Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineEU gears up for its next challenge

This week’s online meeting of the European Union’s members to debate the proposed €750bn Covid-19 recovery plan is vitally important economically and politically.

For progress to be achieved and help offered to those who need it, amid predictions that EU GDP will drop by 8% to 12% in 2020, all 27 nations must agree on:

• The amount of money to be spent, on top of an EU budget of some €1.1trn (itself a matter of some friction between member states).

• The conditions for awards of the capital available, which appear to include both green and digital criteria for would-be recipients.

• How the money is to be spent, and the mix between loans and grants.

• How and when the money is to be repaid and over what time period, starting in 2027.

The discussions are therefore an opportunity to present a united front, tackle the viral outbreak and shore up the EU edifice at the same time, just as the Brexit negotiations with the UK start to heat up again.

Coming of age

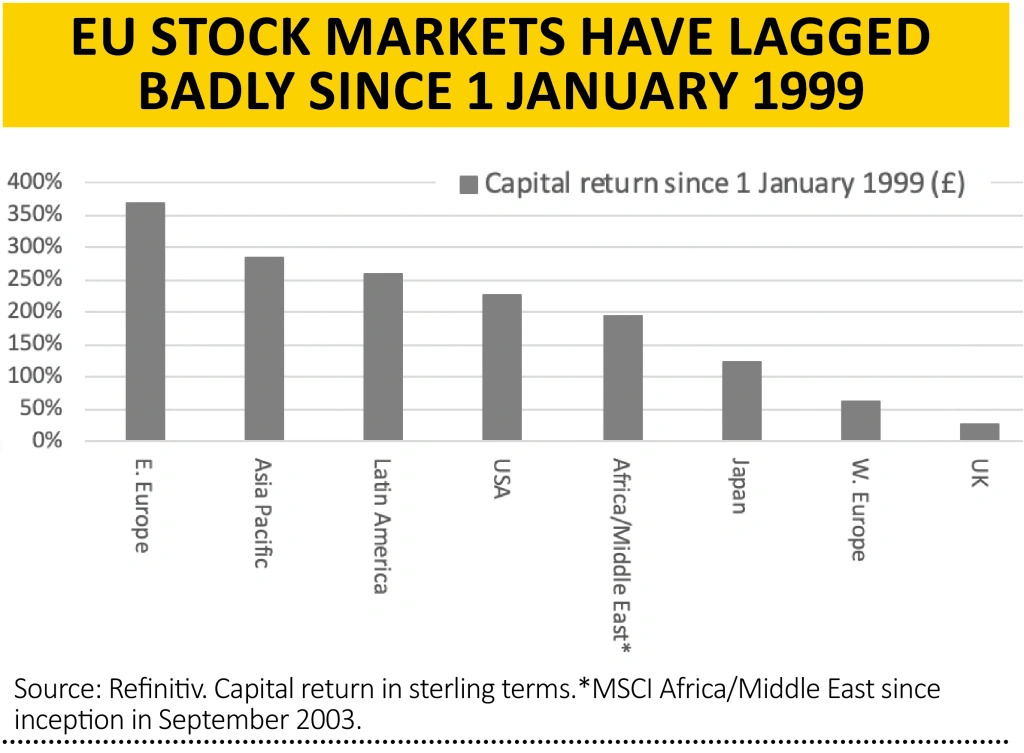

From the narrow perspective of investing in stock markets, it seems that global capital is yet to be fully convinced by the merits of the European project. The sterling-denominated performance of the Stoxx Europe 600 index ranks seventh out of eight in capital terms since the euro came into being on 1 January 1999.

This poor performance may reflect the lingering effects of the debt crisis that first boiled over a decade ago, as well as the difficulties of providing a solid financial platform with which to support political union, in the absence of fiscal and banking union to support a single currency and unified monetary policy.

