Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineIt’s Brexit time: experts say UK stocks could soar

The general election result has removed one of the major hurdles to investing in UK stocks, namely political uncertainty. Brexit is the next big hurdle and it may not be as bad for UK stocks as investors might think, according to numerous fund managers interviewed by Shares.

Despite the UK having to negotiate a full trade deal by 31 December 2020, the fund managers we questioned are generally positive on the economic outlook and the prospects for stocks this year.

‘After three and half years as an investment pariah, the election of a business-friendly and stable government for the next five years could lead to it being regarded as an investment ‘safe haven’. Overall, we expect this to lead to renewed capital allocations to the UK stock market,’ says Gervais Williams, manager of the LF Miton UK Multi Cap Income Fund (B41NHD7).

WHAT HAPPENS NEXT WITH BREXIT?

Although the UK officially leaves the union on 31 January, there are one or two more fences to jump. During this ‘transition phase’ the UK is still effectively inside the EU’s customs union and single market but has no representation in Brussels.

If talks stall, the Government has until 30 June to ask for an extension to the transition period though it has indicated that it has no interest in extending the deadline.

If talks go well, 31 December is the final date for the UK and the EU to agree and ratify a trade deal. Assuming a deal has been reached, we get a new era of trade and political relations; if no deal has been reached the UK faces the prospect of tariffs on all exports to the EU, harming British firms.

So while many big investors are bullish on UK stocks, it is important to understand that trade negotiations could still cause turbulence in the market and it won’t necessarily be a smooth ride upwards.

MARKETS DISLIKE UNCERTAINTY

It’s the oldest refrain in the book but with good reason – markets really don’t like uncertainty. Due to the political and economic risks of the general election and Brexit, overseas investors have mostly shunned the UK market and in particular domestic-facing stocks since 2016. Getting the election ‘done’ has already helped to change that view.

In addition, the IMF expects the UK to be the fastest-growing European economy this year. That may not be saying much, given the low growth rates forecast for many core European economies, but it’s another reason for investors to look at the UK market beyond valuation. Moreover, there are signs that the economy is actually improving.

INDUSTRIAL CONFIDENCE HAS TURNED POSITIVE

Since the election, the data from economic surveys has been uniformly positive. January’s Confederation of British Industry (CBI) quarterly manufacturing confidence survey recorded the biggest three-month jump since it began in 1958. The survey found a net 23% of firms are optimistic about the outlook against a net 44% of firms who were negative in the October survey.

According to the CBI’s deputy chief economist Anna Leach, ‘firms are now planning to invest more in plants and machinery, which will ultimately help increase capacity and output’.

Also, the January flash Purchasing Managers’ Index published last week by IHS Markit and the Chartered Institute of Procurement & Supply (CIPS) showed a ‘decisive change of direction for the private sector economy’ following the election. Business activity expanded for the first time in five months, driven by the sharpest increase in new work since September 2018.

EMPLOYMENT REMAINS STRONG

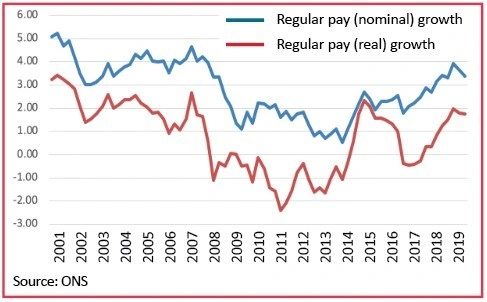

The latest labour market figures from the Office for National Statistics (ONS) show the UK employment rate at a record 76.3% in November 2019, 0.5% lower than the previous quarter.

‘While Brexit has captured a lot of the headlines, the key is going to be what is happening to employment, wage growth and inflation in the UK. Employment still remains at record levels and wage increases are now running 2% ahead of inflation which should mean that domestic spending remains robust,’ says Andy Brough, co-manager of Schroder UK Mid-Cap Fund (SCP).

