Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWhy the UK market has lagged behind

At the time of writing, the FTSE All-Share stands 32% above its March lows, which sounds pretty good, even reassuring, on

the face of it.

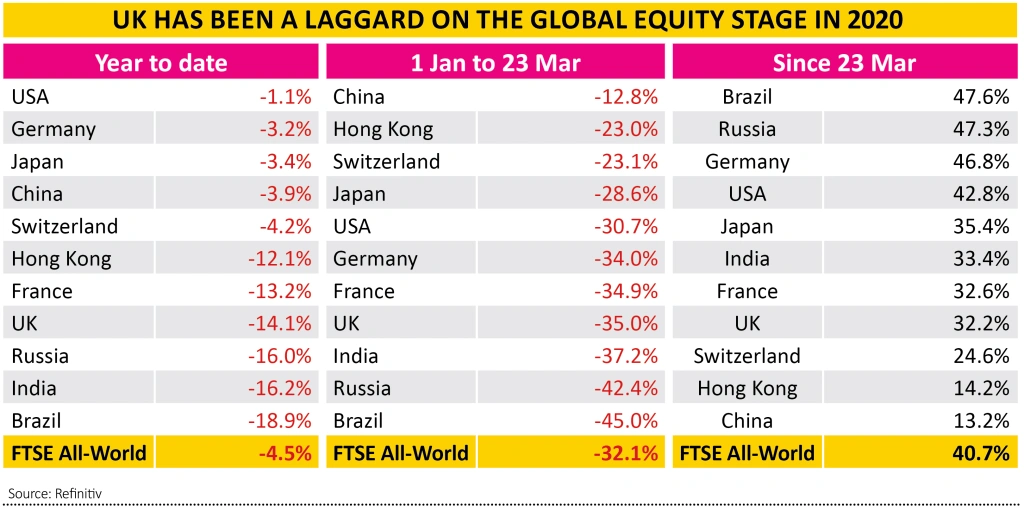

However, that rebound means that the All-Share has still lagged the FTSE All-World over the same period. It also means that the UK has underperformed most major equity markets during the current recovery phase and indeed for the year as a whole.

Cynics may be tempted to argue that this is down to the clarity and efficacy – or otherwise – of the UK’s policy response to the COVID-19 crisis, since the UK has only outperformed India, Brazil and Russia so far in 2020 as a whole, nations where there is also debate over either the quality of either government policy or the local data on the degree of the outbreak.

However, markets usually care little for politics and when they do worry about them they rarely do so for long. The tenure of politicians in office – and their influence – tends to be pretty ephemeral and ultimately corporate profits, cash flows and dividends are the most important drivers of company valuations and thus the indices of which they are a part, although the role of central bank stimulus appears to be getting greater by the month.

No-one would argue that the White House has offered a coherent policy on COVID-19 – or for that matter many other pressing issues – yet the US sits at the top of the performance tables for 2020 to date. And even if questions are being asked about Russia and Brazil, it is not stopping their stock markets from being the best performers since the year’s lows in late March.

Other factors above and beyond politics and COVID-19 could therefore be at work. A huge rally in oil and improvement in other commodities prices may be helping Sao Paolo’s and Moscow’s markets while America’s well-documented strength in areas such as technology and biotechnology is being reflected in equity returns from the S&P 500 overall, as well as certain high-profile companies.

The industry mix within an index is therefore an important factor and this is something which any investor must consider when they are perhaps contemplating buying a tracker fund or even an actively-managed one; in the latter case they will need to assess the manager’s views on the major sectors within a country and also check whether the predominance of certain industries, such as say oil or defence or tobacco mean there are ethical or other grounds for giving somewhere a wide berth.

League tables

Some clues to the UK’s relative underperformance can be found in the FTSE All-Share index’s make up and which industrial groupings have done best and worst in 2020.

Leisure Goods (which is essentially Warhammer gaming specialist Games Workshop (GAW) is the top performer, which relatively defensive areas such as Pharmaceuticals & Biotech, Food & Drug Retailers, Household Goods, Personal Goods and Tobacco also among the top ten. The laggards include some areas which have been hit hardest by the lockdown, such as Travel & Leisure (and by association with that Aerospace & Defence), as well as Real Estate Investment Trusts, by dint of landlords’ exposure to retailers.

