Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

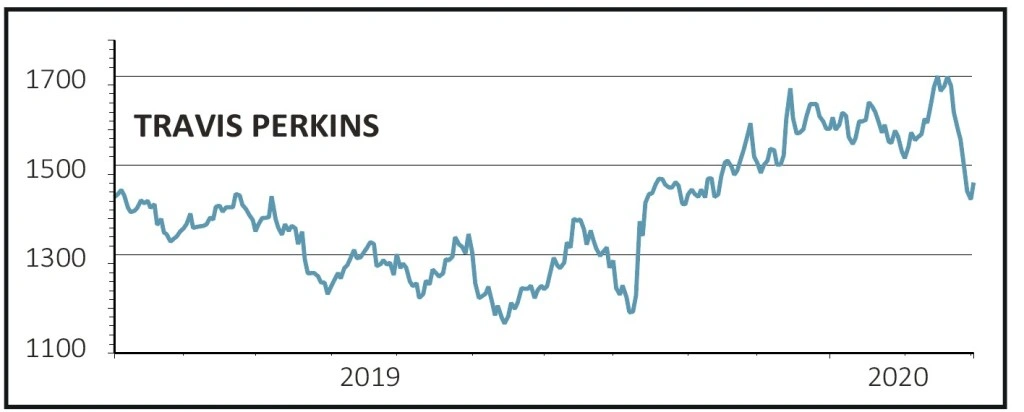

magazineTravis Perkins continues to build confidence with investors

Travis Perkins (TPK) £14.95

Loss to date: 6.3%

Original entry point: Buy at £15.96, 16 January 2020

Considering that we recommended Travis Perkins (TPK) just days before the coronavirus outbreak hit the headlines in January, we aren’t deterred by the small loss in the shares to date.

As the latest results showed, the core merchanting business is outperforming the market with 3.3% like-for-like sales growth last year, split evenly between price and volume increases.

The Toolstation business delivered an outstanding performance last year, with like-for-like revenue growth of 16.3% and overall sales growth of more than 25% due to new store openings, consolidating its market-leading position.

The TradePro and Kitchen & Bathroom units also performed well with an increased share of revenues from higher-margin installation services.

Even the Wickes retail business, which is being demerged from the group next quarter, turned in close to 10% revenue growth thanks to new ranges in decorating and landscaping.

With the housing market still chronically short of supply, and demand rekindled following the election, the repair, maintenance and installation market should see a tangible improvement this year.

SHARES SAYS: As the leading player in its respective markets, and with a clearer focus on trade customers post the Wickes demerger, we believe Travis is set for further growth and a re-rating of the shares.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.