Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineGeneral election: what the big vote means for your money

Just as it looked like a short-term resolution to the Brexit saga was in sight, with a deal agreed with the EU and subsequently gaining early stage approval from MPs, a refusal by the same MPs to go along with Boris Johnson’s timetable led him to put the legislation on pause and push for a general election.

Johnson, who, as a result, failed to deliver on his ‘do or die’ promise to deliver Brexit on 31 October, at least got his wish election-wise as initially the Liberal Democrats and Scottish National Party threw their support behind the idea and Labour followed in their wake. The outcome is a public vote on 12 December as the Brexit deadline is extended out to 31 January 2020.

It might not provide the immediate clarity craved by markets and the business world, but current polling implies the Conservative Party will secure a solid majority which should smooth the eventual passage of Brexit through the House of Commons.

This explains why UK assets like sterling, gilts and real estate have largely taken the election news in their stride. That could change if the polls tighten and a hung parliament or even a Labour majority is perceived to be a more realistic prospect, with all the uncertainty that would bring.

WHY THE ELECTION MATTERS TO YOUR MONEY

In this article we look at what could happen to your investments, personal finances and more depending on the outcome of the looming election.

One point for investors to consider is that, even if the Conservatives prevail and complete the UK’s withdrawal from the EU, the hard bit arguably begins with the task of securing a free trade agreement with the EU.

The current transition period ends in December 2020 and most people think getting an agreement will take longer. Any request for an extension to the transition would need to be submitted by June 2020 and Johnson has indicated an unwillingness to do so.

What are the polls telling us?

On 29 October the Financial Times poll tracker, which collates and derives a weighted average from a range of published polls, gave the Conservative Party a clear lead.

The vast majority of polls have given the Conservatives a double-digit advantage. Before you think a Conservative majority is nailed on, consider that pollsters have consistently been wrong in calling the big votes in recent years and there are several reasons why the result is unpredictable.

First, plenty can change over the course of an election campaign. In 2017 Theresa May’s government enjoyed an even stronger lead over Labour before the polls tightened considerably and eventually she lost her majority.

The difference this time round is that Johnson is seen as a better campaigner than May and Jeremy Corbyn’s personal ratings are the worst on record for an opposition leader – not helped by an anti-semitism scandal in the party.

The other factor making the election hard to call is the volatility of the electorate which is no longer as attached to the main parties and look to be split along remain-leave lines.

FIVE BIG QUESTIONS

1. Will the election be about Brexit?

If yes, this is probably good news for the Liberal Democrats and Tories as their positions are seen as being clearer (cancel Brexit, deliver Brexit respectively) than Labour’s fence-sitting approach (negotiate a new deal, put it to a referendum). Labour will hope to fight the election on areas like the NHS and reversing austerity.

2. Will the Liberal Democrats take seats from the Conservatives in remain-orientated constituencies?

3. Will the Conservatives lose a large number of their 13 Scottish seats?

Johnson is unpopular in Scotland and the country voted to remain in the EU across all council areas. But fans of the union might not vote for the SNP – which won 56 of the 59 seats in Scotland in 2015.

4. Can the Conservatives pick up seats in leave-voting traditional Labour constituencies?

Theresa May failed to achieve this in 2017. There remains strong aversion to voting Conservative in many of these areas which could make them hard to crack. There is potentially a greater willingness to vote for the Brexit Party which doesn’t carry the same baggage.

5. How many seats will the Brexit Party stand in?

It won the biggest share of the vote in the European elections in May but Johnson’s harder stance on Brexit has hit its polling numbers. If, as promised, the party puts up a candidate in every constituency then it could split the leave vote and impact the chances of the Conservatives winning seats from Labour. But suggestions it might target a much smaller number of seats where it feels it has a strong chance would be a significant bonus for Johnson and the Tories.

Two referendums under Labour?

One of the Conservative Party’s lines of attack in the election is that a Labour government would serve up two referendums in 2020.

If Labour is to take power it seems unlikely it will be able to do so by forming a majority and the price of forming a coalition with one of its likely partners, the Scottish National Party, may be a further vote on Scottish independence along with the second referendum on EU membership already promised.

Companies with exposure to Scotland, and which saw some share price volatility five years ago on the previous vote, include financial firms Standard Life Aberdeen (SLA) and Royal Bank of Scotland (RBS) as well as defence businesses with material operations north of the border like BAE Systems (BA.) and Babcock (BAB).

HOW THE ELECTION RESULT COULD IMPACT STERLING, INVESTMENTS, TAX AND PENSIONS

THE POUND

If polling continues to point to a big Conservative win in the election then sterling will probably remain in a holding pattern until the results come in. Confirmation of a Tory majority would likely give the currency a short-term boost.

Bill Dinning, chief investment officer at Waverton Investment Management, comments: ‘There are still many risks to sterling during an election campaign.

