Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineBig moment for Disney as streaming service debuts in UK and Europe during lockdown

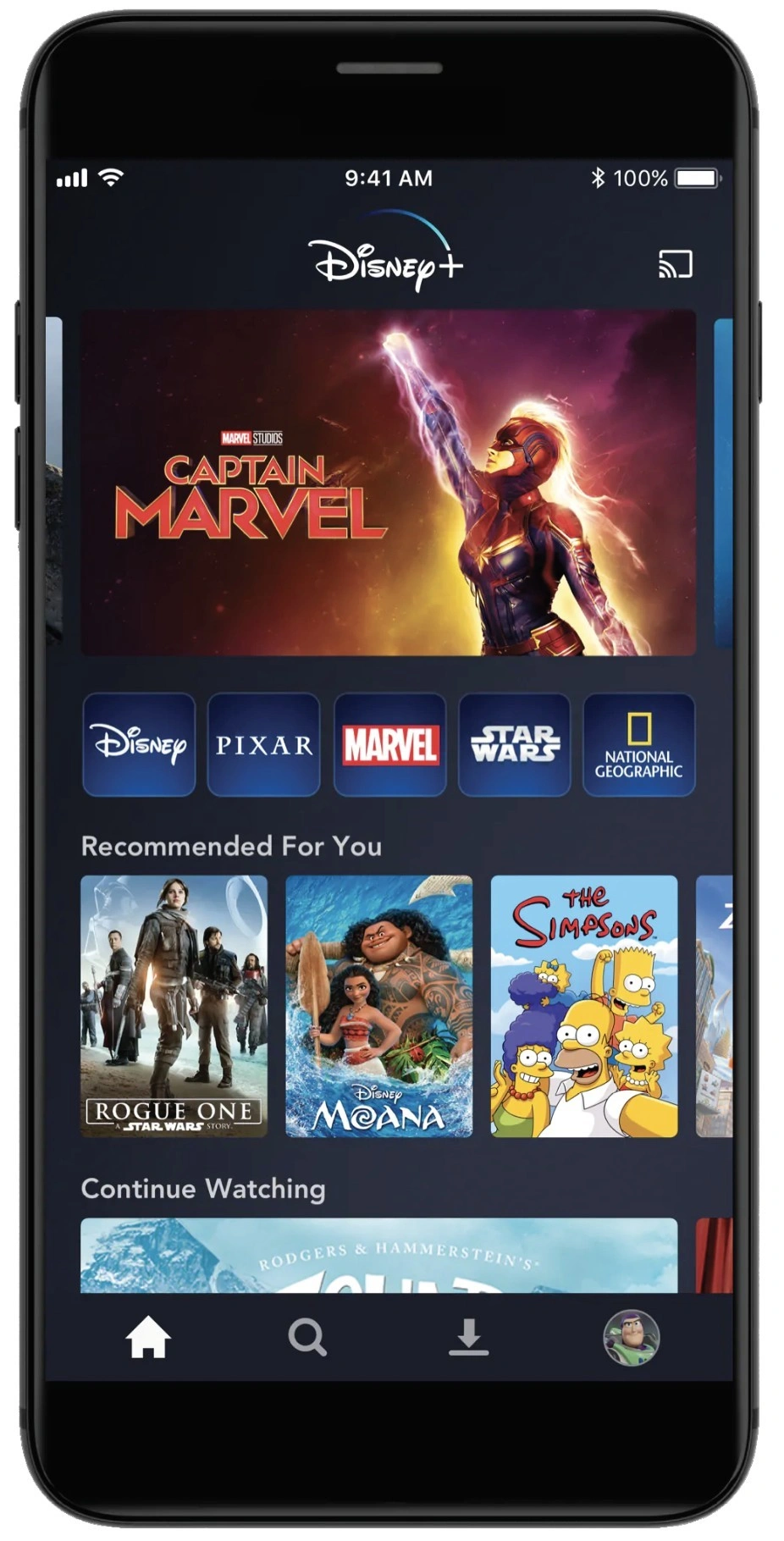

On 24 March the Disney+ streaming service launches in the UK and Europe. This event comes at an interesting time for parent company Walt Disney as an increasing number of people confined to their homes amid coronavirus lockdown might be looking for the distraction provided by a new content platform.

In particular, it could be a saving grace for parents seeking to entertain their children while also trying to work from home.

Disney needs all the positive news it can get given how its theme parks are being negatively impacted by the virus.

CAN DISNEY CRASH THE STREAMING PARTY?

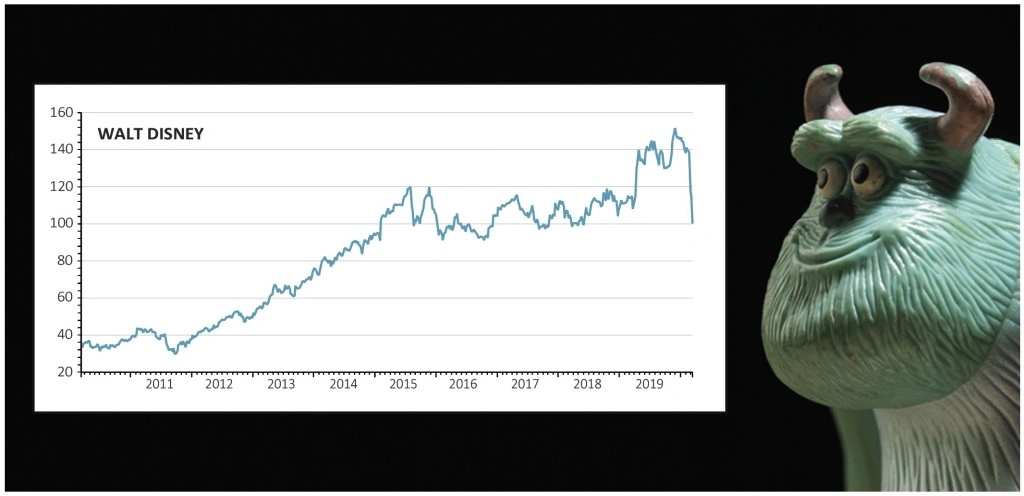

Despite uncertainty over the company’s near-term earnings, the 34% year-to-date decline in the share price could represent a good opportunity to invest in a fascinating business.

