Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineAre stocks heading for a bear market?

The period of 24 to 28 February saw the FTSE 100 suffer its steepest weekly fall since October 2008, just after Lehman Brothers went down, the global financial system was on its knees and a global bear market was in full swing.

The trigger for such a plunge has been the longer-than-expected duration and greater-than-expected geographic reach of the coronavirus.

TWO POSSIBLE VIEWPOINTS TO CONSIDER

The first view is that markets are losing their marbles and behaving irrationally, giving way to indiscriminate selling in a panicked manner.

This assessment rests upon the limited number of people who have caught the virus and the smaller number still who have died. While the numbers are still distressing to consider, especially if you know anyone involved, World Health Organisation data suggests that influenza and other respiratory illnesses lead to between 290,000 and 650,000 deaths worldwide in any given year.

We are nowhere near those levels yet, or even the 13,000 killed by a particular severe year for flu in the UK in 2013.

The second view is that markets are behaving logically, not least because they had behaved irrationally beforehand.

It has been possible, looking at issues such as global merger and acquisition activity, the lack of volatility and especially equity valuations in the US, to argue that markets had become frothy and complacent.

The rampant run witnessed in January alone in names such as Tesla, Beyond Meat and Virgin Galactic was enough to frighten anyone but it is possible to argue that markets have been buying narratives and ignoring the disciplines of numbers for some time.

How else can you explain how Apple’s market cap grew by $550bn (or 74%) in 2019, a year when its sales fell by $566m (0.3%) and its net profit fell by $1.9bn (or 3%)?

Looking at the sharp falls through this latter lens, markets are taking a more realistic view of the prospects for corporate profits and cash flows, at least in the near term.

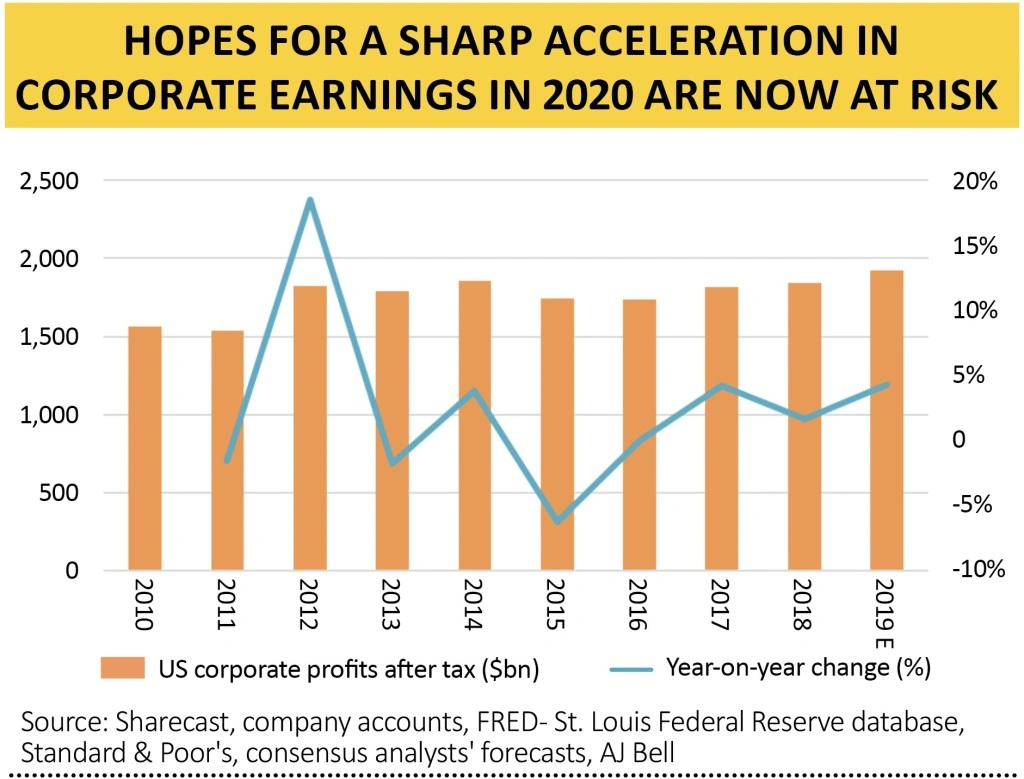

And this is a legitimate problem. The S&P 500 index in the US rose by nearly 30% in 2019, even though corporate profits barely rose at all.

