Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineMarket share gains to fuel Motorpoint

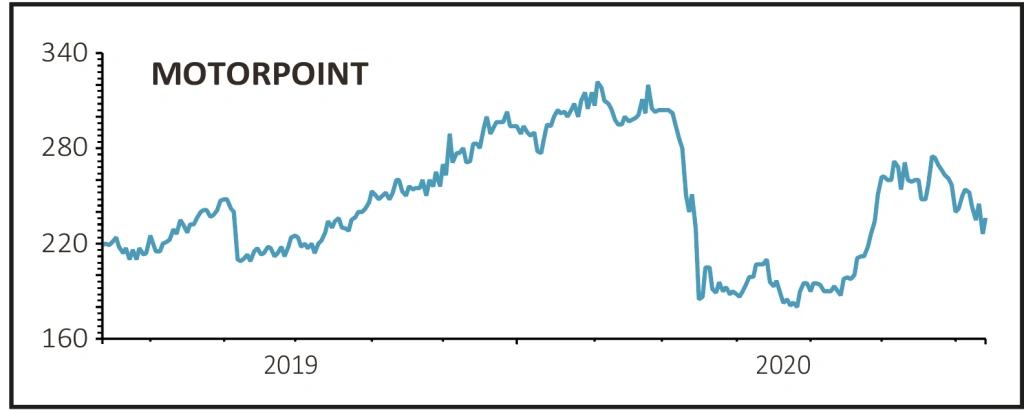

MOTORPOINT (MOTR) 241p

Gain to date: 26.8%

Original entry point: Buy at 190p, 14 May 2020

Our positive stance on second hand car specialist Motorpoint (MOTR), based partly on a return to work tailwind, is a bumper 26.8% in the money.

And we are staying positive on the nearly new vehicle seller given its strong balance sheet and scope for further market share gains.

Full year results (14 Jul) reflected the impact of the Covid-19 crisis and the subsequent lockdown on the key March trading period, with site closures behind a 15.3% drop in pre-tax profit to £18.8 million. Motorpoint understandably decided to pull the final dividend.

However, the positive news was Motorpoint’s encouraging restart post lockdown, with current trading stronger than anticipated and ahead of the same period last year, margins said to be robust and cash levels significantly ahead of the year-end balance and trending positively.

At this stage, it is too early in the unlocking process to decipher whether recent weeks reflect pent up demand or a return to more normal trading conditions, but Motorpoint is seeing strong web traffic and has also invested for the post-coronavirus future via a move towards automation with fully contactless sales routes.

SHARES SAYS: Keep buying.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Editor's View

Feature

First-time Investor

Great Ideas

- Market share gains to fuel Motorpoint

- Analyst upgrades Luceco forecasts for the second time in as many months

- Play the healthcare boom via ‘best in class’ UDG

- QinetiQ growth strategy progressing despite challenges

- Buy care home investor Target Healthcare for a 6% yield

- Hipgnosis is cashed up and ready to buy more songs

- Ocado has a monumental growth opportunity

Investment Trusts

Money Matters

News

- US earnings season unlikely to add clarity to full year outlook

- Red hot Tesla could put huge stock offering on the table

- Fevertree shares fall on margin concerns

- Global company debt could jump by $1 trillion in 2020

- Halma’s record profit streak set to end

- B&M shares hit new record high as analysts upgrade forecasts