Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineHow Games Workshop became a FTSE 350 star performer

Nottingham-based fantasy miniatures manufacturer Games Workshop (GAW) has been the best FTSE 350 performer over the last five years, providing a total return, which includes reinvested dividends, of 1,600%.

That means a £1,000 investment in 2015 would have turned into £17,000 today, which works out at an extraordinary compound annual growth rate (CAGR) of 76%.

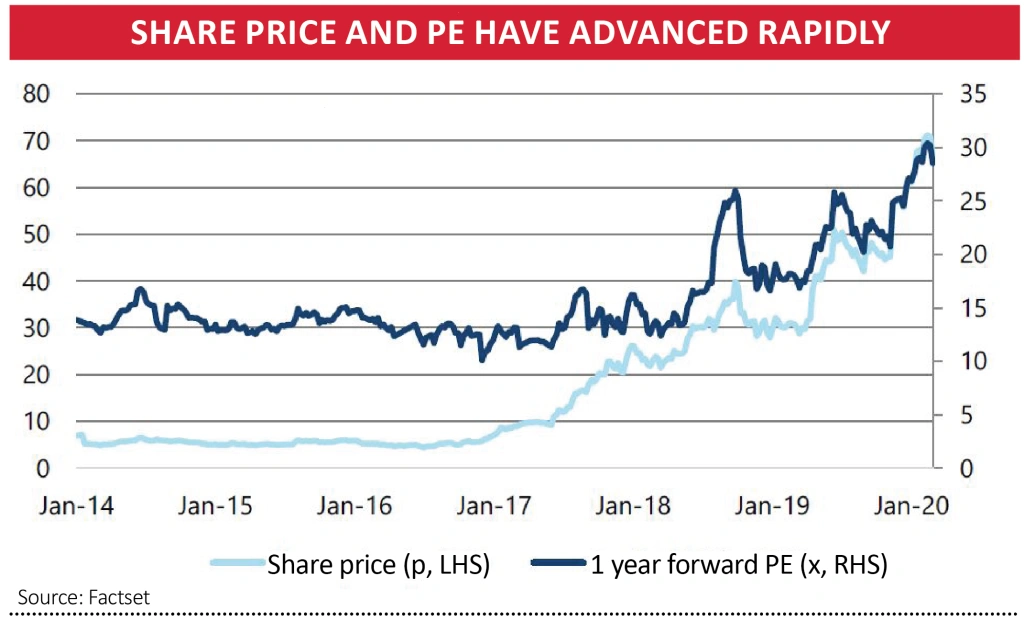

It demonstrates what can happen when strong earnings growth is accompanied by a rising price-to-earnings ratio (PE).

We see Games Workshop as a unique business with strong returns which has arguably only scratched the surface of potential growth opportunities. However, given the growth expectations already embedded in the share price, we believe it is best to wait for a more attractive buying opportunity.

TURBOCHARGING RETURNS

The chart shows that from 2015 onwards the one-year forward price-to-earnings ratio started to rise steeply from around 12 times to the current 29 times. Analysts often use forecast earnings because they are more relevant to investors than historical numbers.

This should always be used with some caution but generally a rising PE means investors expect higher future profits.

In Games Workshop’s case net profits have grown from £12.3 million in 2015 to around £70 million for the year to 31 May 2020, an increase of 5.7 times. If the PE had remained at 12, today’s market value would only be £840 million compared with the actual £2.6 billion.

A higher PE has increased the perceived value of the company significantly.

Before dissecting the financials of the business to understand how the company has achieved such impressive growth, we explain some of the unique aspects of the business that add up to what famed investor Warren Buffett has called an economic moat and which the company calls its ‘Fortress Moat’.

ECONOMIC ADVANTAGES

Games Workshop is categorised a retailer inside the FTSE 350 Leisure Goods sector, but in reality it is much more.

Traditional retailers are intermediaries between suppliers of products and consumers. They apply a small mark-up for providing this service.

However Games Workshop is vertically integrated, which means it designs, manufactures and distributes directly to the consumer via its 529 Warhammer stores, online customers and through over 6,000 trade partners. Effectively it controls all parts of the value chain, from design, manufacturing and distribution.