‘Many of the issues that truly concern the electorate – the NHS, schools, student debt, housing shortages, general malaise about living standards – are seen normally as “Labour issues” by which I mean that opinion polls tend to indicate that Labour is seen as better at dealing with them.

‘But we do not live in normal electoral times and the Labour Party’s divisions are a headwind for the party which may diminish their traditional strength in those policy areas.’

If the election starts to move towards those issues and away from Brexit, and if that is reflected in the polls, then you would expect sterling to retreat.

Nigel Green, CEO of financial adviser deVere, says: ‘Expect the pound and UK financial assets to be increasingly volatile in the run-up to the general election, given the wide-ranging set of outcomes.

‘The most detrimental of these outcomes for sterling, UK financial assets and the wider British economy, include another hung parliament or a victory for Jeremy Corbyn’s Labour Party.’

However, if Labour were to form a coalition and call a second referendum with remaining in the EU as an option, this could be positive for the pound in the long term, assuming it delivered a ‘remain’ result.

INVESTMENTS

The lead-up to an election could potentially benefit media group YouGov (YOU:AIM) which is best known for polling. The results this time round could be very close to call and so YouGov is likely to be in hot demand to constantly measure how the public is thinking ahead of the big vote.

In normal circumstances, Royal Mail (RMG) would pick up more work from an election as political parties seek distribution for their campaign literature. Postal votes would also give Royal Mail a boost but the big question mark is whether strike action threatened by members of the Communication Workers Union would disrupt the business at a crucial time.

Failure by Labour to get elected could trigger a big rally in several different parts of the stock market as a sigh of relief by investors, given how many Labour-related policies have already been priced in to many sectors.

HOW LABOUR HAS WEIGHED ON SHARE PRICES

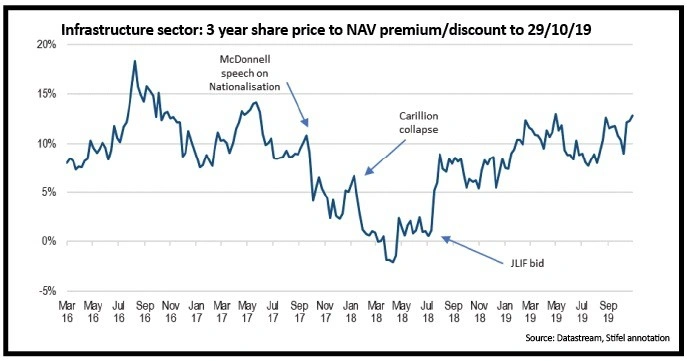

Jeremy Corbyn has previously threatened to renationalise the utilities sector which has weighed on the price of shares in numerous electricity, gas and water providers and has fed through to parts of the investment trust infrastructure space. These funds are exposed through private finance initiatives (PFI), where public sector projects are delivered by the private sector, and through direct exposure to infrastructure assets or utilities themselves.

Removing the threat of Labour meddling with the sector could make the utilities space far more exciting to investors than it normally is. By extension it could also see many infrastructure-related investment trusts trade on higher premiums to net asset value as more investors could feel comfortable paying up to access a stream of dividends backed by long-term cash flows.

Investment trusts HICL Infrastructure (HICL) and International Public Partnerships (INPP) are considered to be among the most exposed to projects that could be negatively impacted by Labour’s plans, so a defeat for Corbyn could see those funds experience a notable relief rally.

The reverse of this situation, namely Labour getting in power, would naturally be negative for the utilities sector as well as the transport industry where Corbyn has also threatened change.

However, there remain big questions over how Labour would fund a large renationalisation plan. The Confederation of British Industry initially put the cost of such a scheme at £196bn but subsequently admitted that might have been over-exaggerated.

LABOUR’S TAX PLANS

Labour getting into power could be negative for all UK companies as it wants to raise corporation tax from 19% (or 17% from April 2020) to 26%. Two years ago Corbyn vowed to introduce an excessive pay levy which would require companies to pay a levy of 2.5% for individual staff earning more than £330,000, increasing to 5% for earnings above £500,000.

The party has also floated the idea requiring companies with more than 250 employees to transfer annually at least 1% of their ownership into an inclusive ownership fund controlled by workers, up to a maximum of 10%. These shares would not be sold or traded, thereby reducing a quoted company’s stock liquidity.

Workers would get dividends up to £500 a year with any surplus from dividends paid into a national fund to be used for public services and welfare. Labour has estimated the cost to business would be £2.1bn a year, however many British firms are unlikely to welcome such measures and, in a worst case scenario, such a policy could result in them moving their stock market listing overseas.

TORIES TO PROVIDE MORE CERTAINTY?

A Conservative majority outcome would likely give sterling a boost and therefore provide a lift to UK domestic companies on the stock market and the FTSE 250 index.

Investors want to know what’s going on with Brexit and having a Conservative majority would remove some of the uncertainty. While many people might not like how Brexit will play out, at least they would have a better idea of what to expect with a Conservative majority government and clarity is what really matters to the markets in the short term.

