Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineMarket sell-off: assessing the damage and looking for bargains

WHAT’S IN THIS ARTICLE?

We’ll run through the reasons why stocks have fallen, compare this sell-off to previous market corrections and consider why certain companies have been affected more than others.

We will also look at the stocks that have risen in value during the market turmoil and finally we choose three shares to consider buying as long as you understand that their prices could easily fall in the near-term. We’re focused on the longer-term value potential.

The speed at which stocks fell in late February took many people by surprise, yet there is no reason to lose faith in investing. It is important to remain optimistic and focus on the long-term potential for your money to grow by owning shares.

Arguably investors were too complacent about how far the coronavirus could spread and its potential to damage economies far beyond China, hence the significant scale of the market correction which started on 24 February. Fear gripped the markets and investors panicked.

This has been an uncomfortable experience yet it is important to understand that share prices should move up and down. Going up in a straight line is not normal. Time and time again the stock market will go through a wobbly patch and you’ll get days of big share price movements. By staying invested you are ready to play the market recoveries which often happen faster than you might think.

TIME TO BUY?

Last week’s punishing market correction will have put a dent in people’s portfolios. No-one knows when exactly the markets will recover, however it is clear that the latest sell-off is pricing in a very significant reduction in earnings for companies in many different industries.

Many investors are asking if now is the time to pile in and take advantage of weak share prices. In effect the stock market has just presented a bargain sale and there are plenty of stocks with 10% or more slashed from their price.

However, there is a very real chance that markets have further to fall as we don’t know the full impact on corporate earnings. Therefore we suggest you take a very cautious approach and be very selective when looking for opportunities in the present climate. Think very carefully about any risks to each stock or fund and perhaps drip feed money rather than putting everything in at once.

‘The outbreak is far from contained and continues to spread internationally, meaning the corresponding double whammy supply and demand shock that hits economic activity is significantly larger than most analysts have forecast and continues to mount,’ says Eleanor Creagh, market strategist at Saxo Bank.

Buying more shares for your money

If you have a regular investment set up then keep putting money into the markets.

You’ll buy at a lower price compared to recent history and possibly even lower the month after if markets are still falling.

This is called pound cost averaging – you buy more shares for your money when markets are low and less when markets are high. You are not trying to time the market and you’re maintaining a healthy investing habit.

‘If the virus continues to spread the market would have to discount these disruptions as a longer term reality and the subsequent uncertainties surrounding the hit to activity and longer term impacts like accelerated de-globalisation would see another wave of selling.’

THREE REASONS WHY STOCKS HAVE FALLEN

The decline in share prices fall into one of three categories:

– Companies said earnings will be hit

– The market thinks earnings will be hit but there has been no confirmation from the company

– Shares de-rated even though there is no reason to fear a cut to earnings

Investor panic has dragged down nearly all stocks, some for good reason and others simply caught up in the market chaos.

Engineering firms with bases in China seem to have been particularly sensitive to the outbreak, with factory shutdowns and supply chain issues smarting for the likes of Porvair (PRV), Avingtrans (AVG:AIM) and Ricardo (RCDO), which is also struggling against a weakening auto market trend.

But shares prices have sold off heavily for companies like IMI (IMI) and Luceco (LUCE) even in the face of reassuring commentary or saying nothing at all.

With markets trading on fear, investors are taking a ‘sell first, ask later’ position. For example, miner Rio Tinto (RIO) may have admitted that projects across the entire industry ‘could’ be affected but it stopped short of any sort of confirmation. Its shares have lost 9% since 21 February as the market automatically assumes Chinese commodities demand will drop off a cliff.

But underlying the nervousness there is real economic damage being done such as Diageo (DGE) which won’t get back lost alcohol sales as a large number of Chinese people remain stuck at home.

HOW DOES THIS SELL-OFF COMPARE TO OTHERS IN THE PAST?

The current sell-off is severe but worth keeping in perspective for now. Since markets closed on Friday 21 February and the intervening spike in coronavirus cases outside China which sparked real market panic, the FTSE 100 is down 8.5% as of 3 March.

The biggie in terms of market corrections is the one that accompanied the global financial crisis. Between October 2007 and March 2009, when equities bottomed out, the FTSE fell more than 45% and the US S&P 500 more than halved.

More recently in October 2018 a cocktail of overstretched valuations, US-China trade tensions and rising bond yields saw the FTSE 100 fall more than 10% by the end of that year.

The table showing the biggest one-day falls for the index also provides some context for the current daily fluctuations in the market.

