Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineDon’t expect the gold price to keep soaring in 2020

Cash is trash, hold gold’ was one of the prevailing sentiments from last week’s World Economic Forum.

Echoed by several big money managers, billionaire investor Ray Dalio suggested investors should allocate at least 5% of their portfolios to gold and perhaps as much as 10%.

For those looking to get exposure to the shiny metal in some way, according to the World Gold Council there are three main things to look out for when it comes to gold this year – financial uncertainty and lower interest rates, weakening in global economic growth, and gold price volatility.

WHY BUY GOLD?

Gold can do well when there’s uncertainty, both financial and geopolitical, as it’s considered a safe haven asset.

Swiss government bonds and the Japanese yen are also examples of

safe haven assets, but gold is seen as the ultimate one because it is a physical asset and can’t be printed like money and hence have its value changed that way.

Lower interest rates from the US central bank also tend to boost gold prices because rate cuts drag the dollar down, making dollar-denominated assets like gold cheaper for investors holding other currencies.

Last year saw gold have its best performance since 2010, rising by 18.4% in US dollar terms. It also outperformed major global bond and emerging market stock benchmarks in the same period.

Between the start of 2015 and the end of 2018, gold traded in a $1,100 to $1,350 per ounce trading range. It then shot up in 2019 with a low of $1,268 and a high of $1,520 per ounce, based on daily closing prices.

So far in 2020, the price of gold has gone from a low just below $1,500 to a high of $1,569 per ounce.

REASONS NOT TO GET CARRIED AWAY

UBS analyst Joni Teves says January is typically a strong month for gold. She comments: ‘Over the past decade, January tends to be a strong month for gold prices, a combination of more robust support from physical markets given seasonal demand in China ahead of the Lunar New Year holidays and likely some investor positions being built at the start of the year as portfolios are rebalanced.’

Analysts at Berenberg have taken a somewhat conservative view and don’t see it going much higher than where it is at the moment.

Laurent Kimman, equity research analyst at Berenberg, thinks gold is likely to stay around the $1,500 mark this year, and actually go down to around $1,350 per ounce in 2021 on expectations that rates will not continue to fall.

‘The gold price tends to outperform in a rate-cutting environment, like we saw last year. Despite pressures from the US president on the Federal Reserve for an even more supportive monetary policy, recent FOMC minutes have pointed to a stabilisation of interest rates.

‘Given that gold is a non-yielding asset, rising interest rates increases the opportunity cost of holding gold and therefore pushes the gold price lower.’

Kimman rubbishes the belief that gold will hit the $2,000 mark as suggested by many other market commentators. For that to happen there would have to be some unforeseen macroeconomic shock (such as the killing of Iran’s General Soleimani), but even then Kimman says any rise in gold would only be temporary, with the fundamentals surrounding the metal putting downward pressure on its long-term price.

Only a global recession would push gold upwards for any prolonged period of time, he adds, but most economists don’t see that happening during this year at least.

Examples of gold miners on the London Stock Exchange

Outside of the FTSE 350, examples of gold miners on the London stock market include Russian miner Petropavlovsk (POG). It has had several operational problems in the past but appears to be back on track with production in line with guidance.

A more recent market addition is Australian miner Resolute (RSG), which has developed the world’s first fully automated underground mine, located in Mali.

DOES THIS MEAN GOLD MINING STOCKS AREN’T WORTH BUYING?

There is merit in considering gold mining stocks even if the metal price eases back a bit as miners’ profit margins should still be attractive.

Analysts at Jefferies think gold’s performance last year won’t be repeated in 2020, which in their view makes stock selection ‘more important’. Two gold miners they pick out as ones to buy are Centamin (CEY) and Fresnillo (FRES).

FTSE 250 miner Centamin remains their top pick because they see stabilisation

of its operations driving a re-rating in the share price, as well as a robust balance sheet and leading shareholder returns with a 6% prospective yield.

Recent merger interest from Endeavour Mining, in Jefferies’ view, highlights Centamin’s Sukari mine in Egypt as a ‘world-class asset’.

