Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

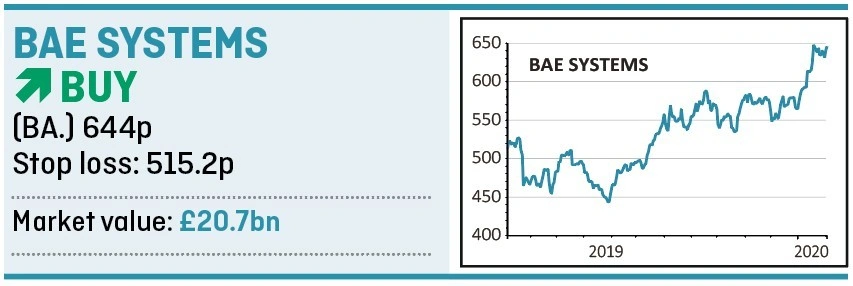

magazineWhy you should buy BAE after acquisition drive

Defence giant BAE System’s (BA.) cheap valuation doesn’t give the company sufficient credit for the improving quality of its business – a transformation which will be accelerated by two recent acquisitions in the US.

Take the opportunity to buy now and gain access to a steady stream of income at a decent yield which should complement a re-rating story.

In late January the company announced two significant deals in the US. They encompassed the $1.9bn purchase of a military GPS system – the Military Global Position System – from Collins Aerospace, and the $275m purchase of Raytheon’s Airborne Tactical Radios division.

There are still some hoops to go through, but assuming the transactions complete these businesses would be absorbed into the company’s Electronic Systems division.

The significance of this M&A activity is two-fold. It will take US operations to around half of overall sales. The US defence market is the largest in the world and as such affords BAE lots of growth potential.

The nature of the outfits, not just their location, is important too. Areas like weapon systems and secure communications are being prioritised as global governments look to face up to complex 21st century security threats.

Investment bank Berenberg believes the addition of the

two new businesses will boost free cash flow by around 5% and 6% in 2021 and 2022 respectively, helping the company exceed its three-year cumulative target of generating cash of more than £3bn.

Improving cash generation, allied with a strong order book, mean the company warrants a higher valuation than the current 2020 price-to-earnings ratio of 13 falling to 11.8 in 2021 based on Berenberg forecasts. The company has a 3.8% prospective dividend yield.

The fly in the ointment of BAE’s investment case is the uncertainty over a £10bn order for 48 Typhoon jets from Saudi Arabia and this may come up at the company’s full year results on 20 February.

Overall we think in an uncertain world BAE is a good place to put your money. As Deloitte summarised in its 2020 outlook on the aerospace and defence sector: ‘Demand for military equipment is on the rise as governments across the globe focus on military modernisation, given increasing global security concerns.

‘The uncertainty and sustained complexity of the international security environment worldwide is likely to boost global defence spending over the next five years.’

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Education

Exchange-Traded Funds

Feature

Great Ideas

Great Ideas Update

Money Matters

News

- China trusts under pressure from coronavirus fears

- Sales growth challenges weigh on Diageo and Unilever shares

- The key challenges facing new BP boss

- Surging stock prices mask concerns about a US economic slowdown

- The companies in the race to find a coronavirus cure

- Burford Capital shares gain despite earnings warnings