WHAT’S THE POTENTIAL ECONOMIC IMPACT GLOBALLY?

At present it is hard to know exactly the extent of the economic damage which the coronavirus will wreak but there will certainly be damage and it could be material.

Bank of America forecasts the world economy will grow at its weakest pace since the financial crisis at 2.8% in 2020.

The closer economic ties between China and the rest of the world, and its status as the world’s second largest economy, mean comparisons with the SARS outbreak of the early noughties are no longer relevant. If the coronavirus spreads extensively in Europe and North America, fears of a global recession will increase.

WHICH SECTORS HAVE BEEN HIT HARD?

The airline sector has been hit hard as the market worries about a big drop-off in air travel.

It now looks like many airline operators including Jet2 owner Dart (DTG:AIM) and TUI (TUI) might have added capacity at what could be the wrong time.

Both companies expanded seat capacity to fit a hole created by the collapse of Thomas Cook last year, adding 10% and 13% on short-haul European routes respectively.

In Dart’s case its share price subsequently jumped over 100% as the market priced in the potential for a big boost in earnings.

Airline bookings are expected to fall markedly, with British Airways owner International Consolidated Airlines (IAG) and EasyJet (EZJ) warning on 28 February about ‘softening demand’.

WHAT CAN WE LEARN FROM OTHER SECTORS?

The energy sector has suffered with the 10 stocks in the FTSE 350 losing an average of 18% since the start of the year and 7% last week, compared with respective losses of 6.5% and 5% for the benchmark.

The main reason is concerns over economic growth in China which is one of the world’s biggest users of oil as well as commodities like iron ore and copper.

Within the energy sector, the largest firms with the best balance sheets, namely BP (BP.) and Royal Dutch Shell (RDSB), have outperformed their smaller peers as their cash flows and by extension their dividends are more resilient to a lower oil price and lower revenues.

WHAT ARE THE UNDERAPPRECIATED RISKS?

A slowdown in Chinese output, and the continuing spread of the disease outside of China, is likely to have a significant negative effect on global economic growth this year.

Dozens of large multi-national firms have already warned that their earnings will be impacted by the coronavirus.

The risks for investors lie in the small and mid-cap companies which have yet to quantify the potential damage to their earnings and balance sheets.

A further risk for investors is that companies which are seen as ‘at risk’ from the virus see their financing squeezed as creditors and suppliers demand their money or stop providing their goods or services.

HOW HAS THE HEALTHCARE SECTOR FARED?

The FTSE 350 healthcare stocks have not shown the same level of weakness as the market, which makes sense given the industry is on the front line in the battle against the coronavirus.

GlaxoSmithKline (GSK), one of the largest vaccine makers in the world, announced on 4 February a research tie-up with China’s Clover Biopharmaceuticals to co-develop the Chinese company’s protein-based coronavirus vaccine candidate Covid-19 s-Trimer.

It is also working to accelerate the creation of a vaccine in collaboration with the Coalition for Epidemic Preparedness Innovation (CEPI). Glaxo’s shares have outperformed the market by around 8% since 21 February market close.

Firms like medical devices company Smith & Nephew (SN.) and animal genetics firm Genus (GNS) have only seen a small share price decline. Both produced consensus-beating numbers and positive outlooks, and investors will have naturally been drawn to the industry as a supposed defensive sector.

THREE STOCKS: WHY THEY’VE FALLEN

CARNIVAL

The world’s biggest cruise operator Carnival (CCL) has faced choppy waters in 2020 with the shares down 35% to £24 year-to-date. Investors took fright when its Diamond Princess ship carrying 3,700 passengers was effectively quarantined off Japan’s Yokohama for two weeks.

On 12 February the company said the potential suspension of its Asian operations through to the end of April would impact 2020 earnings by $0.55 to $0.65 per share, shaving around 14% off expected full-year earnings.

Analysts at Morningstar cautioned investors not to turn their back on the sector. They said: ‘We remind investors not to hit the panic button, as in the year following SARS, H1N1 and Zika, Carnival and Royal Caribbean both posted positive yield growth, conveying resilience of demand across the industry.’

