Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineBig money to be made with this self-storage group

It may not be a glamorous activity but storing the possessions of businesses and households is certainly a lucrative one. Self-storage play Lok’n Store (LOK:AIM) continues to churn out impressive growth numbers and has a clear expansion plan which is underpinned by a strong balance sheet, experienced management and robust market backdrop.

The company provides low cost, secure storage space for companies and individuals. Demand for these services has increased due to smaller homes, a more mobile population and corporate world, and people simply buying and hoarding stuff. At the same time self-storage supply has struggled to keep up.

In the 12-month period to 31 July 2019 the company added five new sites, four of which it developed itself and one which it acquired, taking the total to 34. Around a third of these are not owned by Lok’n Store but managed by the company on behalf of third parties.

Two new stores should open in summer 2020, a further two have had planning proposals submitted, four are currently being designed and six are with lawyers.

The balance sheet looks in good shape to fund the development of this pipeline with a loan-to-value ratio of just 16.1%.

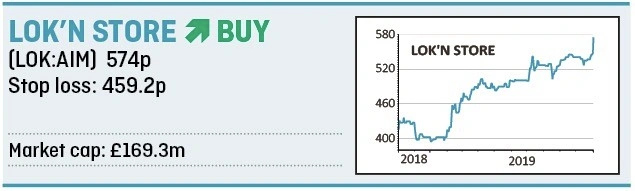

The market has begun to cotton on to the growth story at Lok’n Store with the shares up 43% since we highlighted the firm as a Great Idea in April 2018.

However, the stock remains at a significant discount to its rivals. House broker FinnCap notes it is at a single-digit premium to net asset value in percentage terms compared with a 65% average premium for its self-storage peers despite offering nearly double the growth in earnings.

Lok’n Store’s sites, located in prominent locations and with distinctive orange livery, act as a calling card for its services. Founder and chief executive Andrew Jacobs tells Shares that 40% of its business comes from people who have driven past one of its warehouses.

Pre-tax profit is not a particularly useful metric for measuring the company’s performance as it tends to be impacted by the depreciation of its sites. The company flags cash available for distribution instead – which essentially shows how much cash is available to be paid out in dividends.

This was up 8% in the July 2019 financial year to 19p. FinnCap forecasts this total will reach 53p in the next nine years based on current and secured sites alone.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.