

This year won’t have been easy for the business, although the fact that construction was one of the first industries to get back to work post-Covid has helped. Management sensibly cut costs early.

A recent trading update said first-half earnings held up well with adjusted pre-tax profit to 30 June up 14% despite a 4% decline in revenues. Analysts imply this to mean around £2.3 million profit on £12.2 million sales. Cash generation was strong, turning £1.1 million net cash at the start of the year into a £4.4 million net cash pile.

Analysts seen to think the underlying outlook is improving, which is encouraging given that the building industry is still operating under social distancing rules. This is partly thanks to the launch of new AI visualisation tools, but the real gains should come from the ongoing use of digital tools into the future.

Eleco last year generated 14.9% return on capital and 16.2% return on equity, which is a solid performance. Its operating margin was 15%.

The shares look cheap on earnings growth basis with a PEG ratio of just under 1 using the last published forecasts. The two brokers covering the stock have temporarily withdrawn estimates which is something prospective investors need to consider. Estimates are likely to be reinstated when results are published in September.

Last month Equity Development analyst Paul Hill said Eleco (trading roughly at the same share price as now) was attractively priced, trading on 2.4 times 2019 enterprise value-to-sales compared to typical industry multiples (pre COVID-19) of 4 to 7-times. He added that Eleco’s two closest rivals, Nemetschek and Autodesk, were priced at more than 10 times EV/turnover.

We note that Eleco was added earlier this year to CFP SDL Free Spirit Fund’s (BYYQC27) portfolio. This fund is ranked top in the IA UK All Companies sector for the past three years’ performance, implying that fund manager Andrew Vaughan knows his stuff when it comes to picking stocks.

Ferrexpo (FXPO) 187.6p

Market cap: £1.1 billion

FTSE 250 iron ore miner Ferrexpo (FXPO) is a quality, high yielding stock that appears to be significantly undervalued by the market.

A producer of high grade iron ore pellets, Ferrexpo has a strong track record of profitability and cash generation, and has proven itself to be a reliable income stock with the potential for growth.

The company, which is Swiss-headquarted but has its mining assets in Ukraine, has also weathered the current coronavirus crisis well, with only a modest hit to revenues, earnings and margins.

While others in its sector have increased their debt to cope with the pandemic fallout, in the six months to 30 June Ferrexpo cut its borrowings, with net debt to last 12 months’ EBITDA down to 0.31, compared to 0.48-times as at 31 December 2019.

Being in a position of strength thanks to particularly buoyant iron ore pellet prices, in its half-year results Ferrexpo also declared a second interim dividend of 6.6 US cents, in addition to the 6.6 US cents interim dividend it declared in June.

Shore Capital calculates the two interim dividends as being equivalent to a yield of 5.6%, or a ‘stupendous’ 11.1% annualised (i.e. assuming similar further dividends for the second half of the year).

But still the company appears to be unappreciated by the market, principally because of corporate governance concerns.

It trades on a price-to-book value of 1.19-times – a better metric for miners compared to price-to-earnings – which is about average for its sector, but it has an enterprise value-to-EBITDA ratio of just 3.

According to Stockopedia, the company scores well on various quality measures, with return on capital employed, return on equity and operating margin all above 30%, making it a high quality company generally and particularly high quality when compared to its peers in the metals and mining sector.

Ferrexpo has many potential catalysts for a re-rating. These include higher pellet premiums towards the end of the year if the global economy recovers, while increasing activity in the automotive and construction sectors in the EU and Asia should see steel demand rise, again benefiting Ferrexpo.

Longer term, Chinese pellet demand will be a big factor as pollution controls are implemented across Chinese cities, meaning Chinese steel mills transition from lower-grade, higher-impurity iron ores toward the higher-grade feedstocks Ferrexpo provides.

It will also be a similar situation for Ferrexpo in the EU as demand should rise thanks to tighter emissions controls and regulation.

