Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWhy Scottish Mortgage won’t go the way of Woodford

Shareholders in FTSE 100 member Scottish Mortgage (SMT) have just voted in favour of the popular investment trust increasing the maximum percentage of privately-owned businesses in its portfolio from 25% to 30%.

This is an important development for the trust for several reasons, one of which is the heightened risks associated with investing in unquoted companies – businesses that do not trade on a stock market.

Disgraced fund manager Neil Woodford fell out of favour partly because he deviated from his tried and trusted strategy of buying mainly large caps stocks whose income potential had been undervalued by the market.

Woodford moved away from what had made him so successful at his previous employer Invesco Perpetual and instead invested in lots of tricky-to-value unquoted assets in sectors in which he wasn’t an expert. These illiquid investments were then difficult to sell when he needed to hand investors back their cash.

Given that this style drift was at the heart of the Woodford debacle, should risk-averse investors be worried by the developments at Scottish Mortgage? We think not.

DIFFERENTIATED PROPOSITION

The rapid rise of some of Scottish Mortgage’s most successful investments over the past couple of decades, and their apparent resilience during economic hardship, means some of its biggest stakes increasingly feature in passive tracker funds.

One of the ways Scottish Mortgage can diverge from more mainstream funds is to unearth opportunities among privately-owned companies not listed on stock markets.

GREAT TRACK RECORD

Shares is a long-run admirer of Scottish Mortgage, which gives investors a way to access the world’s most exciting growth companies.

Co-managers James Anderson and Tom Slater identify companies, enabled by technology, which they believe have the potential to be much greater in size in the future thanks to having a proposition which is scalable and could be market-leading in time.

They will hold on to these investments once investee companies become market leaders, thereby turbo-charging returns for shareholders.

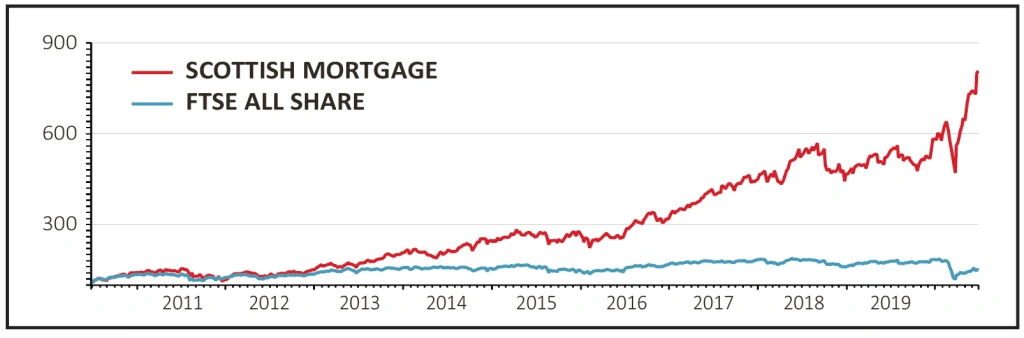

The investment trust performed strongly during the market weakness surrounding the pandemic and economic shutdown and has also benefited during the equity market rebound thanks to its focus on tech companies, disruptive businesses and a relatively high weighting in Chinese domiciled companies.

For instance, the trust owns shares in the likes of video conferencing star turn Zoom, online shopping-to-cloud services colossus Amazon, Google-parent Alphabet and Illumina, which is building advanced equipment to unlock the power of genetic science.

