Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineOur six best small cap ideas

Small caps could be a great place to invest in 2020 as there are some attractively-priced gems flying under the radar of many investors.

It is important to stress that small caps aren’t for everyone as they can be much higher risk investments compared to larger companies. However, for those comfortable with the risks, history shows us that smaller companies can outperform their larger counterparts.

So why look at the space now? There are four key reasons why small caps are really interesting at the moment and why you could potentially pick up a bargain.

1 – Small caps have lagged as the broader UK market has been out of favour. Many investors have turned their back on domestic-facing stocks since 2016 over Brexit fears. Sentiment now seems to be turning which provides an opportunity as many smaller companies are trading on very attractive ratings.

2 - The rise of passive investing (tracker funds and exchange-traded funds) has left small caps unloved. Investors have put lots of money into passive funds which track various indices. Most of the indices either focus on mid to large cap stocks or specific sectors which means passive ‘money’ is not flowing into the small cap space on a large scale.

3 - Liquidity fears mean institutional investors are no longer taking big stakes in small companies. The Woodford Equity Income fund scandal has put the spotlight on how quickly a fund manager is able to sell holdings from a portfolio should investors want to cash out.

The Woodford fund struggled to sell a lot of holdings quickly and is still trying today to exit some more obscure holdings. This has resulted in fund managers losing their appetite for many smaller companies for fear they won’t be able to get rid of holdings when they need to.

4 – Legislative changes have reduced the volume of analyst coverage on small caps. Something called ‘Mifid 2’ has resulted in fewer analyst numbers; of those still in the job, the coverage has tended to focus on mid and large cap stocks.

Less is being written about smaller companies, so it is harder for investors to find out about the opportunities in this section of the stock market.

While small caps are commissioning reports themselves, these tend not to include buy or sell recommendations.

The end result is a growing number of small caps which are going unnoticed by the broader investor universe – and some of these are simply trading on too cheap a price.

Read on to discover six of our favourite smaller companies and the reasons why they could make you good money.

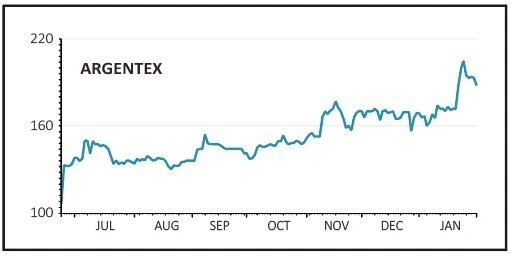

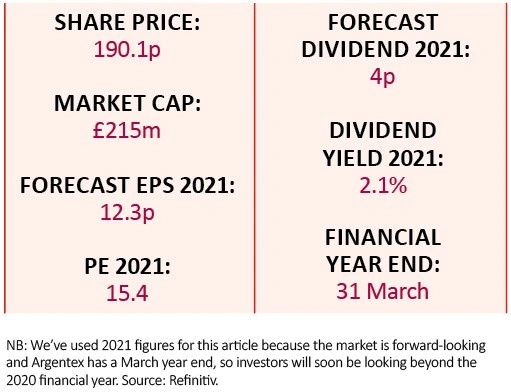

ARGENTEX (AGFX:AIM)

UK-based foreign exchange (FX) provider Argentex (AGFX:AIM) is early in its already impressive growth trajectory, yet unlike some growth companies it is highly profitable and supported by founder-led managers that have over 50 years of collective industry experience.

The company is targeting 30% to 35% growth every year over the next five years accompanied by operating margins in the mid to high 30% range. If the targets are achieved the business will be valued much higher than it is today.

Bear in mind that Argentex has been listed for less than 12 months and has released relatively few updates to the market, so some investors may want to see a greater track record of life as a listed entity before buying its shares. It has also been in business for only eight years.

The firm was founded in 2011 by the current management team, Harry Adams and Carl Jani backed by John Beckwith’s Pacific Investments. Digby Jones is executive chairman.

Beckwith has founded a number of successful fund management businesses including household names such as Liontrust Asset Manangement (LIO) and hedge fund Thames River Capital.

Argentex floated on the UK stock market in June last year and operates as a principal broker for non-speculative FX transactions to institutions and high net-worth individuals. The dealers have a minimum of 10 years’ FX experience and provide personal client-led advice and execution to customers with genuine business needs.

Impressively, since commencing trading in 2012 the business has experienced significant year-on-year growth in customers, transactions volumes and revenue while it has been profitable in every year, achieving around 50% operating margins.

The key to growing the business is increasing client numbers while at the same time improving client conversion rates. The company demonstrated this for the six months to 30 September 2019. Volumes of FX traded increased by 16.4% to £5.96bn which translated into 42% higher revenue to £13.8m and operating profit of £6.5m (2019: £2.6m).

