Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

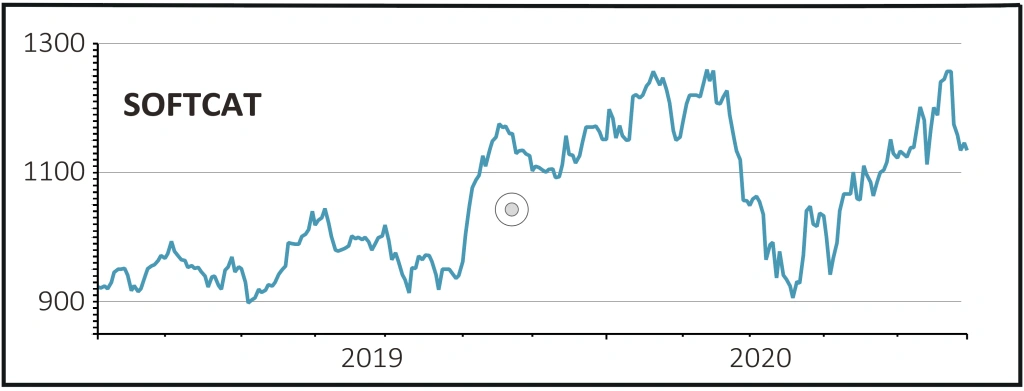

magazineRelative outperformance impressive from Softcat

SOFTCAT (SCT) £11.41

Gain to date: 18.9%

Original entry point: Buy at 959.5p, 1 August 2019

Software reseller and IT advisor Softcat (SCT) continues its excellent performance both operationally and in share price terms, even if its latest update was tinged with a slightly more cautious tone.

The 26 May third quarter update was free of specific numbers, as is usual, but noted ‘satisfactory’ trading during the period to 30 April, and flagged revenue, gross profit and operating profit growth while maintaining cash generation at normal levels.

That’s all very encouraging but the ‘high degree of uncertainty’ in the coming months and an acceptance that Softcat is ‘not immune to the challenges faced by the wider economy’ gave investors pause for thought.

Given that the third quarter bridges the UK lockdown period, it seems likely the company enjoyed a typically busy March, but a much slower April and May.

Those are certainly the implications drawn by analysts at Jefferies, who have decided to trim profit forecasts by £4m this year to 31 July, ‘to reflect the impact of slower trading’ in the second half.

That implies £91.1m for the full year versus £95.1m previously, although it is interesting that gross profit per customer estimates, a key performance indicator for Softcat, were left unchanged.

SHARES SAYS: Lockdown is the ultimate test and Softcat remains a relative outperformer in a world of declining revenues and earnings.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.