Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineThe case for including investment funds in the Christmas stocking

As it’s now December lots of people will be starting their Christmas shopping in earnest, but before you buy more toys for your children is there a more lasting present you could get them?

While your child isn’t going to write to Santa asking for a contribution to their Junior ISA, their future self will thank you more than giving them the latest must-have toy.

Parents often lament the sea of plastic toys littering the house after Christmas, so they could leave the present buying to grandparents or family and instead put some money away for their child’s future.

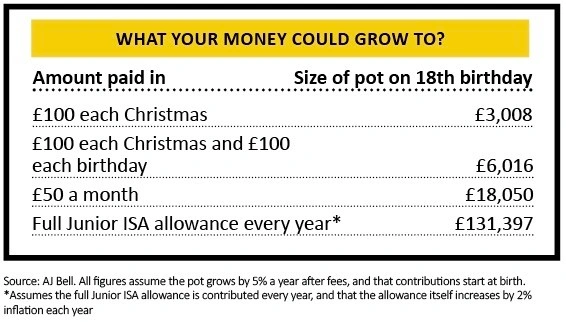

For the price of the latest LOL Doll Glamper fashion camper or Lego set every Christmas (which costs around £100) parents could instead hand their kids almost £3,000 on their 18th birthday. This assumes a £100 contribution every year and 5% a year growth on the pot after fees.

If you go one step further (and are feeling very generous this Christmas) and invested the full Junior ISA allowance each year until they turn 18 you’d be giving them an 18th birthday present worth more than £131,000.

This assumes you put in the full Junior ISA allowance every year (currently £4,368), and that the allowance itself increases by 2% inflation each year, with your pot growing by 5% a year after fees.

HOW TO STOP YOUR CHILD HATING THE PRESENT?

You child isn’t going to be able to parade their Junior ISA account around the playground and show it off to their friends, so understandably might be a bit disgruntled at the gift.

To avoid tears before the turkey, you might agree with grandparents and other family that they still give presents, meaning your kids will have something to unwrap, while you gift money.

You can also use it as a reason for your children to get excited about saving and having money put away. As a starter you could buy them a piggy bank and explain how saving money works. But to get them interested in investing, and give them something to unwrap, you could buy something linked to the investments in the fund you’ve bought.

For example, Nick Train’s Lindsell Train Global Equity portfolio invests in Manchester United, which might appeal to a football-mad child. You could get them a football to go with the Junior ISA. Another example, Witan holds International Consolidated Airlines (IAG), the parent of British Airways, so you could get a small toy plane to bring to life what their money is invested in.

Another parent I know put a small amount of her children’s Junior ISA money directly into shares, but of companies her kids know and use.

She bought some Disney shares for her Frozen-obsessed daughter, while her son got Amazon shares, as he was used to the packages appearing at the door when she ordered things. She then explained the link between buying a Disney film on DVD, via Amazon, and how the company makes money for shareholders.

BUT WHAT SHOULD YOU INVEST IN?

Lots of parents keep their Junior ISA accounts in cash, but the wrapper is really the ideal home for long-term investment with the money locked away for up to 18 years.

But what can you get in cash? The top Junior ISA cash rate at the moment is 3.6% from Coventry Building Society, or 3.25% from NS&I if you want an account you can access online.

Putting the full annual limit into the top cash account every year would give your child £114,000 on their 18th birthday – more than £17,000 less than investing it. Parents putting money in cash accounts also need to make sure the interest rate isn’t subsequently slashed, or that they switch accounts if it is.

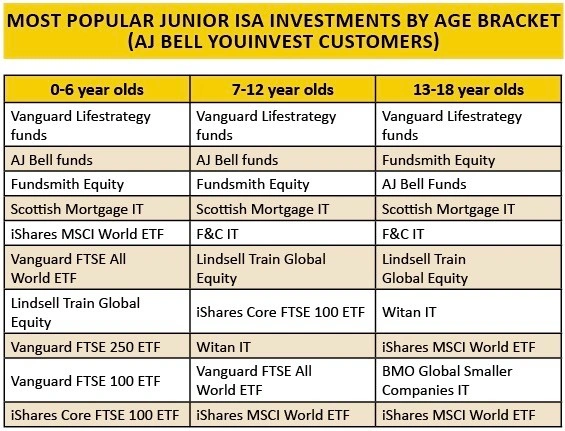

But where are other parents investing the Junior ISA money? Looking at the portfolios of AJ Bell Youinvest accounts parents are investing in a mixture of active funds and passives in Junior ISAs.

A number have plumped for lower cost so-called all-in-one funds, such as Vanguard LifeStrategy or AJ Bell’s passive funds, which spread the money across different markets and mean parents can take a more hands-off approach.

Investment trusts are also very popular, with Scottish Mortgage (SMT), F&C Investment Trust (FCIT) and Witan (WTAN) among the most popular trusts. Among funds Fundsmith Equity (B41YBW7) and Lindsell Train Global Equity (B3NS4D2) are the most popular.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Editor's View

Exchange-Traded Funds

Great Ideas

Great Ideas Update

News

- Japan’s public pension fund bans short-selling on ESG grounds

- Black Friday boost for retailers including Boohoo

- Good and bad: how the Tories and Labour could impact your wealth

- Investors ‘may only see small UK market bounce’ on a Tory majority win

- Activist investor accuses mainstream managers of ‘greenwash’

- What are the prospects for oil prices and big oil firms?