Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWinners and losers among housebuilder, portal and estate agent shares as housing market is defrosted

The housing market is emerging from hibernation but as investors in directly related sectors like housebuilders and estate agents count the cost of lockdown they have seen a significant divergence in share price performance.

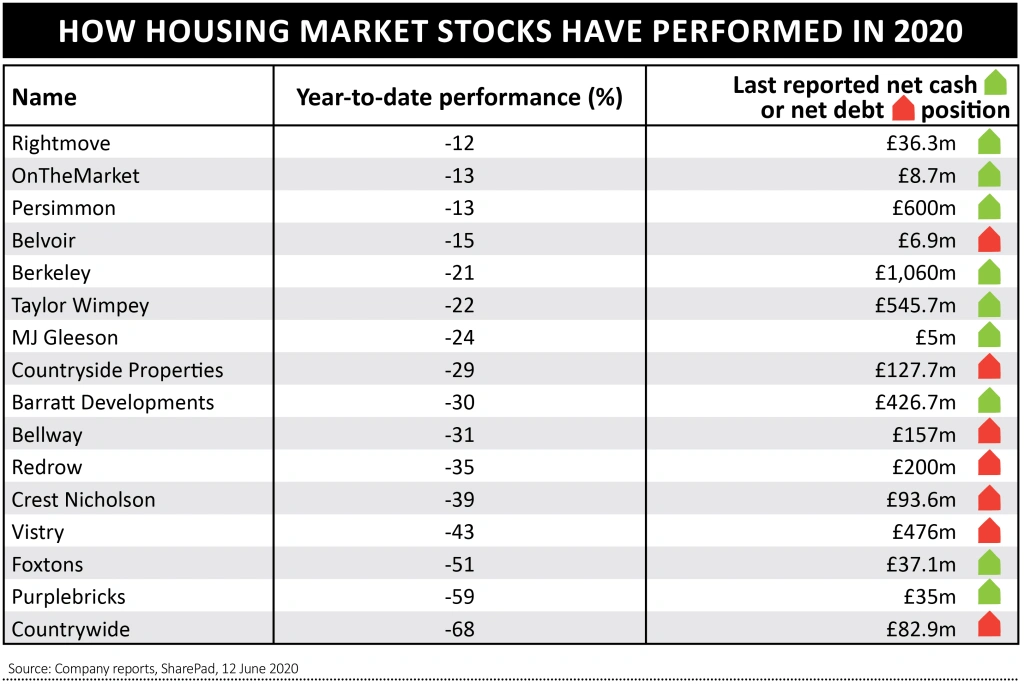

There are a number of factors behind these disparities. A look at the table of year-to-date performance suggests that financial strength has been a clear dividing line but there are other reasons why some stocks have held up reasonably well while others have seen much more substantial falls.

Sifting through the wreckage with an eye on the potential recovery in property activity, we have identified the best housebuilder shares to buy now as well as updating our views on two constituents of this space which we have written about positively in the past.

REMARKABLE LEVEL OF RESILIENCE

In the context of lockdown the UK housing market has actually been remarkably resilient and this can be seen in a number of data points.

House price data has been pretty ropey but not disastrous in the circumstances. The latest figures from the Royal Institution of Chartered Surveyors (RICS) showed 32% of estate agents reported a fall in property prices in May – the lowest point for the gauge since 2010.

However, beneath that headline there were reasons for optimism with RICS also revealing that new buyer enquiries recovered from -94% in April to just -5% in May.

Property portal Zoopla says property sales in England have swiftly rebounded to the same levels they were at shortly before lockdown as pent-up demand has been released. Since restrictions were lifted Zoopla noted a 137% increase in the volume of new sales agreed, though Scotland and Wales remain in deep freeze for the time being.

SHIFTING BUYER PREFERENCES

Site data and a user survey from fellow portal Rightmove (RMV) suggests there is a preference for houses in rural locations and with good transport links – perhaps reflecting a shift to working from home.

This may have negative implications for the London market, which may explain why estate and lettings agent Foxtons (FOXT), focused on the Capital, is a real laggard on the stock market despite a net cash balance sheet.

The theme of resilience is also reflected in a fairly low level of cancellations among the big volume housebuilders.

Several housebuilders said they continued to complete transactions and secure new reservations through lockdown as they adapted to social distancing both in terms of construction activity and online viewings of properties.

One of the better performing property-related stocks in the space, Persimmon (PSN) has noted that cancellation rates have remained in line with historic trends. Like affordable housebuilder

MJ Gleeson (GLE), Persimmon is arguably better placed in recovery with its last reported average selling price of £244,500 towards the lower end of the market.