Despite record levels of employment, the proportion of men in work is no higher than it was in the late 1980s or 1990s. This suggests that employment could continue to rise without excessive upward pressure on wages, which are currently growing at 3.4% before inflation or 1.8% in real terms.

Simon French, chief economist at Panmure Gordon, agrees. He says: ‘There are signs of a pick-up in hiring intentions in the latest survey data and the UK economy keeps confounding estimates of how low unemployment can go without generating sustained wage inflation.

‘As such we expect employment to continue to grow during 2020, however the pace of growth is likely to be slower than in recent years as capacity and skills shortages are a growing issue.’

PROPERTY MARKET AND CONSUMER CONFIDENCE STIRRING

Miton’s Williams believes that with the political logjam now cleared, there could be more money earmarked for investment in UK property. ‘Indeed, there is evidence that this has already started to occur, with Savills (SVS) highlighting it in its recent trading statement. Overall, we believe that this could drive down the yields on industrial and some regional office buildings.’

Simon Gergel, manager of Merchants Trust (MRCH) and head of UK equities at Allianz, is equally upbeat on commercial property. He comments: ‘We have already seen some direct property investments secured from overseas investors, post the general election, and we would expect more to follow. A lessening of uncertainty should encourage tenants to sign leases and investors to put money into the sector.’

There are already signs that industry confidence is improving. The Royal Institute of Chartered Surveyors’ (RICS) indicator jumped to a net 35% of positive respondents in December against 12% the previous quarter even though less than half the responses came in after the general election. In infrastructure, 19% more surveyors said they saw a rise in work than a fall in coming months while in private housing a net 9% of surveyors reported a rise in activity.

Schroders’ Brough suggests that the Government could help the housing market by lowering stamp duty in the upcoming Budget.

Consumer confidence also appears to be recovering. Shortly after the election, GfK’s December survey showed a sharp rise as respondents became more optimistic not just about their own finances but about the wider economy. Director Joe Staton called it the most ‘robust increase in confidence since the summer of 2016’.

Importantly for retailers, GfK’s Major Purchase Index also jumped last month and is now above its December 2018 level suggesting that consumers are more confident about spending on larger items.

In Ipsos Mori’s latest global consumer confidence poll published earlier this month, the UK registered the largest gain of any country in the ‘economic expectations index’.

OUTLOOK FOR STERLING AND INFLATION

The net effect of the election and the raft of positive economic and sentiment surveys has been to push the pound to a five-week high against the euro while against the US dollar it is steadily gaining ground again.

There had been speculation that the Bank of England was readying a 25 basis point or 0.25% cut in official interest rates in response to the tide of weak Christmas trading reports of the last few weeks. However the strength of the latest surveys suggests a rate cut isn’t needed for now so sterling is free to continue its advance.

A strong pound means less imported inflation, as Panmure’s French points out: ‘Near term, inflation is set to head lower as a stronger pound, benign energy costs and lower utility bills all weigh on UK prices.

‘Towards the end of 2020 we are likely to see a rebound as some of these base effects evaporate. I remain relaxed about structural inflationary pressures, despite a tight labour market, as expectations among households and businesses remain well-anchored.’

Miton’s Williams concurs: ‘Sterling will gradually appreciate, which would defray a potential increase in the cost of food, energy and clothing imports. Overall, we believe that UK inflation will remain modest.’

OUTLOOK FOR CORPORATE EARNINGS AND TAKEOVERS

On the whole, fund managers are less concerned about corporate earnings this year. ‘Overall, we believe that corporate growth in the UK is unlikely to differ much compared with others and run at say just over 5% over 2020,’ says Williams.

He adds that if the pound is strong, the international profits of multinationals listed in the UK would translate into lower UK earnings, so in this case earnings might grow at an even slower pace.