GOING WHERE THE GROWTH IS

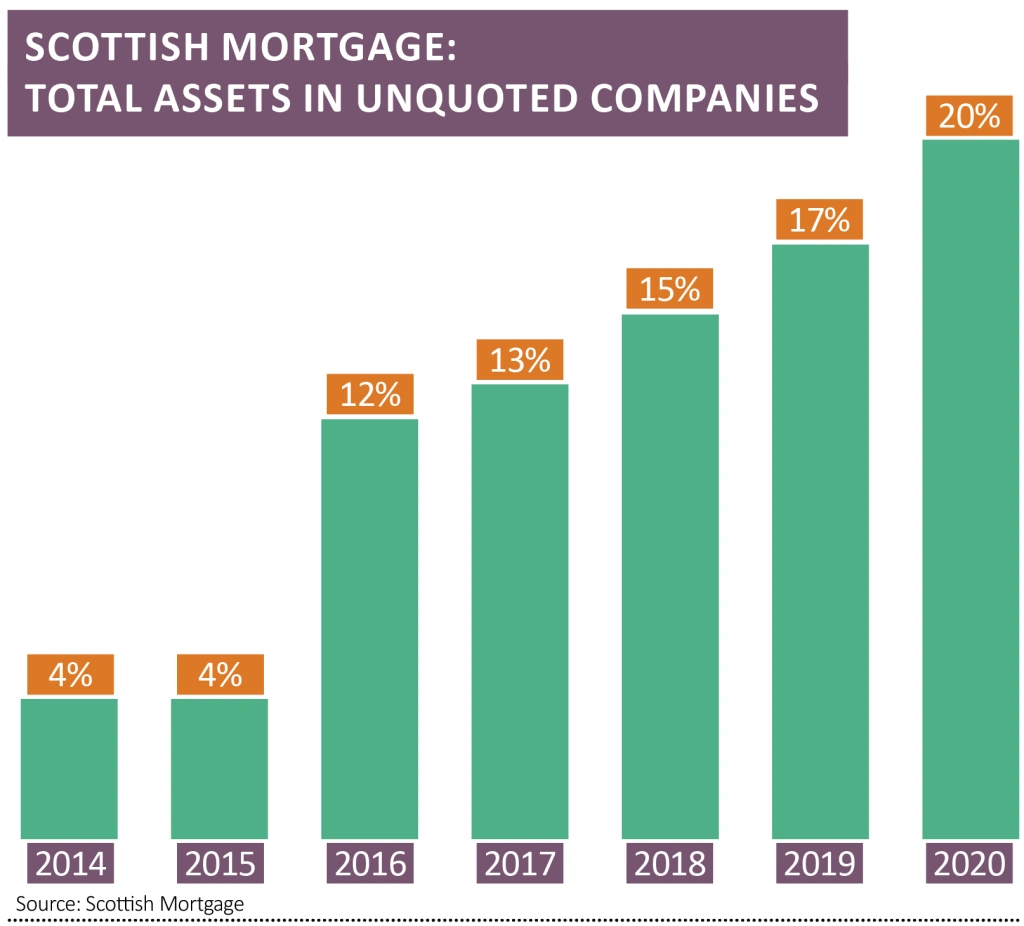

The exposure to unquoted companies in Scottish Mortgage’s portfolio continues to grow rapidly. It has risen from only 4% of net asset value (NAV) in 2015 to 22% as of 31 March 2020.

For Scottish Mortgage to crystalise any value creation from its unquoted investments, it would need to find a buyer for its holdings privately or wait until one of these holdings lists on a stock market so it can freely trade the shares. However, its team are masters at finding excellent growth companies and we have great faith in them picking the right ones.

Analysts at investment bank Stifel say the level of disclosure on unquoted companies in Scottish Mortgage’s accounts has improved and a number of these companies have delivered strong returns for investors in recent years.

Fund managers Anderson and Slater argued for the 5% increase in the unlisted exposure to 30% in the belief that ‘it is just as important to ensure that further investments may be made in those private companies showing real progress, as it is to ensure that all new opportunities may be judged equally on their fundamental merits’.

The unquoted exposure increase will enable them to continue to invest in the best opportunities available, whether they be public or private companies, without changing the nature of the investment proposition.

They say that if Scottish Mortgage hadn’t made this amendment, this valuable flexibility would have become severely constrained and largely dependent on the timings of stock market flotations of existing unquoted companies, to the clear detriment of shareholders.

As Scottish Mortgage clearly articulated in its full year results (15 May), ‘equity investing is all about capturing long run compounding returns’ and one of the important advantages the trust has when investing in established private companies is the ability to continue owning such businesses as and when they become public companies. ‘This means that it is possible to capture the benefits from the long run compounding of returns as they grow from a lower starting value.’

GOOD ACCESS TO GROWTH COMPANIES

Stifel points out that investment manager Baillie Gifford has unparalleled access to many of these unquoted opportunities.

It says: ‘The unlisted portfolio continues to become a more significant part of Scottish Mortgage’s portfolio and potentially returns. The performance of the unlisted segment of the portfolio, as a whole, appears to have been relatively good in the past year at around +11% and this is similar to the performance of the NAV of the rest of the portfolio over the year at +13.7%.’

Admittedly, there have been disappointments – par for the course when investing in unquoted growth hopefuls – but there have also been some significant successes, with five initial unquoted investments delivering annualised returns in excess of 40% per year in recent years.

SEVERAL ADVANTAGES

Shares believes Scottish Mortgage and Baillie Gifford are well positioned to invest in unquoted companies for two key reasons.

