Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

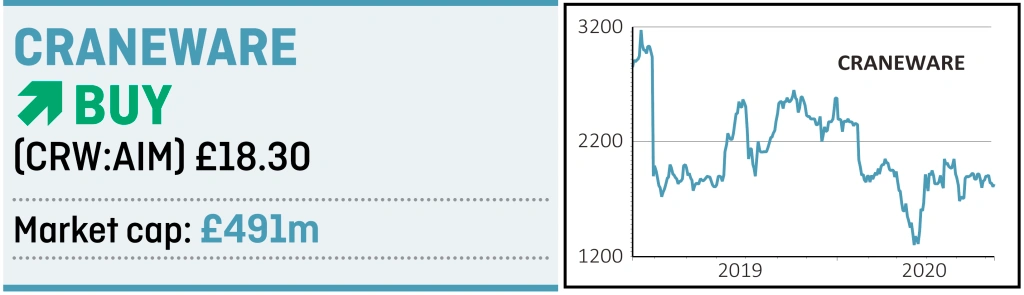

magazineDrive for efficiency in US healthcare is great for Craneware

US healthcare organisations are embracing new technology to navigate the complexities of a post-coronavirus world, and this is great for made in Britain software firm Craneware (CRW:AIM).

The company uses automation and analytics tools to highlight operational and financial risks, identify new income opportunities to US hospitals management and improve patient experience. The financial health of all US hospitals is already faced with challenges

as the healthcare system across the pond transitions to a value-based approach.

The continued imposition of regulations on pricing transparency from the Trump administration and the pressures from the pandemic are likely to reinforce its place as a key trusted hospitals technology partner.

Craneware estimates that it can help an average 350-bed hospital tap an extra $22m of revenue a year.

DE-RATING IS TEMPORARY

The stock had been hit hard prior to the Covid-19 outbreak because of a new sales slowdown and the loss of a hospitals network customer, the latter of which was due to a revolving management door at the client meaning Craneware’s tools were never fully integrated into its system. That implies a one-off issue rather than anything more sinister.

The brake on sales was caused by the introduction of Trisus Health Intelligence, Craneware’s cloud-based analytics platform that launched in 2019. Developed over many months, it combines the best of the firm’s core price, cost and compliance features with new financial, operational and clinical data tools.

Those extra features and complexity mean demonstrating the platform’s scope to slash costs, drive new revenue streams and speed up administration takes that bit longer, something to be aware of but already partly smoothed out.

Still, on a premium rating, the impact on the share price was dramatic, slashing the June 2021 price to earnings multiple from

50 to today’s more interesting 32.

COMPELLING LONGER-TERM STORY

Demonstrating that this was all temporary will obviously be vital in getting the share price going again, but Craneware has a hard-earned reputation for operational excellence to lean on. The improvement in sales reported in March suggests that the business strategy is back on track.

Dominating an exciting niche, deriving only recurring revenue on average five-year contracts, and enjoying an entrenched competitive position at the top of its industry, Craneware is a compelling proposition for investors comfortable taking a bit more risk for the better growth implied.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.