Allianz’s Gergel believes Brexit is unlikely to be a massive driver for UK quoted company earnings this year, not least because the majority of sales and earnings come from overseas.

‘Few large quoted companies are very dependent upon the Brexit outcome,’ he says. ‘In addition any disruption from Brexit is unlikely to hit the economy in 2020, or not until the last few months, given the transition period.’

On the other hand, other managers were optimistic about the prospect for an increase in corporate activity. According to James Lowen, co-manager of the JO Hambro Capital UK Equity Income Fund (B8FCHK5), the election result and progress on Brexit should unlock allocation and flows into the UK stock market. ‘As a result of the greater clarity, we expect corporate activity to increase sharply, particularly for UK-focused stocks. We would not be surprised if 2020 was a record year on this front.’

A pick-up in mergers and acquisitions would theoretically provide a stronger backdrop for investment banks, deal advisers and legal firms which advise on corporate transactions.

FUND MANAGERS POSITIVE ON MARKET DIRECTION

The Government has set a fairly ‘demanding’ timeline to complete negotiations with the EU over the final terms of the UK’s exit, according to Miton’s Williams.

However, he says the good news is that the status quo is the default position. ‘In our view the Government will have to prioritise a relatively narrow agenda to have any chance of an agreement.

‘Overall, we don’t expect the Brexit negotiations to have a significant influence on the outcome of the UK stock market over 2020,’ he adds.

Allianz’s Gergel is similarly upbeat. ‘Markets may start to worry about the ability to agree a trade deal later in the year, so there are likely to be some sentiment swings along the way this year and possibly into 2021 if trade negotiations are extended.

‘Overall, however, we expect a greater focus on company fundamentals in 2020 rather than big sector and style-driven sentiment swings which have been prevalent since the referendum in 2016.’

Panmure’s French believes a pragmatic approach to some of the trade-offs that come with greater political and economic sovereignty will reassure investors that the Government will avoid unnecessary trade frictions. ‘This could lead to a rapid revaluing of UK assets after more than three years when the UK has been out of favour amongst international investors.’

Moreover, as James Henderson, director of UK investment trusts at Janus Henderson, points out, ‘the market is pricing in some delay to the final deal and some economic cost, so for Brexit to be quick and relatively painless would be the least expected outcome.’

WHICH AREAS OF THE MARKET COULD

DO BEST?

Williams sees mid and small-cap stocks as the most likely beneficiaries of new fund flows into the UK market.

‘This pattern has already been evident in the mid-caps over the final quarter of 2019, but at this stage the new wave of capital hasn’t drifted down the size bands into small caps, and ultimately into the micro-caps.

‘Furthermore, since many of the share prices of small and micro-caps have been dropping back over the last 18 months, we anticipate that the period of small and micro-cap catch-up could be quite marked.’

Kartik Kumar, manager of the Artemis Alpha Trust (ATS), believes that ‘recency bias’, where investors put an undue weighting on recent events – in this case the political paralysis of the past three years – may be clouding the significance of December’s election outcome.

‘I would argue that the prospects for a UK bank before the election result and today are not the same. And yet prices indicate they are, with most UK banks share prices flat to down.

‘UK banks’ such as Barclays (BARC) and Lloyds (LLOY) could benefit from a pick-up in the economy and are being priced for disruption when further digitalisation could, in fact, benefit their large incumbent customer bases and lower costs.’

He has a similar view with retail, saying there is significant change underway as the strong become stronger and the weak fall away.

‘In this sector, companies such as Dixons Carphone (DC.) and Sports Direct owner Frasers (FRAS) occupy leading market positions but have been dragged down by the wider industry turmoil – unlike operators like Boohoo (BOO:AIM) and JD Sports (JD.) where their leadership is already recognised by the market.’

THREE WAYS TO PLAY A POST-BREXIT UK STOCK MARKET BOUNCE

Vistry (VTY) £13.71

The clear Conservative majority has given the housing market some much needed certainty which is a boost to the housebuilders. This

sector is a good way to play stronger demand for UK stocks.