Our timing in flagging Persimmon’s income attractions in late February was poor, particularly as like nearly all of its peers it subsequently suspended dividends. However, we remain comfortable with the view that it has good prospects for recovery as the market kicks back into gear, supported by its robust balance sheet.

FINANCIALLY STRONG

Even more robust financially is Berkeley (BKG) which has the kind of resources many companies could only dream of, sitting on £1bn-plus of net cash at the last count.

These deep pockets should enable Berkeley, whose chairman Tony Pidgley is seen as one of the shrewdest operators in the sector, to add to its land bank at an opportune point in the cycle when competition is low.

Another relative outperformer, Taylor Wimpey (TW.) outlined plans for land acquisition in its latest update (5 June) as it revealed that in the nine weeks since the start of lockdown it had seen cancellations at just 5% of its private order book (compared with 6% for the equivalent period in 2019).

The land acquired cheaply in the wake of the financial crisis was one of the reasons why the sector has been so profitable in recent years, along with the Help to Buy scheme, strong supply-demand dynamics and the easy availability of affordable mortgages.

PROPERTY PORTALS

Beyond the housebuilders, shares in property sites Rightmove and OnTheMarket (OTMP:AIM) have held up relatively well, perhaps because investors believe estate agents will continue to spend money on advertising properties as the latter need to facilitate transactions to generate a key source of income.

Lettings and estate agency operator Belvoir Lettings (BLV:AIM) has done better than some of its peer group on the stock market – with its lettings business and franchise model providing some protection from a collapse in transactions.

As FinnCap analyst Guy Hewett notes on Belvoir: ‘Early indications for April trading are that the franchise networks have shown considerable resilience.

‘Less than 5% of tenants are in arrears on their rent, only a small increase on the 2% seen in normal times, and sales transactions of around a third of usual levels were able to complete.’

We featured Belvoir in ‘Our six best small cap ideas’ article on 6 February and we continue to rate the stock as a ‘buy’.

THE HOUSEBUILDER TO BUY NOW

Bellway (BWY) £26.35

The company recently confirmed that trading had been relatively strong through lockdown. It has completed on 708 units since 23 March and it flagged a pick-up in interest since reopening its English sales centres on 1 June.

Selling prices have remained solid according to the company and the order book remains above £1.5bn.

Net debt of £157m is very manageable and the shares are also cheaper than rivals with net cash on their balance sheets. Based on forecasts from Liberum the shares trade on a price-to-net asset value ratio of around one.

While dividends are off the table for the time being, its track record suggests this will likely be a temporary phenomenon. Liberum notes Bellway sustained its payout through the financial crisis.

MORE STRETCHED

One of the worst performers in the space on the stock market has been estate agent Countrywide (CWD) which is lumbered with net debt of £82.9m at the last count. The company was not helped

by the collapse of the sale of its troubled commercial arm Lambert Smith Hampton. It is currently suing the buyer after the deal fell apart at the final hurdle.

Countrywide’s less robust financial position is a trait it shares with other relative underperformers.

In hindsight Vistry’s (VTY) acquisition of Galliford Try’s (GFRD) regeneration and housing divisions was poorly timed, stretching the balance sheet and exposing it to integration risks. Its shares have lagged the peer group.

One of Shares’ key selections for 2020, Redrow (RDW) has also disappointed. Again this is likely to be linked to its net debt position of around £200m which left it more exposed to the unprecedented situation created by the pandemic.

Our December 2019 article picking Redrow was based on the premise that the UK’s economy would bounce back and that its shares were attractively valued. The former has clearly been knocked off course by Covid-19.

Redrow’s pricing levels are closer to the top end of the market, something it shares with Crest Nicholson (CRST) whose stock price has significantly underperformed the former in the past three months.

Elsewhere, Purplebricks (PURP:AIM) has seen its stock sold by several major institutional investors, including the offloading of the stake held by Neil Woodford’s collapsed equity fund. The company’s weak share price performance is probably also a hangover from a very difficult 2019 when it had to effectively abandon plans for overseas expansion.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Feature

First-time Investor

Great Ideas

Investment Trusts

Money Matters

News

- Valuation and competition pose a threat to Zoom's soaring share price

- What US stimulus and infrastructure news means for markets

- Private equity investors ready to swoop as they sit on record cash pile

- Time to be more cautious on this year’s biggest biotech winners

- Best of the Best’s success attracts takeover interest