Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineClothing retail post-corona: smaller, faster, cheaper

Clothing retail is one of the most difficult businesses to get right at the best of times. Low profit margins, intense competition, changing consumer preferences, the weather and any number of smaller challenges can upset the plans of even the best operators.

The coronavirus has had a devastating short-term impact and in the long term retailers will have to adapt by improving their online offering and their understanding of customers.

RETAILERS WERE ALREADY STRUGGLING

It’s no secret that retailers – especially those on the high street – were facing tough times before the crisis.

Last year was particularly brutal with more than 50 firms entering administration including Bonmarché, Debenhams, House of Fraser, Karen Millen and Coast, LK Bennett, the UK arm of Mothercare, Office Outlet (formerly Staples) and Select.

Since the turn of the year, fashion chains Autonomy, Cath Kidston, Laura Ashley, Oasis and Warehouse; luggage retailer Antler; department store Beales; rent-to-own retailer Brighthouse; and footwear chain Johnsons have also gone into administration, leaving hundreds more empty sites on our high streets.

According to the mid-May Opinium-Cebr Business Distress Tracker, one in five businesses in the wholesale and retail sector said they were at high or moderate risk of insolvency and might not survive another month of lockdown.

High streets, shopping centres and out of town retail parks have all suffered the same problem – a lack of people coming through the doors.

Non-food retail sales have been shrinking in value terms by an annual rate of 5% for more than a year according to the British Retail Consortium (BRC), but in-store non-food sales have been falling at a rate of 11.5%.

CHANNEL SHIFT

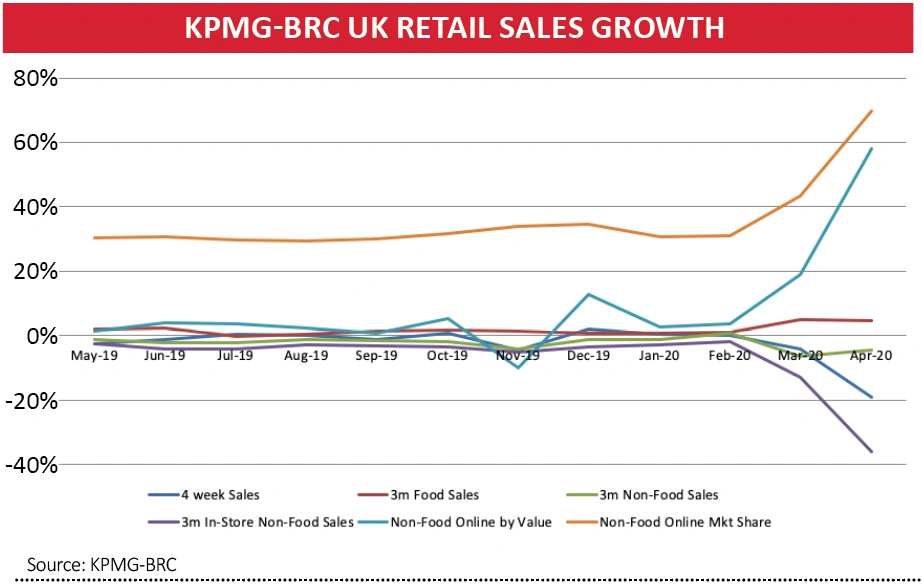

In contrast, online non-food sales have been growing by 4% to 5% a month for the last year with online making up around 30% of non-food spending.

After the ‘Boris bounce’ that followed December’s election, in-store non-food sales briefly turned positive in January and February, but March’s sales were shocking with the BRC reporting overall spending down 27% in the last two weeks of the month due to the closure of ‘non-essential’ shops.

April was even worse, and in-store non-food sales were almost non-existent due to the enforced closures. Instead, online spending on non-food items soared nearly 60% by value and the market share of online sales nearly hit 70%.