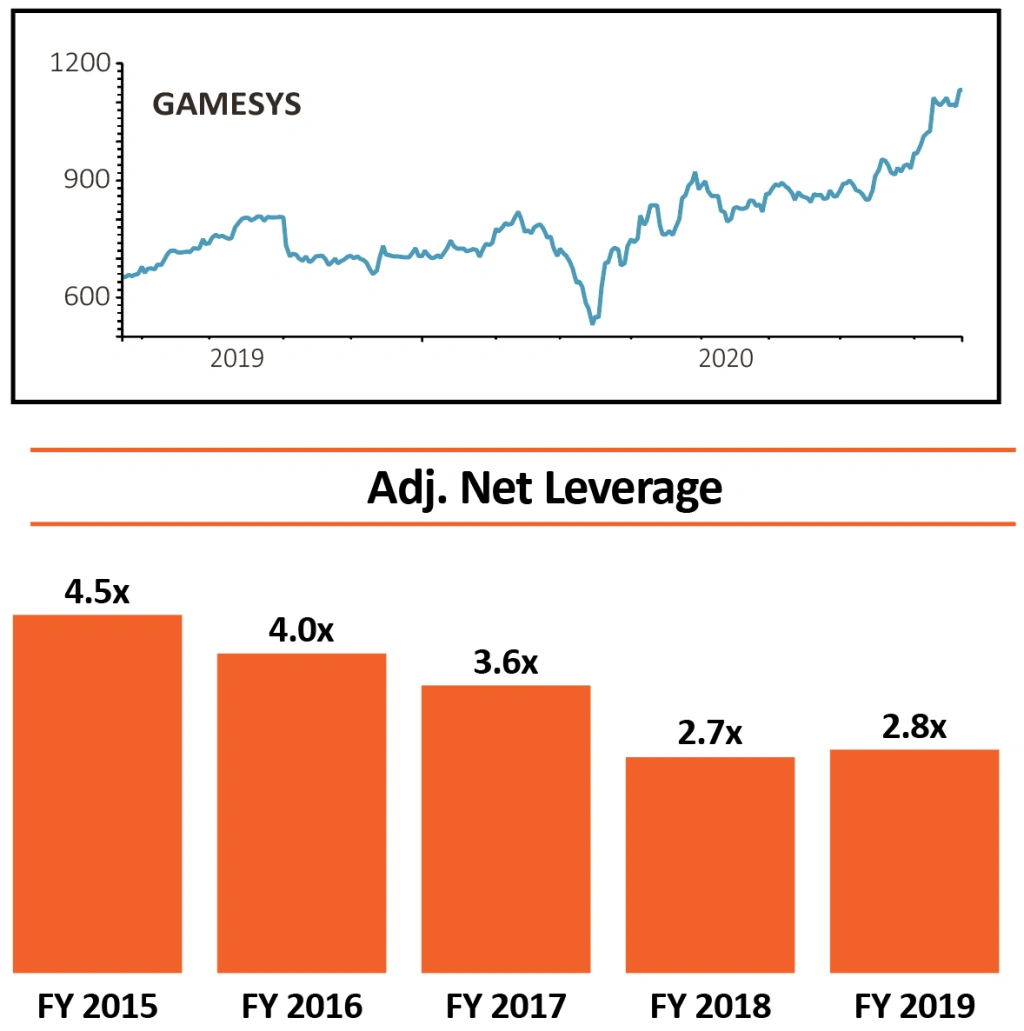

Gamesys (GYS) £10.90

Market Cap: £1.2 billion

Having built a diversified portfolio of well-established brands through acquisitions and developed a platform for international growth, casino and bingo-led Gamesys (GYS) offers investors the prospect of increasing shareholder returns through deleveraging and initiating a progressive dividend policy.

This is not reflected in the low 12-month forward price-to-earnings ratio of 8-times which is probably influenced by the historically high indebtedness of the company.

Companies with higher debts are forced to spend some of their cash flow on servicing their debts rather than paying shareholders in dividends or reinvesting in the business for growth.

For this reason, investors penalise highly leveraged firms and back in 2015 Gamesys had a net debt-to-earnings before interest, tax, depreciation and amortisation (EBITDA) of 4.5-times which compares with the current level of 2.2-times. Management have targeted a range of between one and two-times.

Theoretically as the debt is paid back, more of the operational cash flow is available to shareholders which should increase the earnings multiple that investors are prepared to pay for the shares.

Gamesys has announced a maiden dividend of 12p per share to be paid in October with an expected final dividend of 24p, providing a forecast yield of 3.3% covered three times by earnings.

As debts get repaid there is scope for the dividend to increase through time, providing further benefits for shareholders.

First-half results to 30 June showed impressive growth with year-on-year revenues up 27% to £340 million fuelling 17% growth in EBITDA to £95 million. Asia was stunning with growth of 92% while the UK chipped in a respectable 16%.

Europe saw revenues fall 4% impacted by challenging markets in the Nordics, offset by good growth in Spain and Germany, while the US was the standout performer in the rest of the world, generating 37% growth.

The firm has a 30-year trademark licensing agreement with Virgin and 160 worldwide licenses to operate Monopoly branded websites for an initial term until the end of 2025. The product is available across 114 countries in 47 languages and over 1 billion people have played Monopoly across the globe.

The scope to further internationalise the brands is considerable given that both have over 95% brand awareness worldwide.

In the UK the company enjoys a leading position in online bingo through the Jackpotjoy brand.

The journey towards a more shareholder-focused strategy is only in the early stages and should provide rewards over time.