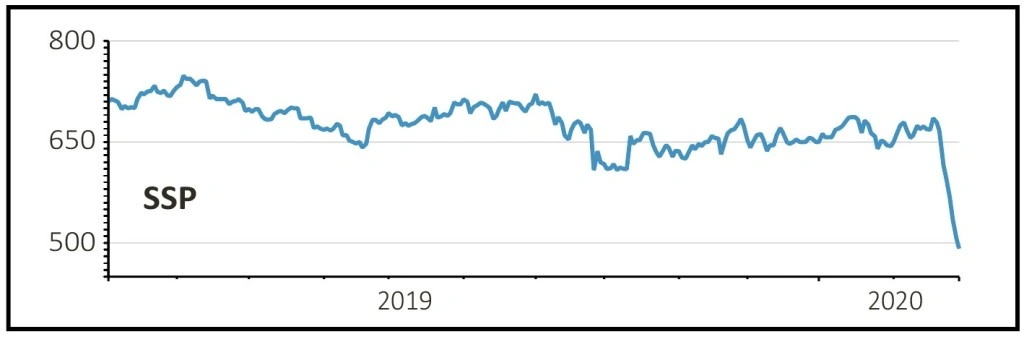

SSP

Food seller SSP (SSPG), which operates units in transport hubs, recently warned the virus will reduce revenue by £10m to £12m and operating profit by £4m to £5m.

Given its reliance on airports and train stations for business, SSP’s earnings look almost certain to be impacted further if the virus continues to spread, but its long-term fundamentals remain unchanged. The company serves a captive audience and its margins have been growing steadily.

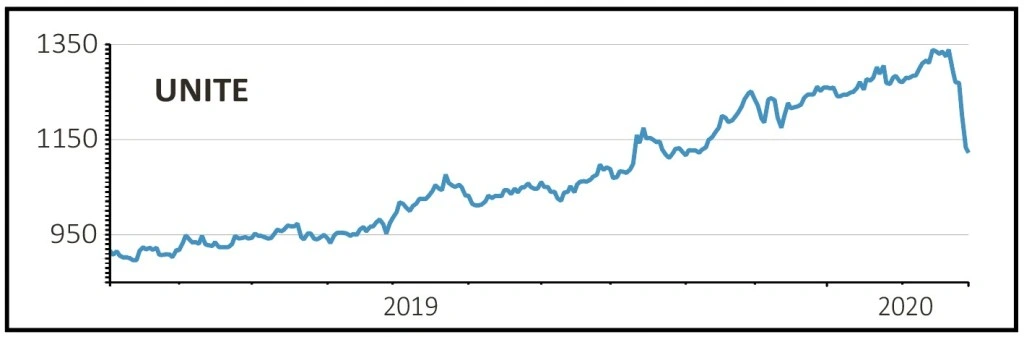

UNITE

Shares in student accommodation investor Unite (UTG) have fallen as the market is worried about the travel restrictions in a number of countries, thereby potentially making it hard for overseas undergraduates to get to the UK.

China is the biggest source of international students in the UK, with more than 100,000 according to the latest figures from the Higher Education Statistics Agency.

The sector was already facing a challenge associated with a Brexit-inspired drop in the number of EU students.

Alongside full year results (26 Feb) the company said it was confident that any potential downside would be outweighed by domestic growth built on demographic trends and overseas students attracted by supportive Government policies.

THE STOCKS THAT HAVE HELD UP WHEN EVERYTHING ELSE IS DOWN

PLUS 500

Shares in online trading platform Plus 500 (PLUS) gained 7% during the global markets sell-off last week as investors thought it would benefit from wild swings in share prices, creating an environment favoured by people trading the markets. The more trades, the more commission and financing fees earned by Plus 500.

The company mentioned it was seeing better trading activity at its half-year results on 12 February and on 28 February confirmed a significant increase in customer trading activity.

Also helping to support the shares has been the company’s additional $30m buyback programme, following the completion of the $50m buyback programme announced on 13 August 2019.

BUNZL

Business supplies distributor Bunzl (BNZL) has been a rare bright spot in the sell-off, outperforming the market thanks to forecast-beating earnings and an upbeat outlook for this year.

Bunzl has been making acquisitions in growth markets like Brazil to offset slowing organic growth among its retail and grocery customers in the US.

Among the products it supplies are hygiene and medical items including masks and gloves which have been in high demand since the virus outbreak.

HUNTING

Oil services firm Hunting (HTG), which makes a range of tools and solutions used by the oil and gas industry, had previously endured share price weakness as investors factored in slowing demand in the US shale market which has accounted for much of its recent growth.

In this context the latest results (27 Feb) were seen as reasonable with solid cash flow performance and earnings, modestly ahead of expectations.

What really got investors excited was a share buyback as Hunting said the current price ‘highly undervalued’ the group and it pledged to buy 2m shares at a cost of £6.2m.