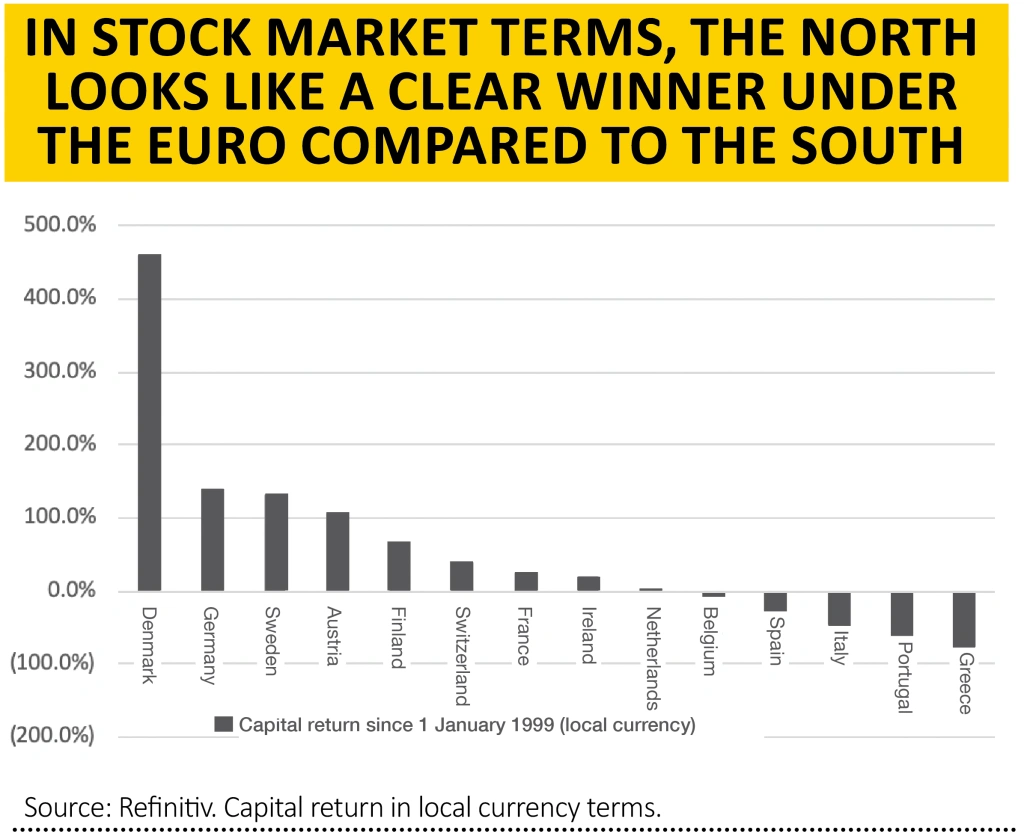

It may also reflect the different aims and needs of the 27 member states which are again becoming apparent as the recovery plan and budget come up for discussion.

The most serious questions of the plan are being asked by the so-called ‘Frugal Four’ of Germany, Denmark, Austria and Sweden.

Failure to agree, in the twenty-first year of the existence of the single currency, would raise existential questions about euro and the EU’s purpose and usefulness. Government is there to provide assistance in times of crisis above all others and were the EU to fail to offer help to those nations which Covid-19 has treated most cruelly – notably Italy and Spain – then scope for further local disaffection with the supra-national powers in Brussels is considerable.

These countries suffered the most in the wake of the debt crisis that started in earnest just under a decade ago.

