Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWill the ‘Boris bounce’ fall flat?

March could be a big month for the UK stock market. Investors continue to await news on the spread of the coronavirus (COVID-19) and whether containment and quarantine policies are starting to work. The Bank of England will formulate its first monetary policy decision under its new governor, Andrew Bailey on the 26th of the month; and the new chancellor of the exchequer, Rishi Sunak, will outline the fiscal policy plans of the Boris Johnson-led Conservative Government on the 11th.

How the viral outbreak develops is still anyone’s guess. The profit warning from Apple suggests the outbreak is starting to have a negative impact on economic activity, although markets still seem to be leaning toward the view that any effects will be relatively short-lived, as was the case in SARS in 2002-03, and that the world is not on the brink of the sort of apocalypse witnessed in John Wyndham novels.

The Bank of England still seems more inclined to cut interest rates rather than raise them, although the arrival of a new governor could change the tone, as could both fresh economic data and Government policy.

On the policy front, economists seem convinced that Sunak will oversee an increase in spending as the Government prepares for the ending of the Brexit transition phase on 31 December and looks to cement its current popularity in the seats won in last year’s election.

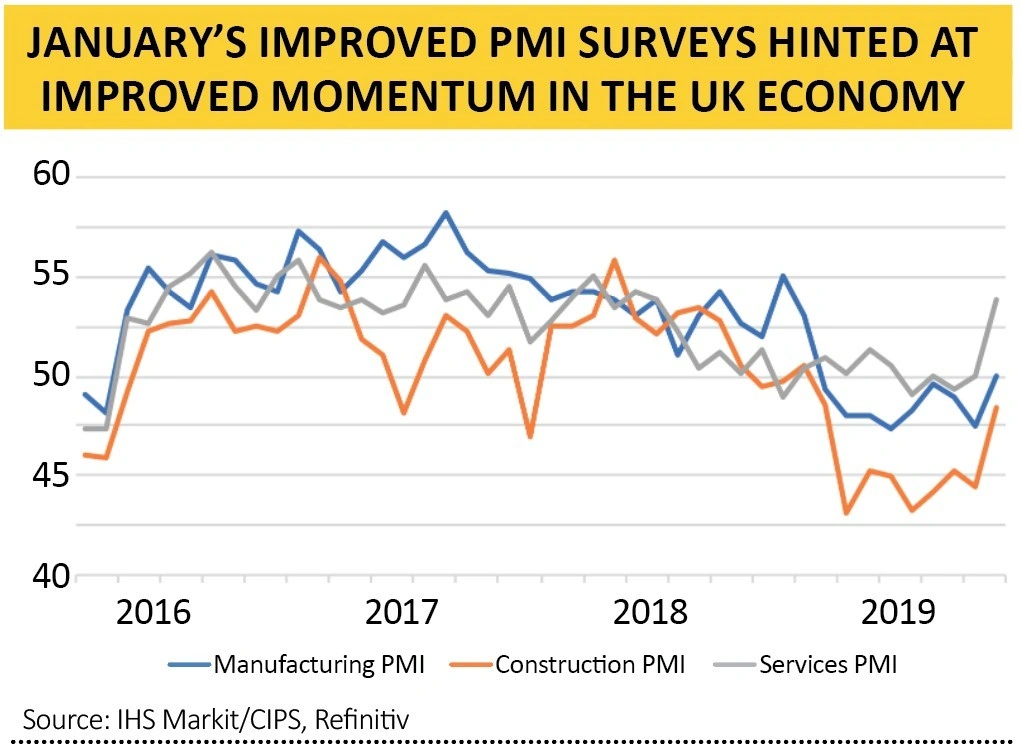

In terms of the economic data, there have been some tentative signs of improvement and it will be interesting to see if the latest batch of purchasing managers’ indices for the manufacturing, construction and services industries that will come out between 2 and 4 March show additional momentum or not.