Argentex added 210 new clients and had 932 corporate clients active during the period.

In order to accommodate additional headcount growth, the firm is looking to move into bigger premises. The extra investment and ramp-up of a bigger sales team will result in lower operating margins in the near-term, but hopefully higher growth and productivity further out.

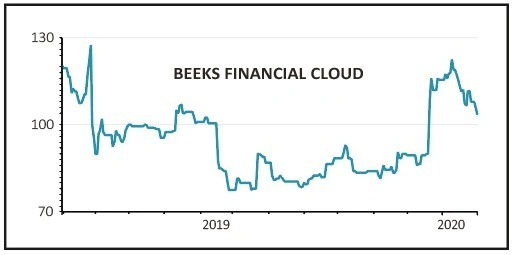

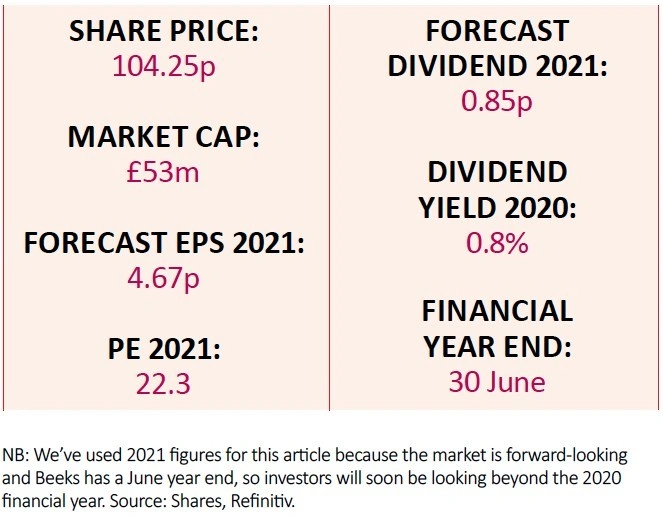

BEEKS FINANCIAL CLOUD (BKS:AIM)

There is a lot to like about Beeks Financial Cloud (BKS:AIM), namely rapid and profitable growth and decent cash conversion from an expanding market niche.

Reported earnings have expanded by 35% on average each year since 2015, and if management can continue their near-faultless execution, the shares could be worth several times the 104.25p at which they now trade.

Started in 2010 by chief executive Gordon McArthur who still owns a 54% stake, the Glasgow-based business provides low latency access for traders to futures, forex and other financial markets. Latency is the time lag you sometimes get when trying to connect to something using the internet.

With 80% of Beeks’ client institutions using automated trading systems, fractions of seconds matter, making the difference between a profitable trade and one that loses money.

Beeks uses a cloud infrastructure platform that runs out of data centres located close to the exchanges, currently 11 in financial centres including London, Frankfurt, New York, Tokyo and Hong Kong. A 12th is in pipeline in Brazil. Clients access the platform through a configurable portal that means they get exactly want they want with Beeks doing the behind-the-scenes work.

Deep-pocketed institutions could do this themselves but it would be costly and a poor use of internal resources, a point demonstrated by the rapid growth in clients, going from 90 in June 2016 to 220 three years later.

Beeks is also increasingly securing large tier 1 clients, winning three in the last financial year, and two more significant contracts just before Christmas.

There are some risks to consider. For example, the bigger the client the longer the sales cycle, and onboarding for some tier 1 clients can run for up to four months thanks to stiffer compliance and procurement processes, versus the couple of days turnaround for small customers. This was illustrated in June 2019 when Beeks had to tone down growth expectations for this very reason. But the upsell opportunity can also be considerable.

The other 20% of revenue comes from serious retail investors, although future growth is firmly institutions-facing.

Other growth opportunities include adding new asset classes such as cryptocurrencies. It is also making progress in fixed income, a potentially huge market.

Return on capital is running at 18.6% and return on equity 20%-plus.

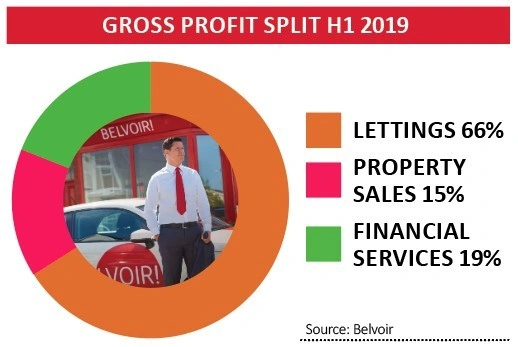

BELVOIR (BLV:AIM)

Shares in franchise-based estate and lettings agent operation Belvoir (BLV:AIM) look great value. The company has a capital-light model which should allow it to grow quickly and its market backdrop is showing signs of improvement.