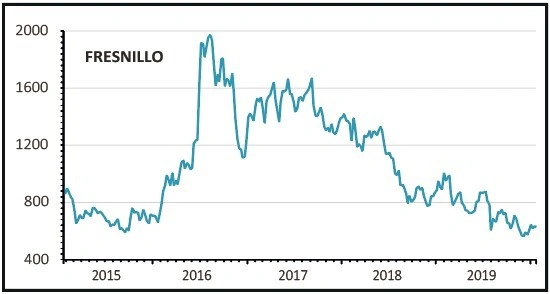

As for Fresnillo, the Mexican miner struggled in 2019. Operational performance and its share price declined in the year.

The analysts expect the second half of Fresnillo’s financial year in 2020 to show more pronounced growth before its Juanicipio mine, which is currently under construction, drives a year-on-year step change in silver production (+16%), earnings before interest, tax, depreciation and amortisation (+23%) and free cash flow (+86%) in 2021.

They’ve put a ‘buy’ rating and 825p 12-month price target on the stock, compared to its current 627p share price.

GUIDE TO FTSE 350 GOLD MINING STOCKS

When looking at gold mining stocks, it’s important to consider their operational history as it can be a tough industry and it is quite common for mining companies to encounter problems when digging gold or other metals out of the ground.

Also key to consider is the company’s all-in sustaining cost (AISC) of producing gold, which looks at the direct and recurring costs to mine a unit of ore. Any AISC below $1,000 per ounce of gold is usually considered good. The AISC and average realised price figures used in this article are the most recent ones published by each company.

Polymetal (POLY)

Market cap: £5.9bn

Forward PE: 10.9

A member of the FTSE 100, Russian gold and silver miner Polymetal has become a favourite with investors thanks to its strong cash flows and operational strength.

Miners can typically be beset by operational difficulties, particularly those mining in remote regions or difficult jurisdictions. But Polymetal has largely managed to avoid such problems and has a good operational track record with a well-regarded management team.

It also performs well on various investment metrics, such as a double-digit return on capital, which at 15.3% stands better than the majority of its peers, while its share price has gone up by a higher percentage than the gold price.

AISC: $904/oz. Average realised price: $1,332/oz.

Fresnillo (FRES)

Market cap: £4.7bn

Forward PE: 27

Mexican gold and silver miner Fresnillo had a tough 2019. Its share price plunged following its half year results in July where it cut the production output guidance and profit forecast.

The company’s problems date back to 2016 when it experienced a technical failure at its San Julian mine milling plant.

But analysts at Jefferies think the company can get back on track and that its new Juanicipio mine will drive a step change in production and earnings when built later this year.

AISC: $1,025.85/oz. Average realised price: $1,320.74/oz.

Hochschild Mining (HOC)

Market cap: £867m

Forward PE: 14.9

Hochschild Mining had an up and down 2019, producing the second biggest amount of gold in its history but failing to fully capitalise on soaring gold prices as it struggled to keep a lid on costs.

The gold and silver miner, which has three mines in Peru and one in Argentina, had to take a $11.9m hit after temporarily closing its Arcata mine in February due to low silver prices time, while it was also hit by higher capital expenditure and the devaluation of the Argentine peso.

AISC: $1,008/oz. Average realised price: $1,329/oz.

Centamin (CEY)

Market cap: £1.5bn

Forward P/E: 17.6

Recently subject to merger talks with Canada’s Endeavour Mining which have since been abandoned, Centamin has long been admired by peers in the sector for its ‘prized asset’, the Sukari gold mine in Egypt.

This is Centamin’s only operational asset and produces around 500,000 ounces of gold a year. It is one of the largest gold deposits in the world with estimated reserves and resources of 15.7m ounces.

The business is eager to diversify geographically and has exploration interests in Burkina Faso and Cote d’Ivoire.

AISC: $1,141 per oz. Average realised price: $1,478 per oz.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.