Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

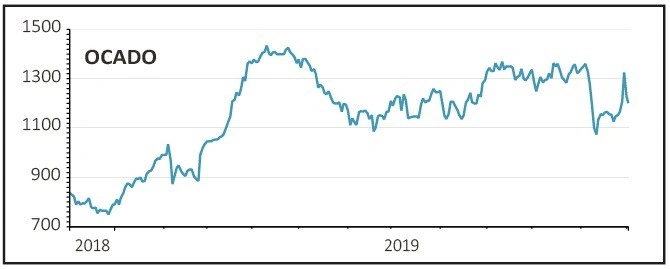

magazineStick with Ocado despite wild share price swings

OCADO (OCDO) £12.19

Gain to date: 2.7%

Original entry point: Buy at £11.87, 25 July 2019

Our ‘buy’ call on grocery delivery solutions firm Ocado (OCDO) has been tested in recent weeks with the shares demonstrating above-average volatility.

Last month the stock sank 20% in short order due to fears of increasing competition from US firms Amazon and Walmart. Last week it rallied sharply on the news of a multi-year agreement with Aeon, Asia’s largest supermarket group, to open up Japan’s £25bn-plus online grocery market.

The first warehouse should be operational in 2023. Aeon expects to have an annual sales capacity in Japan for online orders of Y200bn or £1.8bn – about the size of Ocado’s existing UK grocery delivery business – by 2025, growing to Y1trn or £9bn in 2035 as younger consumers drive online spending.

Finance director Duncan Tatton-Brown claimed last week that Ocado had ‘no immediate need’ for additional funds, yet this week it announced a £500m convertible bond offering, sending the shares spiralling lower.

Although the terms of the deal are highly favourable, negative sentiment towards the stock – 10% of shares are on loan to short-sellers and more analysts have ‘sell’ recommendations than ‘buys’ – is a fact of life and price volatility is likely to continue.

SHARES SAYS: Investors of a nervous disposition may want to exit but we would top up on weakness as the business grows with more global partners.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Editor's View

Exchange-Traded Funds

Great Ideas

Great Ideas Update

News

- Japan’s public pension fund bans short-selling on ESG grounds

- Black Friday boost for retailers including Boohoo

- Good and bad: how the Tories and Labour could impact your wealth

- Investors ‘may only see small UK market bounce’ on a Tory majority win

- Activist investor accuses mainstream managers of ‘greenwash’

- What are the prospects for oil prices and big oil firms?