MOVING PARTS

There are four main moving parts to any country’s GDP data, at least from a pure accounting perspective. They are:

– Private consumption

– Business investment

– Government spending

– Trade (defined as exports minus imports)

While investors may not be accustomed to receiving too much good news on the UK economy, this is perhaps one reason why upside surprises cannot be ruled out.

It is quite possible that consumer spending, business investment and Government expenditure all rise, if left to their own devices.

The last forecast provided by the Office for Budget Responsibility (March 2019) looked for a meagre 1.1% increase in household consumption in 2019, down from 1.7% in 2018 and 2.1% in 2017. However, the OBR then expected an acceleration to 1.5% in 2020 and 1.6% in 2021. This seems sensible enough, especially if the Conservatives follow through with some of their promised tax cuts.

Moreover, wage growth continues to outpace inflation and that trend could also boost individuals’ spending power, if it is maintained. One risk here is that the household savings rate starts to rise. At 5.5% in Q3 2019 this came in well below the near-9% average seen since records began in 1963.

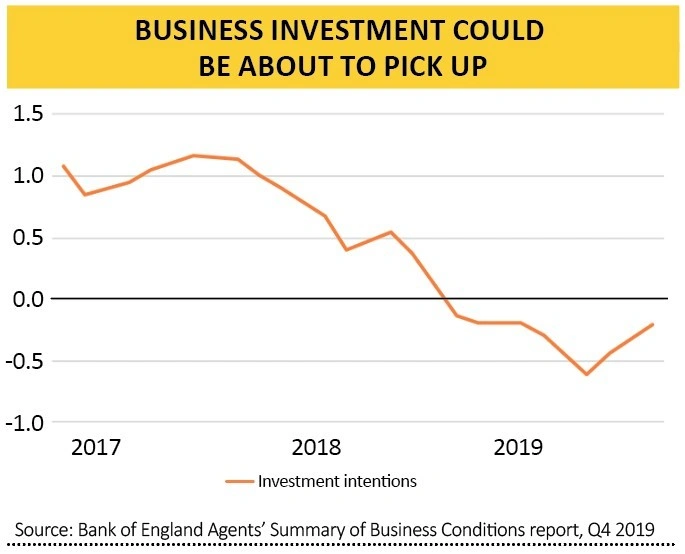

The OBR expected business investment to fall for the second time in a row in 2019 but its numbers then looked for a sizeable post-Brexit deadline bounce, with 2.3% growth in 2020 and 2021.

The last Bank of England agents’ survey, for Q4 2019, gave some credence to that view as the investment intentions reading improved for the second quarter in a row, albeit from very low levels.

Growth in Government spending looks set to accelerate, at least if the ejection of the apparently fiscally-prudent Sajid Javid from 11 Downing Street and the decision to press ahead with the HS2 rail project are any guide.

Another former chancellor, Philip Hammond, had begun to refer to £26bn of fiscal headroom, which is not a pot of cash, but extra spending that would take the UK’s annual budget deficit back to 2% over the next five years. The only question to ask is presumably whether the new Government stops there or spends further. The OBR factored in a relatively modest increase in spending in 2020.

The hardest area to judge may be trade, given the impact of Brexit talks, the coronavirus outbreak and wider global trade tensions. Export growth has sagged of late while import growth has surged, increasing the trade deficit and weighing on growth.

However, the OBR did expect the negative impact to shrink in 2020 and beyond so it will be interesting to see how the OBR’s forecasts change from a year ago when the next Budget is released on 11 March.

UPS AND DOWNS

If this column was forced to guess, Government spending could provide the greatest upside surprise, and trade is perhaps the biggest risk, with the overall scope for surprises slanted to the upside. If so, that could favour domestic-facing stocks over the multinationals of the FTSE 100, although, as Warren Buffett once commented: ‘Forecasts tell you a great deal about the forecaster; they tell you nothing about the future.’

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.