After a long period where the shares tracked sideways, the market finally appears to be picking up on the company’s appeal. Even after a good run in recent months, the stock trades on a mere 11.4 times 2020 earnings and offers a dividend yield of 4.5%.

A trading update on 30 January revealed 43% sales growth for 2019, ahead of expectations, encompassing a 6% advance for the core property division and 148% in the ancillary financial services arm. Cash flow was strong, pushing net debt down to £6.9m.

This performance was achieved despite the uncertainty created by Brexit and the introduction of a ban on tenant fees hitting the lettings space.

We are excited about the prospects for 2020 given more positive signs from the housing market and the recent transactions involving Dacres and Lovelles which will boost the financial services and property parts of the business respectively.

Lovelles, a 19-office estate agency network, has been acquired for £2m, while Belvoir has agreed a deal to provide financial services to clients of Yorkshire property market specialist Dacres.

Founded more than 20 years ago, Belvoir joined AIM in 2012 and now provides support and guidance to franchisees across 300 high street offices in return for a management service fee. It has a 23 year record of uninterrupted profit growth.

This growth has been supported by M&A both at group level and so-called ‘assisted acquisitions’ whereby it helps local franchisees to identify and make bolt-on additions to their local operations.

The diversified model has significant exposure to lettings, which is generally more stable than estate agency and offers recurring revenue.

This provides some protection against a downturn in the property market. However any deterioration remains a risk for prospective investors to weigh.

The acquisition of Brook Financial Services in 2017 and MAB in 2018 has created a new income stream, adding almost 150 financial advisers who can offer guidance on mortgages and other related financial services.

Brook operates in Yorkshire, while MAB is primarily focused on the Midlands, South West and Wales but Belvoir’s plan is to extend the financial services network across the UK.

The next catalyst for the shares could be the publication of its 2019 results on 30 March.

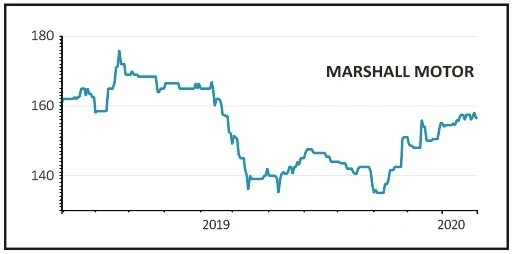

MARSHALL MOTOR (MMH:AIM)

Sometimes it can pay to look at sectors which everyone else currently dislikes, as you might find something really interesting. We certainly believe that is the case with car retailer Marshall Motor (MMH:AIM).

Weaker UK car market conditions could persist in 2020, denting demand for new and used car sales, although the removal of political uncertainty after Brexit could help drive improved consumer confidence and stoke a revival in big ticket purchases.

In any event, asset-backed auto trader Marshall Motor has proven its ability to outperform the market and continues to invest for growth during a tougher time for the industry.

Marshall Motor is the UK’s seventh biggest motor retailer and is one of only six UK dealership groups that represent each of the top five volume and premium brands.

With a strong presence in eastern and southern England, Marshall Motor is growing share in a testing UK automotive market organically and by using its balance sheet to acquire dealerships to boost brand presence and regional coverage alike.

Marshall Motor uses its own operational tools to improve returns from the underperforming dealerships it buys.

In December it acquired a portfolio of loss-making Volkswagen and Skoda franchises from Jardine Motors in a transaction that shifted Marshall Motor into pole position as Volkswagen UK’s largest partner by number of locations.

Since floating on AIM in 2015, the motor trader has established a track record of either meeting or beating market estimates. That is no mean feat given prevailing sector headwinds. Indeed, despite a further weakening in trading conditions during the fourth quarter of 2019, Marshall Motor was still able to leave its full year outlook unchanged.

For the year to December 2019, and ahead of results due on 10 March, Zeus Capital forecasts lower adjusted pre-tax profit of £21.2m (2018: £25.7m), ahead of £19.1m and £21.2m for 2020 and 2021 respectively, estimates that factor in the short-term dilutive impact of recent acquisitions.

Based on the broker’s 2020 earnings per share and dividend estimates of 19.3p and 8.5p respectively, Marshall Motor trades on a low price-to-earnings ratio of 8.2, implying re-rating scope. Investors are also being paid 5.4% yield to wait for earnings acceleration driven by wider car market recovery. You may need to be patient with this trade and the shares are not suitable for someone who couldn’t cope with a loss to their investment in the short-term.

For those comfortable with the risks, it is worth noting that Marshall Motor trades at a discount to the £125m of freehold and long leasehold assets on the balance sheet.