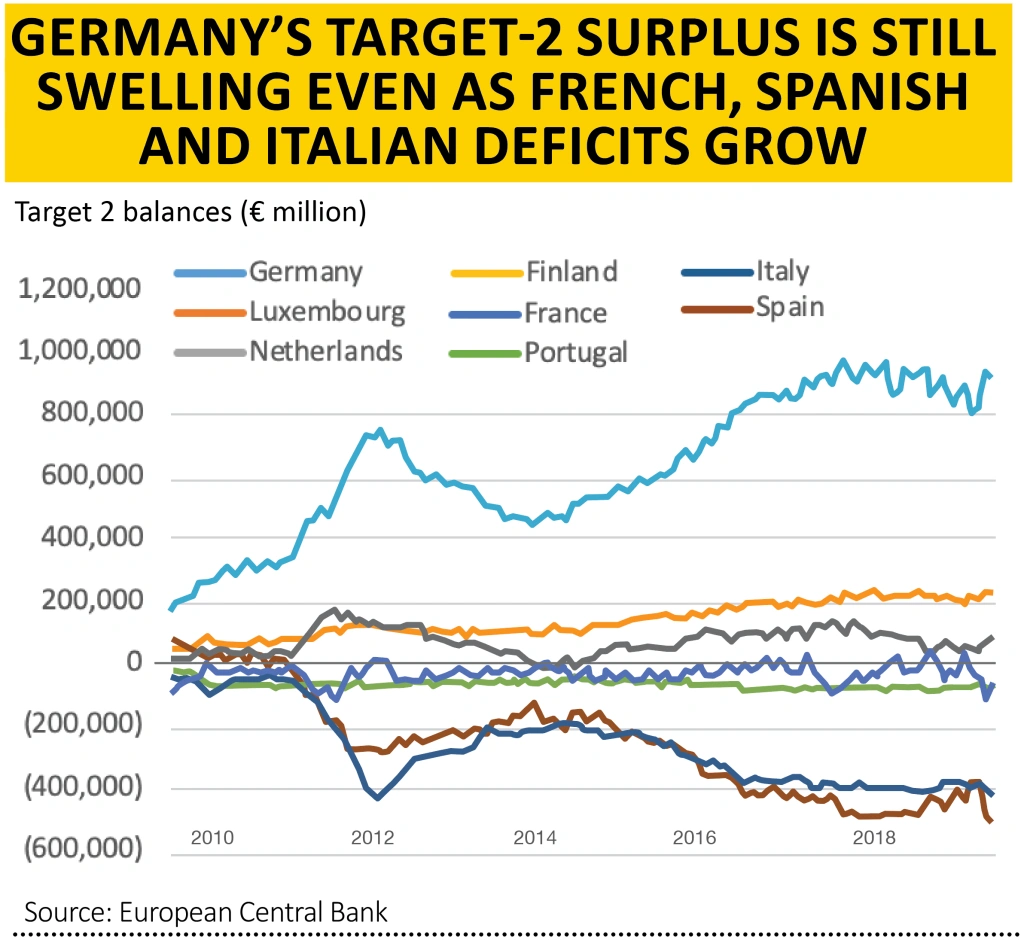

This North-South divide can be seen in another way, via the Target-2 payments mechanism.

Target stands for Trans-European Automated Real-time Gross Settlement Express Transfer system. In essence the system is there to help balance trade flows but it could also reflect capital flows. Supporters argue that the Target-2’s smooth functioning shows that it balances out the capital needs of the EU’s member nations.

Sceptics assert that Target-2 merely highlights huge capital flight from the South to the North and Germany in particular.

No harm is done – unless an EU member defaults or drops out of the monetary union. Those that have a positive balance are on the hook for the deficits of the member in the red.

This may be why the €750bn recovery plan alarms the Frugal Four, as they fear it could be the first step to debts being aggregated and funded at EU level, potentially leaving them to subsidise what they see as the spendthrift southern members.

The European Central Bank is doing its bit to keep the plates spinning, as it holds headline interest rates at zero and its €650bn expansion of the Pandemic Emergency Purchase Programme (PEPP) to take the total to €1.35trn. As elsewhere, that quantitative easing (QE) largesse is boosting equity and bond markets to create some kind of feel-good factor.

But whether QE provides a lasting solution is unclear. The cost of meeting each crisis – 2007-09, 2011-15 and now Covid-19 – is becoming ever greater each time.

The euro is under less scrutiny than it would be, even if has lost 84% of its value against gold since its launch, because sterling, the yen and the dollar are also at the mercy of identical monetary policies (and all are down by more than 80% against the metal, too).

Investors may not welcome another round of patch fixes and last-minute fudges from the latest round of talks, especially if they only serve to stoke further support for anti-EU parties in the South, should those nations start to feel neglected again.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Feature

First-time Investor

Great Ideas

Investment Trusts

Money Matters

News

- Valuation and competition pose a threat to Zoom's soaring share price

- What US stimulus and infrastructure news means for markets

- Private equity investors ready to swoop as they sit on record cash pile

- Time to be more cautious on this year’s biggest biotech winners

- Best of the Best’s success attracts takeover interest