Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWill UK banks struggle like their Japanese counterparts?

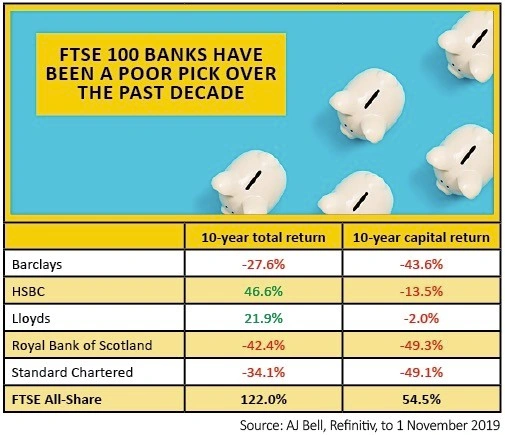

The third quarter results from the FTSE 100’s ‘big five’ banks generally got a cool reception, not least because of fresh payment protection insurance (PPI) compensation claims and other assorted legal and conduct costs of £4.6bn.

As a result, the FTSE All-Share Banks sector is down by 0.4% in 2019 to date, when the FTSE All-Share is up by 9.4%. That leaves the banks ranked just 32nd out of the 39 industrial groupings which make up the index.

But the malaise runs deeper than PPI and (mis)conduct fines. They have only added to the UK-based banks’ deep-rooted challenges where the market is mature, competitive and tightly regulated.

Throw in a grinding drop in interest rates, bond yields and credit spreads and you have a rotten environment for banks, as their share prices over the past decade will attest, even after the hard work to cut costs and rebuild balance sheets.

The question now is whether this environment is going to change. As the source of the crisis that engulfed markets 12 years ago, investors want to see the banks doing well, as that would help to provide a firm footing for the wider economy, whose wheels would be greased by the credit they provide.

Healthy banks would help the stock market too, since consensus analysts’ estimates suggest that the sector will provide 17% of the FTSE 100’s total pre-tax profit for 2020 and 16% of its dividends.

Mangled margins

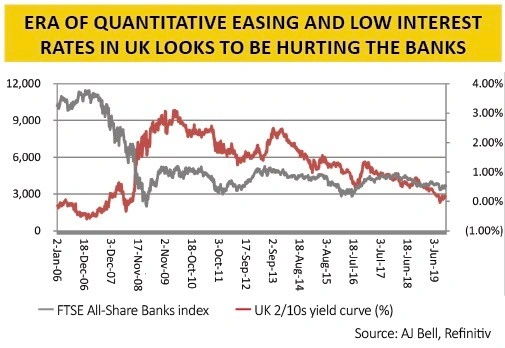

Banks raise money at one interest rate, through deposits or borrowing, lend it out at another and pocket the difference while (hopefully) getting their money back once the loan matures to start the process again. The result is the net interest margin on the loan book and this is a key measure of profitability.

The bad news is margins are under pressure, for three reasons. Interest rates have gone to near zero or even gone negative in some areas. The yield curve has flattened and credit spreads have been compressed.

All three can be seen as an (unintended) consequence of central banks’ low interest rate or negative interest rate policies. The chart may not be totally conclusive (investors must also accept that correlation does not mean causation) but the steady flattening of the yield curve in the UK, as benchmarked by the gap between two-year and 10-year government bonds, does seem to be weighing on the share price performance of the FTSE All-Share Banks sector.

Turning Japanese

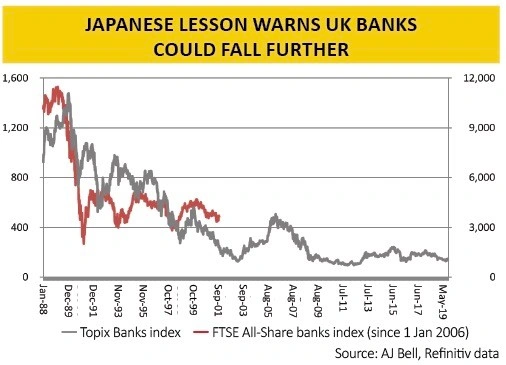

Since its own debt-fuelled property and stock market bubbles burst in 1989, Japan has tried to reinflate valuations and stoke both growth and inflation with negative and low interest rates and quantitative easing policies, with mixed results.

The very fact that the Bank of Japan is still hard at it after nearly three decades hardly smacks of success. Worse, the gradual compression of the same yield curve in Japan looks to have done huge harm to the country’s banks.

The Topix Banks index is down by 90% since its all-time high. By comparison the FTSE All-Share Banks index languishes some 69% below its peak. If history repeats itself – and that remains an if – then things could get worse for the UK banks before they get better.

The final graphic shows the performance of the Topix Banks index from two years before it peaked to today. It then overlays the performance of the FTSE All-Share Banks index starting on 1 January 2006 – two years before the financial crisis really hit – and then runs it over the same time line as the Topix Banks benchmark.

This suggests that UK banks could fall further, if a backdrop of easing and low rates persists or negative rates are introduced and the Bank of England fails to fire growth and inflation. The past is no certain guide for the future and value-hunting contrarians will note with interest the 270% rally in Japanese banks that ran from 2003 to 2006, when it seemed like Japan was finally breaking out of its deflationary debt trap.

That proved to be a false dawn. But it did show what could happen to ‘value’ financial stocks if sentiment changed and investors began to believe in inflation rather than fear deflation, so the UK’s bank stocks could be a good way of judging whether the Bank of England is winning in its efforts to fuel inflation and fend off the spectre of deflation.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.