But a hung parliament result could put the market is disarray once again and weigh on sterling as well as banks and housebuilders in particular as these sectors are often seen as proxies for the UK economy and barometers for Brexit. Investors may start to panic about more deadlock which could lead to further chaos on the markets.

WHAT COULD HAPPEN IF LABOUR WINS?

Potential weakness in the utility, transport and infrastructure sectors

Businesses could clash with Labour over tax and employee ownership plans

Expect general stock market weakness in the short-term

WHAT COULD HAPPEN IF CONSERVATIVES WIN (WITH A MAJORITY)?

The pound could rally

UK-focused companies could surge in value, particularly banks, housebuilders and businesses serving consumers such as leisure groups, retailers and supermarkets

Stocks previously marked down for Labour Party-specific fears could rebound

WHAT COULD HAPPEN IF THERE IS ANOTHER HUNG PARLIAMENT?

The pound could fall

UK-focused companies could drop in value

Investor and business sentiment could wane

INCOME TAX

The Conservatives want to hike the point at which the 40% income tax rate kicks in, from £50,000 to £80,000 in England, Wales and Northern Ireland, which represents a 60% hike. The move would affect around 4m people, and the highest earners in that group would get an extra £2,500 each year.

Labour wants to bring more people into the 45% tax bracket, reducing the threshold at which you start paying it from £150,000 down to £80,000. It wants to introduce a 50% tax rate for those earning over £123,000, in a move that could raise billions for the public purse, but cost the highest earners the most.

INHERITANCE TAX

Labour has pledged to scrap the current inheritance tax system and instead cap the amount everyone can receive in inheritance across their lifetime at £125,000. Any gifts received above this level would be taxed at income tax rates.

The Conservatives also seems to be thinking about making changes to the inheritance tax system with Chancellor Sajid Javid saying ‘it is on his mind’ at a recent event. According to reports, he believes there is an issue with people who have already paid tax through work or investments having to pay tax again.

‘Javid has already said he is a fan of simplified taxes, and as the Government has already commissioned the Office for Tax Simplification to carry out a review of inheritance tax simplification, it seems a likely area of focus,’ says Laura Suter, personal finance analyst at AJ Bell.

THE PROPERTY MARKET

Boris Johnson has talked about cutting stamp duty on all homes worth £500,000 or less, in a bid to stimulate the property market.

First-time buyers already get a stamp duty break as they pay nothing on the first £300,000 if they buy a property worth £500,000 or less. But Johnson’s plan is to extend this to all buyers and increase the tax-free limit to £500,000. The move would save first-time buyers up to £5,000 and all other homeowners up to £15,000.

Labour is in favour of scrapping stamp duty for homes people will live in themselves and to abolish council tax and replace it with a new ‘progressive property tax’, based on property values.

This would also be payable by landlords rather than tenants, which would put money in the back pocket of anyone renting, and hiked for second homes, empty homes or those owned by non-domiciled residents. The capital gains tax rate for second homes or investment properties would increase too.

Labour has also floated the idea of allowing tenants to buy their homes from private landlords, possibly at a discount to the market rate.

INTEREST RATES

This is a tricky one. Interest rates will be heavily influenced by how Brexit plays out and it is impossible to make any predictions now.

Fundamentally a messy Brexit could hurt the economy, meaning the Bank of England may have to cut rates to stimulate investment and spending. But a better than expected Brexit situation could boost economic activity, at least in the short term. The Bank of England may only seek to raise rates if the economy looks like it is overheating.

Ketish Pothaligam and Peder Beck-Friis, portfolio managers at fixed-income specialist Pimco, are sceptical that any bounce in investment once there is clarity on Brexit will be ‘long-lasting, sharp and meaningful’.

They say UK growth will continue to be shaped by global developments. ‘Over the medium term, Johnson’s Brexit deal would likely lower UK potential growth somewhat, exacerbating the country’s already weak productivity profile.’

PENSIONS

Pension policy is likely to be an area of focus for both parties for several reasons. Firstly pensioners tend to vote in large numbers and secondly an increasingly large chunk of the population have more direct experience of retirement saving outside of the state pension thanks to auto-enrolment in workplace schemes.

Labour might campaign on a platform of slowing or halting entirely Conservative plans to increase the state pension age – currently set to move to 67 by 2028 and 68 by 2039.

All parties seem likely to support the retention of the ‘triple lock’, which sees the state pension rise in line with the highest of average earnings, inflation or 2.5%.

Tax relief attached to pensions (paid as a top-up to contributions at the highest rate of income tax you pay) came at a cost of £38bn in the 2017/18 tax year. Labour seems the most likely to push for reform in this area given pension tax relief is perceived to be more advantageous to the wealthy.

Changes wouldn’t be brought in immediately and it is unusual for tax changes to be retrospective so it makes sense for now to continue to take advantage of the generous relief still on offer through a pension if you can.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.