Who is Games Workshop?

Warhammer and Warhammer 40,000 is a miniature wargame based on Warhammer Fantasy Battle, the most popular wargame in the world. The game is set into the distant future where a stagnant human civilisation faces hostile aliens and malevolent supernatural creatures.

The company doesn’t sell ready-to-play models but rather it sells boxes of model parts which enthusiasts are expected to assemble and paint. The tools, glue and paints are sold separately. Effectively the company serves and inspires millions of table-top hobbyists across the world.

Board gaming is a global market growing at an estimated compound annual growth rate (CAGR) of 9% and is expected to be worth around $12 billion by 2023 according to consultancy Statista.

The company employs a 200 person design studio which creates all of the firm’s miniature designs, artworks, games and publications. That adds up to over 30 years of intellectual property rights. As we will elaborate later, the business is starting to reap some meaningful revenue from selling TV and production rights to its products.

Focusing on fantasy characters instead of historical ones means future product innovation is only limited by the designers’ imaginations and provides endurance to the brand, a valuable trait.

Investing in the best manufacturing and tooling equipment means the company makes the best quality and most detailed miniatures on the market which protects the business from inferior imitators. In addition the firm is much larger than its nearest rival which means it can manufacture the products more cheaply.

Finally, controlling the whole supply chain means the company has flexibility to set prices. Once made all products are distributed from a warehousing facility in Nottingham to stores, trade partners and online customers or via hubs in Sydney and Memphis.

STRONG RETURNS

The financial consequence of possessing a ‘Fortress Moat’ and having control over the entire value chain is that the company achieves a very high return on capital employed (ROCE). According to company data the ROCE hit 111% last year, one of the highest in the UK market.

This means the company can easily self-fund future growth from internally generated cash with the flexibility to pay consistent dividends. Since listing in 1995 the company has grown its dividend by a CAGR of 9.5%.

WHAT HAS DRIVEN SUCH STRONG GROWTH?

The short answer to what is behind the firm’s rapid expansion was eloquently articulated by small cap fund manager at Aberdeen Standard, Harry Nimmo who told Shares ‘new management made it fit for the internet age’.

Having joined the company in 2008 and served time as chief financial and operating officer, Kevin Rowntree took up his current chief executive role in January 2015.

Stronger revenue growth can be traced back to the 2016 launch of online hub WarhammerCommunity.com, which attracted 5 million users and 70 million page views over the first two years.

In the 2019 half-year report the company highlighted 48% growth in users accessing its online hub while sessions per user also increased, ‘meaning our fans are visiting more often and are more engaged with the content’.

At least one new video is uploaded to Warhammer TV every day across YouTube and Facebook platforms, detailing how to build and paint models as well as unbox the kits. This is a marked improvement from 2016 when only 40 videos were uploaded in a year.

Twitch is a streaming service that allows users to watch live and pre-recorded recording of a broadcaster’s video game. Warhammer is featured heavily with a busy programme that includes ‘Hang out and Hobby’ which broadcasts from 4pm to 7pm during weekdays and live content at 3pm every day bar Wednesday.

LICENSING DEALS

According to some analysts there was a step change in the company’s approach to licensing from around 2015, which has resulted in income increasing from £1.5 million to around £16 million in the year to 31 May 2020.

All in all, successful social media engagement has not only resulted in the company selling more products to its existing customer base but has also attracted new, younger hobbyists.

