Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

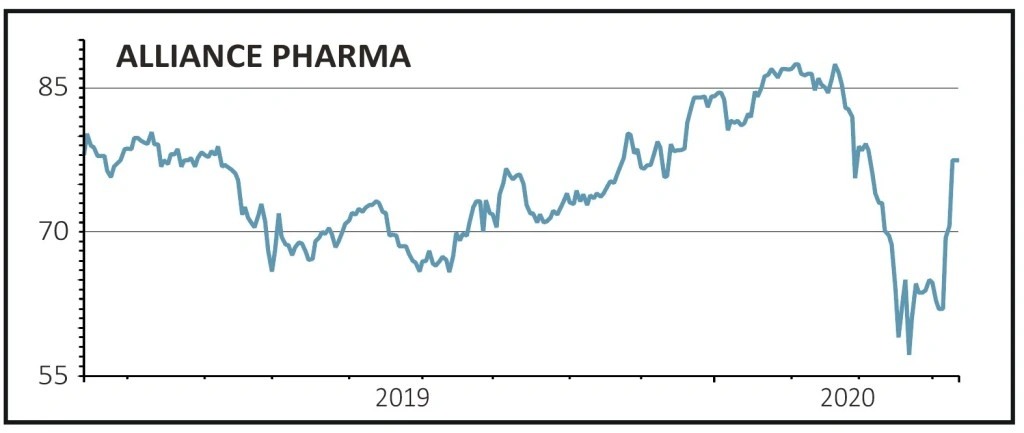

magazineAlliance Pharma remains on growth track

Alliance Pharma (APH:AIM) 77.4p

Gain to Date: +8%

Entry point: Buy at 71.6p, 3 October 2019

Pharmaceuticals firm Alliance Pharma (APH:AIM) continued its trend of strong revenue and profit growth when it reported results for the year ended 31 December 2019 on 7 April, with revenue up 16% to £144m and pre-tax profit up 36% to £31m.

Free cash generation was 81% higher at £29m, which reduced net debt to £59m from £86m last year and resulted in a net debt to earnings before interest, tax, depreciation and amortisation (EBITDA) ratio of 1.48 times, down from 2.3 times.

The international star brands portfolio performed well, delivering like-for-like growth of 30% and these key brands now account for 45% of group revenues, with the percentage expected to increase in the current year.

Local brands delivered a stable performance with revenues of £78.3m (2018: £73m) as the company discontinued a few products as part of the regular review and trimming of the portfolio. Cash generation from these assets is expected to remain strong, reflecting limited promotional investment.

Taking a prudent approach to the ongoing coronavirus pandemic, the board cancelled the final dividend for 2019 to preserve cash.

Remote working practices and a high level of connectivity means the company has seen minimal disruption to the business. The supply chain is said to be holding up well with no material impact in the current year expected.

SHARES SAYS: We remain buyers.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.