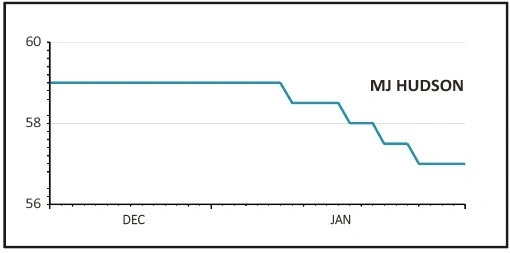

MJ HUDSON (MJH:AIM)

Fresh to the stock market, MJ Hudson (MJH: AIM) is a consultancy to the global alternative asset management industry providing advice on areas such as compliance, regulation, reporting, legal and ESG issues.

Clients include the world’s largest private equity, private debt and hedge funds as well as real estate and infrastructure funds with combined assets of more than $1trn.

Unlike traditional asset managers, who are seeing their fees squeezed relentlessly, alternative managers are still able to charge healthy levels of fees with no sign of ‘compression’.

The fact that MJ Hudson went ahead with its share listing on general election day – despite the potential binary outcome of the vote – speaks volumes about founder and chief executive Matthew Hudson’s resolve.

‘Institutions were amazed and delighted that we went ahead with our float when everyone else had pulled theirs,’ says Hudson. Given his connections with the world of private equity, there was strong demand to sell the company privately, but Hudson opted instead for the public markets where investors were receptive to the long-term growth story.

Strong investor demand for alternative assets and high levels of cash in the industry mean MJ Hudson has good visibility on future revenues. It takes a fee each time a client launches a fund and earns a retainer during the fund’s life, including the wind-down phase.

A second tailwind is increased regulation. Each time there is a new piece of legislation ‘the phones ring off the hook’ says Hudson. Anything that causes aggravation and an increased workload for clients is good for its business.

A third tailwind is the wave of money coming into the ESG space as investors look for more clarity on environmental, social and governance issues. To this end Hudson acquired Dutch ESG consultancy Saris, now re-named MJ Hudson Spring, to help clients incorporate ESG criteria into their investing and reporting.

The firm has grown rapidly since Hudson started it, with 33% annual revenue growth over the last three years alone, but it has plenty of room to continue growing as it adds more partners, clients and services. As a trusted party it also has the potential to cross-sell services such as its recently-developed data analytics tool.

With an experienced management team and strong industry tailwinds, we think MJ Hudson is a great way to play the growth in alternative assets without having to take market risk.

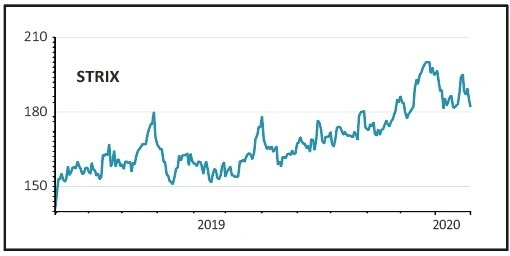

STRIX (KETL:AIM)

Strix (KETL:AIM) is the global leader in the design, manufacture and supply of kettle safety controls, while it is developing complementary products ranging from on-demand hot water to water purification.

While growing and defending its leading market positions (38% globally) in the kettle control market, the company aims to leverage its global sales and distribution networks to grow into adjacent disruptive product niches.

Strix estimates that across all its product categories there is a £1bn revenue opportunity up for grabs, which dwarfs its current £100m revenue.

To give a sense of the company’s ambition it has an agreement with China to build a factory which will be more than two times the size of its current premises with 50 years of rights-of-use granted for the land. The project is expected to be completed in August 2021.

Strix is currently valued at 11.9 times forward earnings, a rating which doesn’t capture the quality of the business or its significant growth prospects.

Kettles are replaced every 3.5 years on average which effectively secures around 90% of annual revenues.

The company has high market shares in the regulated parts of the world (61%) while in the faster growing, less regulated markets, it has a smaller (22%) but growing share.

In China, despite the challenges of protecting intellectual property rights the company has built a share of around 50%, testament to the strength of its product range and innovation.

The entire adjacent product ranges have similar characteristics: convenience, safety, speed and energy efficiency. The company has collaborated with Mr. Coffee in the US to launch a high quality coffee machine, while in China it has launched the ‘true boil’ appliance.

In water purification, alongside the AquaOptima range in the UK, Strix aims to launch 16 new products internationally by 2021 including filters, jugs and bottles.

Baby care products have seen huge demand in China in recent years and according to the China Britain Business Council, international products are perceived as better quality, safe and more reliable than their Chinese equivalents.

Strix offers investors access to the sustainable long-term trends of improving consumer convenience and safety, supported by increasing regulation.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Education

Exchange-Traded Funds

Feature

Great Ideas

Great Ideas Update

Money Matters

News

- China trusts under pressure from coronavirus fears

- Sales growth challenges weigh on Diageo and Unilever shares

- The key challenges facing new BP boss

- Surging stock prices mask concerns about a US economic slowdown

- The companies in the race to find a coronavirus cure

- Burford Capital shares gain despite earnings warnings