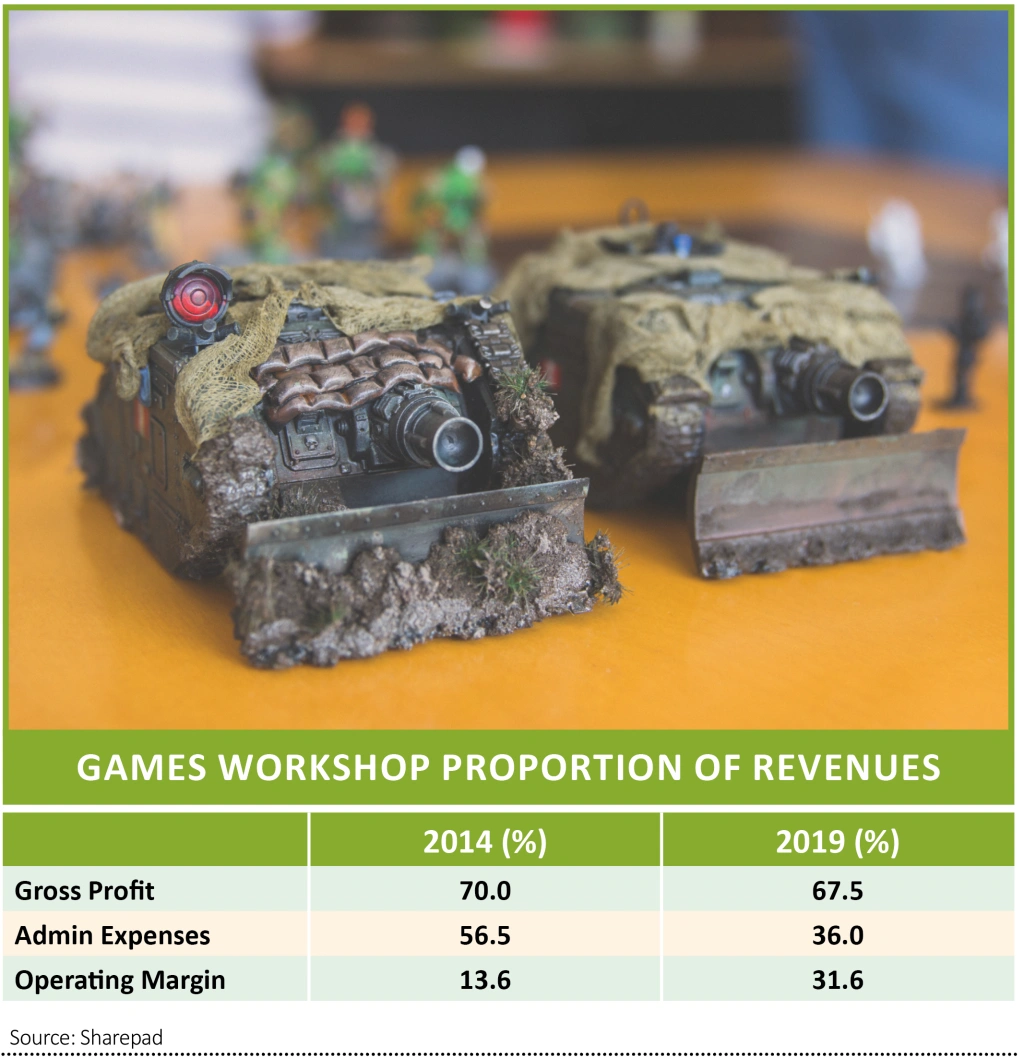

Revenue has gone from £119 million in 2015 to around £270 million in 2020. However operating profit has increased five-fold.

The table shows the operating margin has more than doubled over the last few years as more revenue was captured as profit. This is due to management keeping a tight lid on administration expenses which have not kept pace with the expanding size of the business.

As a proportion of revenue, they have fallen by over a third, allowing operating margins to expand appreciably.

While the company should be applauded for good financial controls, it has also benefited from an increase in volumes going through the manufacturing and warehouse facilities at no marginal cost.

One underappreciated aspect of Games Workshop’s business model is the huge fan base that in effect acts as a free sales and marketing team. The move to online has accelerated this effect because of the viral nature of social media, where videos, podcasts, interviews and tutorials spawn yet ever increasing content.

In turn, discussion among users drives awareness, attracting new hobbyists, creating a virtuous circle.

HOW FAR CAN OPERATING MARGINS EXPAND?

A key consideration for investors is to make an assessment of how sustainable the current economic advantages enjoyed by Games Workshop can continue.

Analysts at Jefferies believe sales growth momentum will continue for the next decade, eventually fading to around 3% a year by 2030. Recognising the benefits from operational leverage they expect the operating margin to continue to expand to 40.5%.

The higher margins are also expected to get a boost from increasing, higher margin license revenues.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.