Firstly, Anderson and Slater take a long-term view which suits growing unquoted companies – a number of the listed holdings have been owned in excess of 10 years – and they like to hold on to investments for a long time, meaning that a stock market listing is not necessarily the point at which Scottish Mortgage will exit an investment.

Secondly, the closed-end structure of an investment trust works well with an unquoted strategy given there is no requirement for immediate liquidity, unlike an open-ended fund such as the ill-starred Woodford Equity Income.

PORTFOLIO EXCITEMENT

Unquoted companies are growing in importance to the returns delivered by Scottish Mortgage too and add a sprinkle of diversification to a trust with a concentrated portfolio including only 43 listed companies as of the end of May; the largest investment is electric vehicle maker Tesla, followed by Amazon.

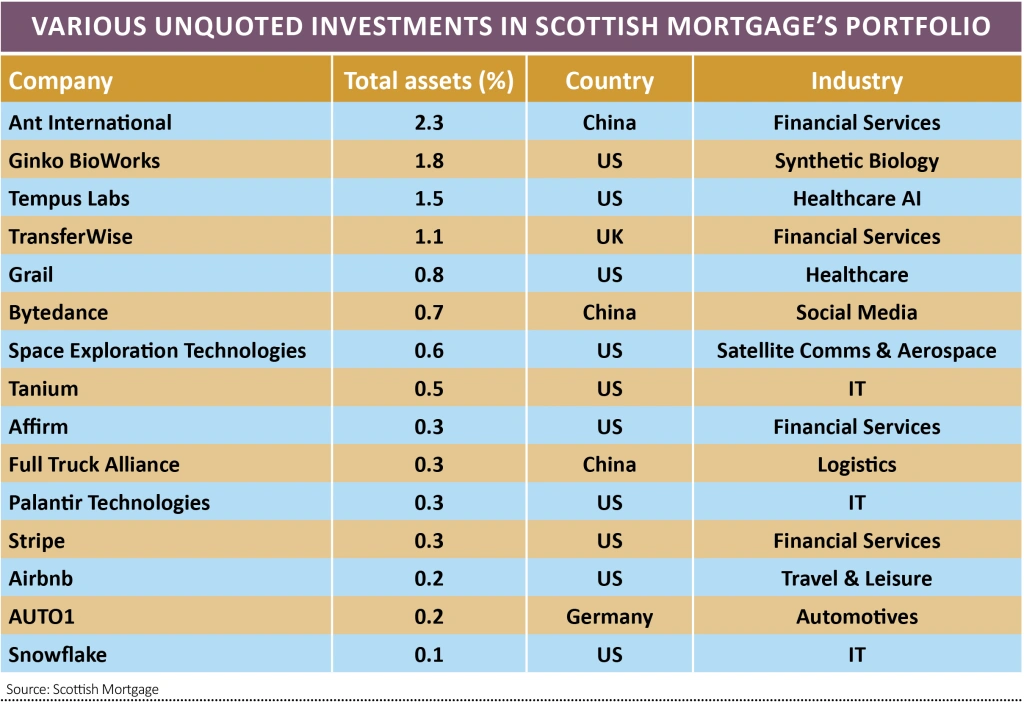

Within the trust’s largest 30 investments there are six unquoted companies, the largest being online financial services platform Ant, a subsidiary of Chinese internet titan Alibaba. While there have been some disappointments, Stifel says there have also been numerous significant successes.

It points out that of the 59 investments that Scottish Mortgage originally backed as unquoted companies, including music and podcast streaming platform Spotify and Alibaba, 21 have delivered annualised returns north of 10% per year, with five of those names, including Alibaba and Slack Technologies, returning over 40% on an annualised basis.

The best performer is Vir Biotechnology whose stake was initially purchased in 2017 and it has returned 115% annualised.

The top unquoted holdings by scale include Elon Musk’s rocket and spacecraft designer SpaceX.

Unquoted portfolio investments expected to float on a stock market in the future include accommodation platform Airbnb; Ant Financial; Bytedance, which owns the social media phenomenon TikTok; and data integration software play Palantir Technologies.

Other private companies in Scottish Mortgage’s portfolio that should excite investors include online payments platform Stripe, cloud data warehousing platform Snowflake and Indigo Agriculture, a company that analyses plant microbiomes to increase crop yields. It is also worth noting stakes in electric aircraft hopeful Joby Aero and Recursion Pharmaceuticals, which uses machine learning to improve drug discovery.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.