Vistry, until recently known as Bovis Homes, should be on a growth path following its £1.14bn acquisition of construction firm Galliford Try’s (GFRD) housebuilding and regeneration divisions.

The company hopes to deliver synergies of £35m over the coming years as it integrates these businesses.

Industry veteran Greg Fitzgerald led the repair job at Vistry after it ran into trouble over build quality in late 2016 and early 2017 and, after taking a step back to make improvements to its operations, the firm is now very much on the front foot.

Although the acquired businesses made no contribution to the 2019 financial year and the company faced some pressure on sale prices, strong cost control and easing build cost inflation mean it still expects to report a record adjusted pre-tax profit of £181.6m for 2019, slightly ahead of estimates.

Peel Hunt’s forecasts put Vistry on a 2020 price-to-net asset value of 1.3 times, below the sector average of 1.8 times, and between 2019 and 2021 earnings per share is expected to advance more than 40%.

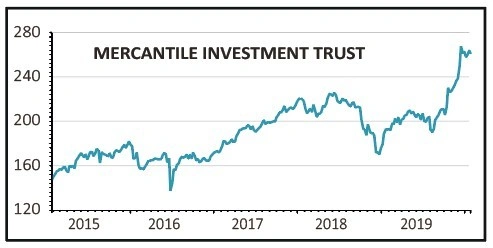

Mercantile Investment Trust (MRC) 261p

JP Morgan’s 135-year-old Mercantile Investment Trust aims to provide income and capital growth through investing in UK mid and small caps that have good track records and significant room for growth that isn’t recognised by other investors.

In addition the trust aims to deliver long-term dividend growth which at least matches inflation.

The trust’s bias to medium and small sized companies provides diversification to a portfolio which might be focused on UK large caps.

The £2.3bn fund’s share price has doubled in value over the last five years while the underlying portfolio has delivered a 76% return compared with the benchmark’s return of 48%.

Managed by Guy Anderson and Anthony Lynch, the pair focus on stocks that have disappointed or been neglected by the market where there is an attractive valuation and a catalyst to drive the share price higher.

The top 10 holdings feature exposure to consumer goods and financials, such as alternative asset manager Intermediate Capital (ICP), housebuilder Bellway (BWY) and fantasy miniatures company Games Workshop (GAW).

Financials and industrials make up half of the portfolio with consumer services and consumer goods another third.

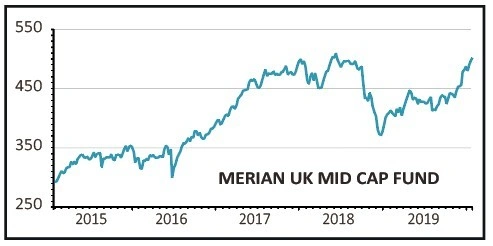

Merian UK Mid Cap Fund (B1XG948) 339p

The £3.3bn Merian UK Mid Cap Fund invests at least 75% of its assets in UK mid cap shares and aims to deliver returns greater than the FTSE 250 ex-investment trusts index over three-year rolling periods.

The fund has delivered an 81% return over the last five years compared to 48% for the benchmark.

Lead manager Richard Watts has managed the fund since January 2009 and heads a team of five fund managers and three analysts.

The team’s flexible investment approach means that they adapt to the changing economic conditions. For example, if the economy is in a recovery phase, the team will look for companies likely to respond quickly to new growth.

The fund currently has 97% of the portfolio invested in mid and small cap shares with the largest weighting towards consumer cyclical and real estate stocks which make up close to half

the portfolio. Financial services represent 12% of the portfolio.

The top 10 holdings include online fashion retail company Boohoo which represents 9% of the portfolio, media outfit Ascential (ASCL), office space supplier Workspace (WKP) and challenger bank OneSavings Bank (OSB).

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.