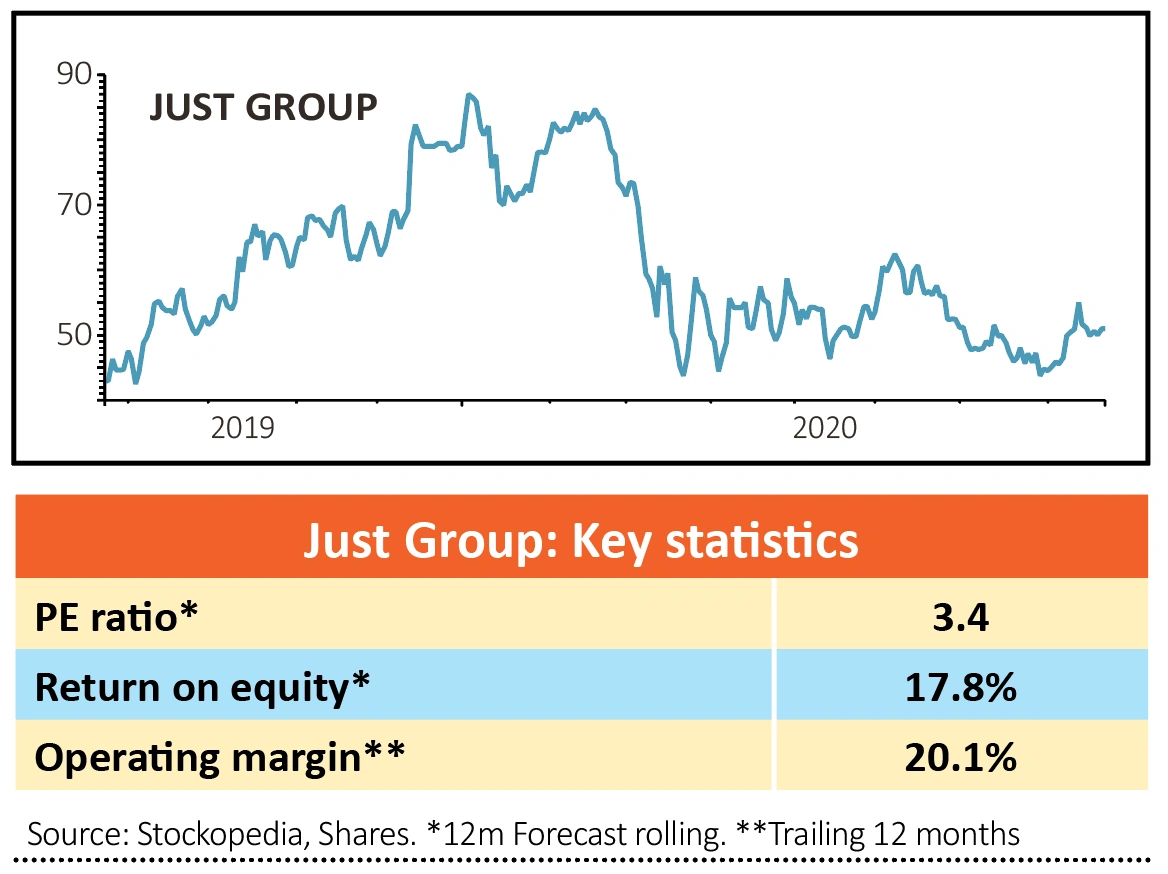

Just Group (JUST) 49.68p

Market cap: £515 million

Management action has put retirement solutions provider Just Group (JUST) on the front foot.

The specialist financial services firm, which is focused on the UK retirement income market, passed a major milestone earlier this month after it reported a move to a net positive cash generation position, delivering on its promise to build a more sustainable and resilient business model.

In early 2019 chief executive David Richardson took a tough decision to manage the firm’s capital more tightly and raise its internal rate of return with a view to achieving ‘capital neutrality’ by 2022.

This meant raising prices on its guaranteed income for life products, at the expense of business volumes, cracking down on costs, selling loss-making operations like its US arm and a shift towards more capital-efficient assets.

The plan worked. As at the end of June this year the firm had turned from a net cash outflow of £36 million in 2019 to organic cash generation of £145 million thanks to ‘reduced new business strain and improved in-force surplus generation’ which were the direct result of management action.

‘We have a clear strategy focused on improving the group’s capital position and we are making good progress in adapting our business model to achieve our strategic goals. Despite operating in a tough environment, we took big strides in improving our organic capital generation and reducing balance sheet risks in 2019,’ says Richardson.

The firm kept its 1,100 staff on full pay throughout the pandemic, with 98% working from home servicing clients as usual. Despite initial fears that people would put off making decisions about their financial future, in the event customers responded well to the situation as did the independent financial adviser sector.

Richardson believes business volumes should get back to 2019 levels by the fourth quarter of this year. Indeed, demand for defined benefit annuity products has ‘never been stronger’ says the chief executive.

Thanks to two major de-risking initiatives this year – one covering property risk and one for defined benefit deals above £250 million – the firm is writing larger transactions with a capital-light model. Writing bigger-ticket deals mainly using external capital opens a much bigger market for the firm.

It has also developed an innovative decumulation product for customers approaching retirement who want to gradually move their assets into guaranteed income for life, opening yet another market.

Meanwhile tangible net asset value continues to grow, reaching 204p per share in the first-half period against 181p at the end of December 2019, and a share price of just under 50p.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Editor's View

Feature

Great Ideas

News

- BT takeover hopes shot down by analysts

- Balfour Beatty's £2bn contract win fails to move its shares

- BlackRock World Mining’s ’decade of lost returns’

- Analysts say Greencoat Renewables cannot justify premium rating

- M&A revival predicted after worst first-half for deals since 2010

- Investor hopes raised over Covid treatments