Some of those sectors have come roaring back since the late-March low, in the view that if revenues are down nearly 100% then it cannot get much worse and if it cannot get much worse then it will soon start to get better. Hopes for wider, global economic upturn are also giving fresh life to sectors such as Mining, Industrial Metals and General Industrials.

But the underperformers which seem to be weighing most heavily on the All-Share include the oil companies (down nearly 30% for the year) and financials, where non-life insurance (presumably owing to its business continuity, event cancellation and other outbreak-related exposures) and banks are down near the bottom of the performance tables for 2020 as a whole.

Financials represent 17% of the FTSE All-Share’s market cap, the oil firms 10% so a quarter of the index is in investors’ doghouse right now. Other substantial weightings are the index-leading 17.4% at Consumer Staples and 12.8% at Healthcare. They are both defensive in nature so if global markets are going to stay in ‘risk-on’, recovery mode, then the UK could continue to less well relative to other geographic options which are more sensitive to the global economy and trade flows, such as Germany.

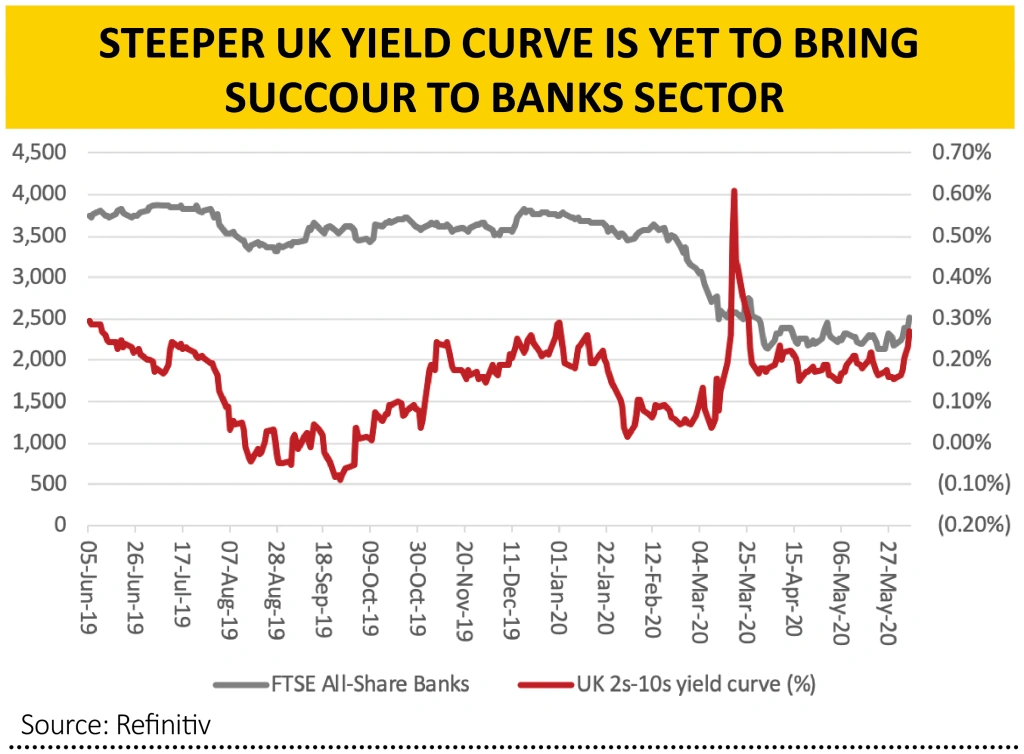

As a final point, the rotten performance of the banks is eye-catching. It is the single-worst performing sector since the recovery began in March. This seems odd, as the yield curve has steepened for much of the last nine months and the wider gap between the UK two- and ten-year Government bonds would normally herald higher lending margins.

Perhaps this reflects concerns that banks are being used as public utilities during the crisis, with the forced scrapping of dividends and obligations to offer fresh loans, or at least payment holidays, to corporations and consumers alike, almost regardless of whether the money can be finally paid back. Throw in HSBC’s (HSBA) and Standard Chartered’s (STAN) political discomfort in Hong Kong and China, and it is indeed a grim time to be a bank.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.