This means that pretty much all of last year’s gains were based on multiple expansion – the ‘p’ in the price-to-earnings ratio went up – rather than increases in earnings (the ‘e’ in the same calculation).

Valuations cannot be stretched higher for ever, even if no-one knows what will cause them to snap back.

On this occasion, the possible impact upon supply chains, freight costs and end demand (not just in China but worldwide) across many countries and industries has forced at least a temporary reappraisal as the future earnings growth upon which share prices were relying now looks less likely to materialise in 2020.

DOWNS AND UPS

The pull-back looks quite rational from this perspective. The more companies that withdraw earnings guidance or actively warn on profits, the choppier stock markets could get.

We have not had a recession in the US for over a decade and this market is pretty confident in saying that one is not priced in yet.

That does not mean a recession is certain, although that must be a possibility with China, the world’s second biggest economy, unless the viral outbreak is contained and eradicated remarkably quickly.

NOW VERSUS HISTORY

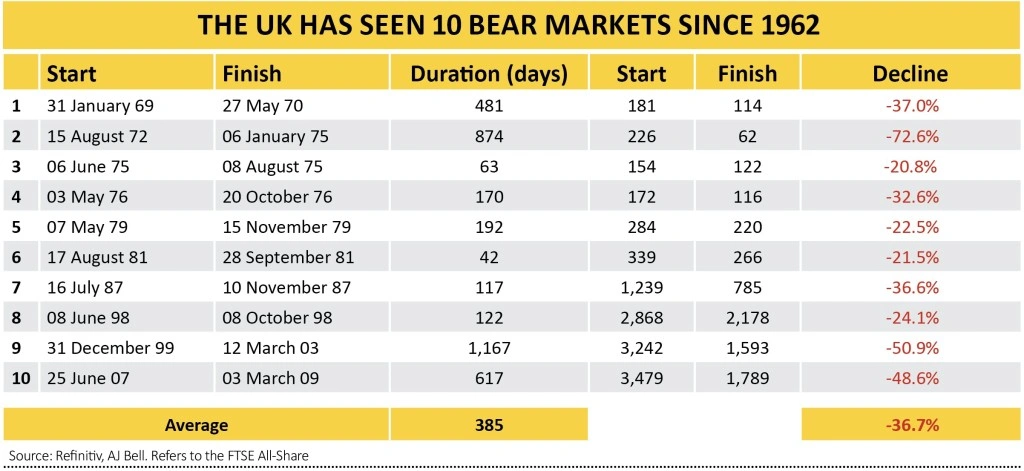

So how bad was the February fall in the grand scheme of things? Since the inception of the FTSE All-Share in 1962, there have been 10 bear markets. Their average duration has been just over a year and the average drop has been 36%.

By contrast, nine bull markets (excluding the current one) offered an average capital gain of 143% over an average of 1,200 days.

At the close on Friday 28 February, the FTSE All-Share was down by 14% from its January peak and 15% from its May 2018 all-time high.

TRIO OF TACTICS

This can be viewed positively as markets are still holding up well despite the uncertainty, or negatively as markets are still too relaxed about the impact of the virus.

Investors will have to make their choice to as which scenario they believe but whatever their viewpoint there are three long-term tactics which can help to manage the downside when times do get tough.

Keep a diversified portfolio across asset classes, industries and countries, to ensure your returns are not too reliant on one or two areas.

Ensure your portfolio offers some downside protection and contains some ballast as well as picks for capital gains and income. An allocation to cash can help and it also leaves scope to step in and pick up bargains in the event of a real panic.

No-one knows what’s going to happen so don’t guess and don’t overtrade. It would be expensive to switch a big percentage of a portfolio around and if the outbreak is contained quickly you could miss a rally – and a better exit point – or even a fully-fledged market turnaround.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.