THREE STOCKS TO BUY NOW

KAINOS 786p

If you believe the pre-Budget rhetoric, the ‘end of austerity’ will open the floodgates on public investment and IT projects. That’s great for Kainos (KNOS) which is one of the Government’s key private sector digital transformation partners.

It has designed and implemented projects for the Cabinet and Home Office, NHS and many more, but it is also Europe’s Workday software testing and implementation partner, which gives additional growth scope in the UK and overseas.

A tight market for technology talent remains a challenge, although it has good links into universities (including 11% shareholder Queen’s in Belfast) and business schools.

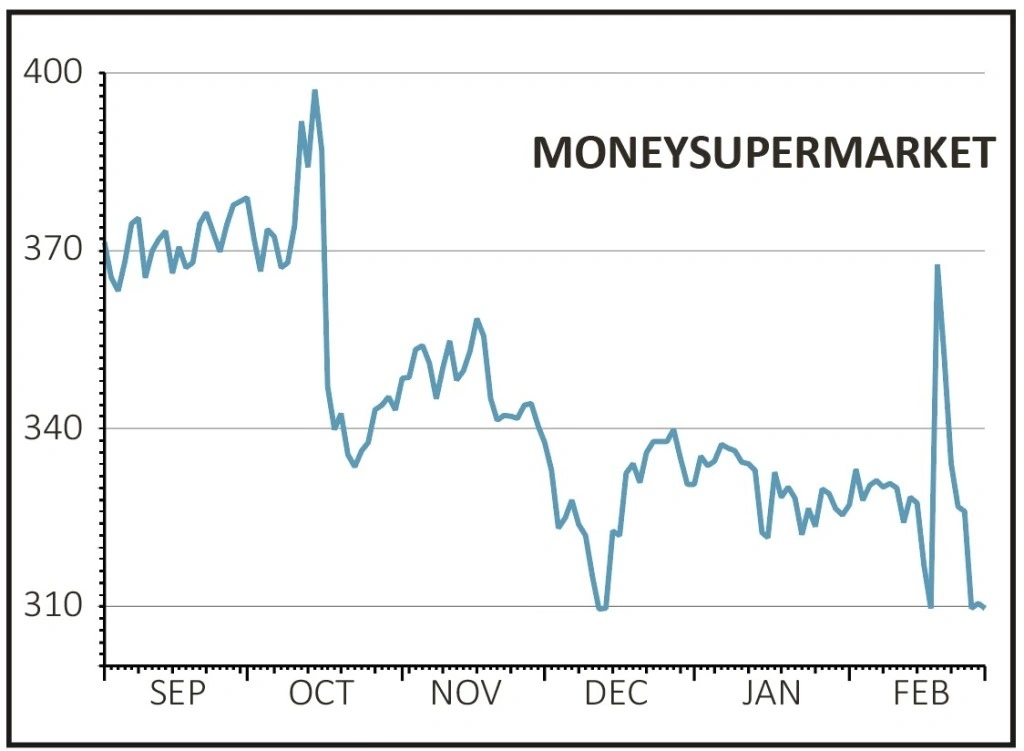

MONEYSUPERMARKET 312.8p

The indiscriminate sell-off across the UK market has seen comparison site Moneysupermarket (MONY) give back all the gains it made (and more) in the wake of an encouraging full year trading update which last month triggered a huge spike in the shares.

The market sell-off has effectively rewound the share price so you can buy at roughly the same level at which investors suddenly got very excited, even though nothing has changed to the business.

It is signing up increasing numbers to bill management and credit monitoring services, boosting engagement and the value it can generate from these users.

The company arguably has no direct exposure to the coronavirus and it seems people will still be shopping around for financial products, energy providers and insurance even in the event of wider disruption. However, a global recession could alter this view as widespread job cuts could make it harder for people to qualify for certain loans and credit cards.

VISTRY £13.10

The housebuilders, along with all consumer-facing stocks, have been battered as the coronavirus-driven selling has ramped up. Yet Vistry (VTY) (formerly Bovis Homes) looks interesting at a beaten down price.

Post Vistry’s acquisition of the regeneration and housebuilding divisions of Galliford Try (GFRD), Numis is forecasting 35% pre-tax profit growth between 2019 and 2021 as the company increasingly develops higher margin mixed use sites.

A lasting hit to consumer sentiment and the economy is a risk to weigh given the likely knock-on impact on the property market. But a forward price-to-earnings ratio of 9.7 and yield of 5.5% are attractive.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.