Disney+ launched in the US last November and has already secured nearly 30m subscribers, ahead of analysts’ initial expectations.

While Disney was behind the curve in launching a streaming service, the quality of its existing content and franchises could put it in a strong position to unseat more established rivals like Netflix.

Also key to the investment case is Disney’s unrivalled intellectual property which generates significant opportunities for revenue generation, such as merchandise linked to films and show.

NEW BOSS

The company is at an interesting inflexion point with chief executive Bob Iger moving to the executive chairman’s seat after more than a decade in charge and 27-year Disney veteran and former parks and products boss Bob Chapek stepping up to the helm.

Two of its major film franchises are also at a crossroads following the end of the current cycle of Star Wars and Marvel films, with Disney+ likely to see greater exploitation of these universes on the small screen.

Notwithstanding the current disruption caused by the coronavirus outbreak, the theme parks division is a big driver of profit and cash flow for the company and also deepens the resonance of its intellectual property with consumers.

As media commentator Matthew Ball described it in a recent essay: ‘There is nothing that can compare to the impact of a child being hugged by her heroes. The ability to enjoy your favourite intellectual property as “you” is unique and lasts a lifetime.’

This is important as the company transitions from wholesale approach, where its content was delivered to consumers through other platforms, to a more direct relationship with viewers.

UNRIVALLED POSITION

For many of us, watching our first Disney film was a coming of age experience. With the company’s capture of the Star Wars and Marvel franchises over the last decade, plus the 2019 takeover of 21st Century Fox, it has carved out an unrivalled position in the global media sector.

One offshoot of the M&A drive worth noting is that net debt has more than doubled from the $20.9bn posted in the September 2018 financial year to $47bn at the last count.

VARIETY OF EARNINGS

Headquartered in Burbank, California, Disney’s activities span films, television, publishing, merchandise and theme parks and it generated revenue of nearly $70bn in the 12 months to 28 September 2019.

It is split into four different divisions: media networks; the parks, experience and products arm; studio entertainment; and direct to consumer / international.

While the potential of the parks side of the business may be significant, the short term looks set to be a rollercoaster ride thanks to the challenges posed by the coronavirus pandemic.

Alongside first quarter results (4 Feb) Disney flagged a $280m second quarter hit to operating income from the closure of its parks in Shanghai and Hong Kong. Tokyo Disney Resort has also closed to the public. Since then it has temporarily closed its parks in California, Florida and Paris. The flying ban between the UK/Europe and the US will have a definite negative impact on earnings, particularly if the ban extends to the Easter holiday period.

RIVALS AT THE BACK OF THE QUEUE ON THEME PARKS

Taking a long-term view and hoping that coronavirus will be a short-term disruption, Disney’s parks dominate a market with significant barriers to entry.

As well as having strong franchises which can be used in the creation of rides, rivals attempting to replicate its success face issues around securing large enough sites as well as the huge upfront costs of building and maintaining these parks.

In the three month period to 28 December the parks, experiences and products division accounted for 35% of revenue but 58.4% of operating income.

GROWTH DRIVERS

On future plans for the division UBS analyst John Hodulik notes: ‘Chapek suggested the segment still has a ways to go in terms of pricing power and described how yield management continues to drive value without hurting the customer experience.

‘His longer-term goal is to extend the Disney franchise in the parts of the world where it doesn’t have a presence.’

The other key growth priority is streaming. Disney+, which is being offered in a bundle alongside Disney-owned sports platform ESPN+ and Hulu (acquired as part of the Fox deal) in the US, has a target of hitting 60m to 90m global subscribers by the end of the company’s September 2024 financial year.

For context this compares with 167m subscribers worldwide for Netflix and could end up being quite a conservative target.

EARNINGS SETBACK

Because Disney+ is being launched in a competitive market where incumbents like Amazon’s Prime Video and Netflix have built strong positions, and others such as Apple TV+ and HBO have also launched of late, Disney is investing heavily in original content alongside its existing back catalogue.

As a result Disney+ is not expected to turn a profit until its September 2024 financial year. ESPN is also affected by inflation in the price of rights to live sport and this could pile further pressure on margins.

There are also market fears that coronavirus disruption to the sporting calendar could see ESPN temporarily short of new content which could trigger subscription cancellations.

Disney has an impressive roster of films set to be released in the future including a live action version of Mulan and the next title in the Marvel series, Black Widow. However, cinema attendance could be affected by coronavirus and the film industry is already pushing back big-name releases until later in the year or 2021.

POINTS TO CONSIDER

The main risks to our positive view on the stock is that the coronavirus outbreak has a more lasting impact on appetite for travel, thereby depressing visitor numbers at its parks in the longer term.

You must also consider the risk that Disney struggles to secure expected subscriber numbers for Disney+ (as well as Hulu and ESPN) and faces escalating programming costs.

On balance though we think these risks are outweighed by the ability to invest in such a high quality business at significantly lower share price than you could at the start of 2020. If you’re happy with the risks and understand the shares could be weak near-term, buy at $91.81. Otherwise, wait on the sidelines and reappraise Disney’s status once the coronavirus pandemic is over.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.