Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineTaking stock of markets and the major challenges ahead

As we reach the halfway stage in what has been a year of upheaval, we thought we would look at which markets and sub-areas of those markets have held up best and which are still nursing their wounds.

For the first half of the year the UK’s FTSE 100 benchmark of large cap companies had lost 16.9% while the FTSE 250 mid-cap index had lost 21.9% and the higher-growth AIM 100 market had lost just 8.4%.

WINNERS AND LOSERS

The best performing part of the UK market has been the Leisure Goods sector with a gain of 32.2%, which seems unlikely until you discover that the sector is dominated by ‘stay at home’ success story Games Workshop (GAW). Its fantasy miniatures and intellectual property have been in strong demand through lockdown.

Other winners have been pharmaceuticals, food and drug retailers and personal goods, all made up of large, unglamorous but dependable stocks.

The biggest losers so far are oil services and autos, both of which reflect the lack of travel during lockdown. Close behind are banks, which are essentially a leveraged play on the prospects for the UK economy and the direction of interest rates and as such probably tell us more about the market’s view of what is to come than any of the winners.

VALUE AND EARNINGS

Unlike the US market, which was trading at stretched multiples before the coronavirus crisis, the FTSE 100 was only trading at or slightly above its long term average valuation on the basis of cyclically adjusted earnings prior to the March sell-off.

On the same basis, today it trades close to the level reached at the bottom of the great financial crisis in 2009 which suggests long-term investors could find value in large-cap UK stocks.

However, the flip side of the value case is the fact that earnings will take many years to recover to their previous levels so reversion back to the mean for the market is going to take some time.

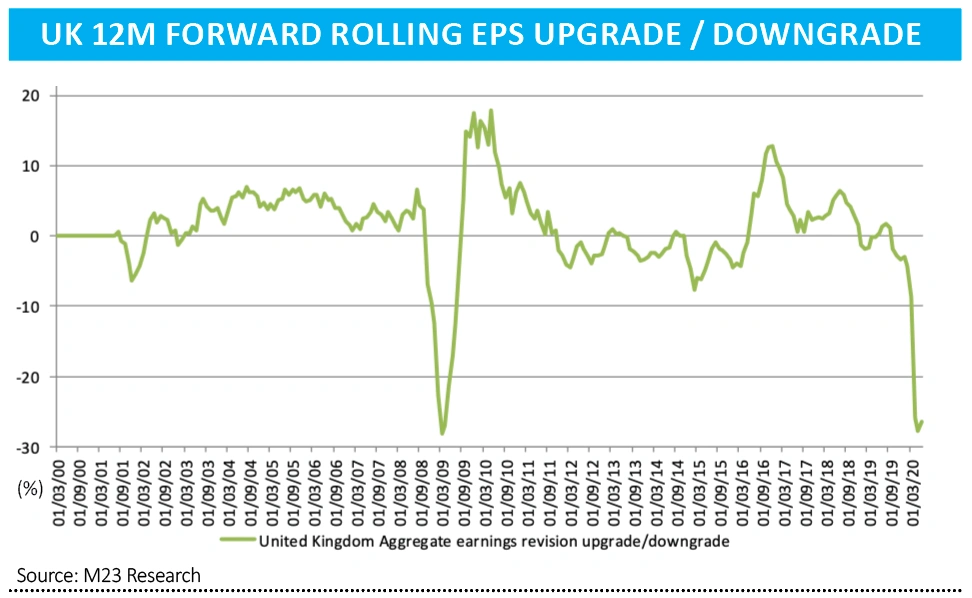

Analysts are currently cutting their 12-month earnings forecasts for the UK market as a whole by more than a quarter, approaching the same level as in early 2009.

Whether they subsequently raise them as fast as they did over a decade ago is the great unknown. For all the talk of a V-shaped recovery, few firms seemed to have any visibility in terms of earnings in their latest trading updates.

First half reports, which will begin rolling in this month, are likely to be a write-off so investors need to concentrate on the outlook statements before coming to any conclusions on particular stocks.

BULLS VERSUS BEARS

Strategists such as Morgan Stanley’s Andrew Sheets are upbeat, arguing that the global economy was showing typical late-cycle characteristics before the pandemic, and that ‘the market is under-pricing the extent to which the recovery could follow the traditional playbook’.

On the other hand, the International Monetary Fund (IMF) has warned that the global economy faces the biggest slump since the Great Depression of the 1930s and that financial markets are ‘disconnected from shifts in underlying economic prospects’.

Last week the IMF cut its 2020 global growth forecast to minus 4.9% from minus 3% previously due to lower consumption, demand shocks from social distancing and an increase in the savings rate as people hunker down.

It also said that if there was a second wave of infections the global economy could flatline instead of growing 5.4% next year.

BREXIT TIGHTROPE

Politics is likely to play a large part in how markets behave in the second half of the year, both in the UK and abroad.

While there seems to have been little progress so far on a Brexit deal with the EU, European chief negotiator Michel Barnier believes an agreement is still within reach as long as the UK adheres to ‘the letter and the spirit’ of its non-binding declaration last year.

There are hints the UK would accept tariffs and quotas in areas of its choosing if they allowed it to walk away from other conditions.

Ultimately the ‘moment of truth’ will come at the EU summit in October when the bloc will want to see a draft agreement.

TRUMP DUMPED?

In the US, which is grappling with severe outbreaks of coronavirus across several states, investors will eventually have to switch their focus to the presidential election in November.

The latest Financial Times poll calculator puts Joe Biden on 287 electoral college votes against 142 voted for Donald Trump, with support for Biden on both coasts far outweighing Trump’s narrow central southern base.

Interestingly, key states such as Florida and Michigan are leaning towards Biden while Texas, the second biggest state in terms of college votes, is considered a toss-up.

Despite his erratic performance, Trump is pro-business and pro-markets so if the current projections prove to be correct there could be volatility ahead for US stocks.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.