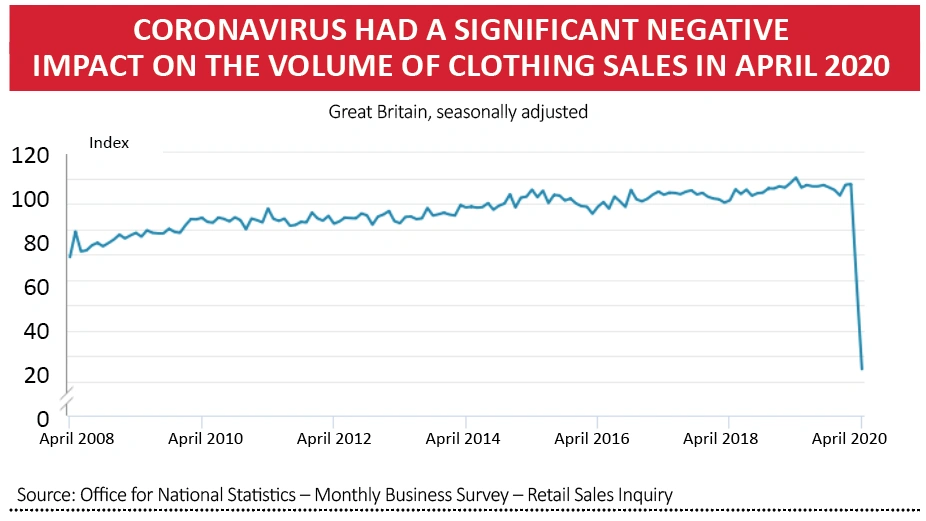

Figures from the Office for National Statistics (ONS) paint a similarly dire picture, with non-food stores registering their sharpest monthly fall in volume sales on record. Textile, clothing and footwear stores reported the biggest fall at 50.2%.

It’s obvious from most retailers’ trading updates that having an online sales channel – even if it isn’t that good – has been better than not having one.

By its own admission, Marks & Spencer (MKS) has been behind the curve with its web offering, and while online sales haven’t exactly blown the doors off in 2020 they have been the only significant contributor to the clothing business.

For chief executive Steve Rowe, the crisis ‘has illustrated the need to be leaner and more integrated to compete with online pure plays’.

Next (NXT), which had to close its online operations briefly, has seen web sales recover sharply although overall sales are still a fraction of their pre-crisis levels.

Primark, part of Associated British Foods (ABF) and one of the UK’s biggest fashion retailers in terms of sales, was ‘squarely in the path of the pandemic’ to quote chief executive George Weston.

From making monthly sales of £650m a month, since 22 March it has sold nothing at all because it doesn’t have an online channel. The margins on most of its items are so small that when shipping and returns are included, it isn’t worth it financially.

‘One third of clothes bought online get returned,’ says John Bason, finance chief. ‘That means someone has to pick it up, someone has to deliver it, someone in the store has to take it back, refold it. It doesn’t work at the lower price point.’

Although some of its European stores have reopened, and the average customer spend or basket size is higher than pre-crisis, that alone won’t make up for the massive shortfall in sales.

At some point Primark is going to have to consider the multi-channel option if it isn’t to be left behind.

THE NEXT NORMAL

The big worry for retailers is that when restrictions on store openings are lifted on 15 June (or 1 June for outdoor markets), aside from issues of hygiene and social distancing, will customers actually bother venturing out, or has the pandemic accelerated a trend which was already in progress and is the massive shift to online irreversible?

If the ‘next normal’ is for only 30% of sales to happen in-store, how can retailers entice customers back? Also, how quickly will consumer confidence return, and what will the crisis have done to household savings and levels of indebtedness?

As Julie Palmer, partner at insolvency firm Begbies Traynor (BEG:AIM), put it, ‘The end of lockdown is not the light at the end of the tunnel for retailers. When lockdown is over the return to normality will not be like flicking on the lights, it will be like dimmer switches turned at low speed.’

Another concern is the shift in customer loyalty under lockdown. According to McKinsey, up to 40% of consumers have switched stores and brands during the crisis and many may choose to keep their new habits.

One theory is that stores could reflect the tastes of local consumers by adapting their products, pricing and promotions to each market. This means firms will need to invest heavily in digital, data and analytics (DD&A), to know their customers better, and radically improve their supply chains.

Retailers typically allocate less than 10% of their total resources to e-commerce, DD&A and flexible supply chains. If they are going to keep their most loyal customers and appeal to new ones, they may need to allocate two or three times their current spend, which will eat into already-slim margins.

POST-CRISIS PLANNING

Most retailers have taken advantage of the Government’s furlough scheme together with business rate and VAT relief, as well as drawing on their banking facilities to finance their day-to-day operations.

All have cut non-essential spending but most still have large amounts of unsold spring and summer stock and have taken large write-downs as a result.

Given that margins may never return to pre-crisis levels, firms need to reset their cost structures as quickly as possible. Those that ‘right-size’ now, and upgrade their online capability, could see faster earnings recovery.

That’s the message coming from Steve Rowe of Marks & Spencer: ‘We have discovered we can work in a faster, leaner, more effective way. I am determined to act now to capture this and deliver a renewed, more agile business in a world that will never be the same again.’

Sonia Syngal, chief executive of Gap, is equally bullish. She says: ‘We continue to use this crisis as an opportunity at every turn. As we leverage our stores as distribution hubs, lean into the meaningful acceleration of our online business and play forward the learnings from our Asia business, we believe we’ll be well-positioned as this crisis subsides.’

Sadly, there are likely to be more retail insolvencies before the crisis passes. Less capacity is good for strong, solvent firms, but it doesn’t solve the bigger conundrum of how to reignite demand.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.