Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineNegative yields have forced investors to explore ‘alternative assets’

It is little wonder that interest in ‘alternative assets’ has exploded.

We live in a world of negative interest rates, where $17tn of bonds including government bonds trade at nominal yields below zero – meaning that if investors held them to maturity, they would lose money not make money – and more than double that amount trades on yields which track below the rate of inflation.

Alternative assets typically include property, precious metals, hedge funds, structured products, private equity, venture capital, fine art, fine wine, classic cars or watches, rare stamps and pretty much any other type of asset which is expected to hold its value due to its scarcity factor.

Given the option of making a certain loss on the ultimate safe investment, government bonds, many investors are opting for less safe investments even though the prospective returns on offer may be low by historical standards. In other words they feel forced to buy risky assets rather than accept a negative return on safe assets.

This isn’t just happening among retail investors, as the Financial Times flagged in August: ‘The flow of pension fund money into any asset that promises to beat zero-rate bonds has been so dramatic that equities, junk bonds, property, private equity and a host of other more abstruse (obscure) areas of investment have spiralled in value.'

PROPERTY AS A LONG-TERM PLAY

Historically residential property has proved a sound long-term investment and has typically generated a return above the rate of inflation if not quite as high as the return on equities. However, specialist knowledge is required as values can vary even down to the level of city streets.

Moreover the cycle is notoriously vicious and following more than a decade of steep price rises, particularly in prime and super-prime property, this is probably not the time to be getting in. Particularly when you consider many of us already have significant exposure to residential property if we own our home.

In fact the Begbies Traynor (BEG) Red Flag Alert published last week showed a significant increase in UK residential property investment companies in what it calls ‘significant financial distress’.

Commercial property is a more interesting proposition, and as well as the big quoted real estate firms such as British Land (BLND) and Land Securities (LAND) there are a wide range of investment trusts.

Office developer Regional REIT (RGL), for example, is a running Great Idea.

GOLD AND OTHER ‘HEDGES’

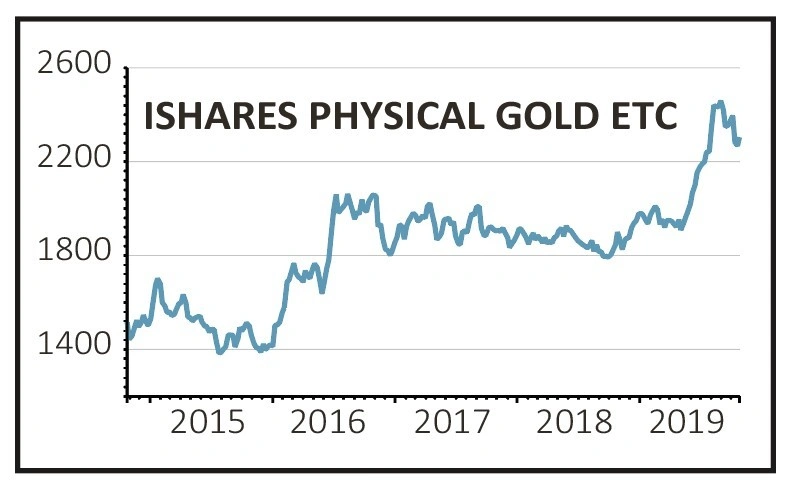

We have covered precious metals, in particular gold, on many occasions and there are arguments in favour of them not least from the point of view of portfolio diversification. Investing via a fund or an ETF like iShares Physical Gold (SGLN) rather than holding the physical assets themselves is probably the cheapest and easiest route to ownership.

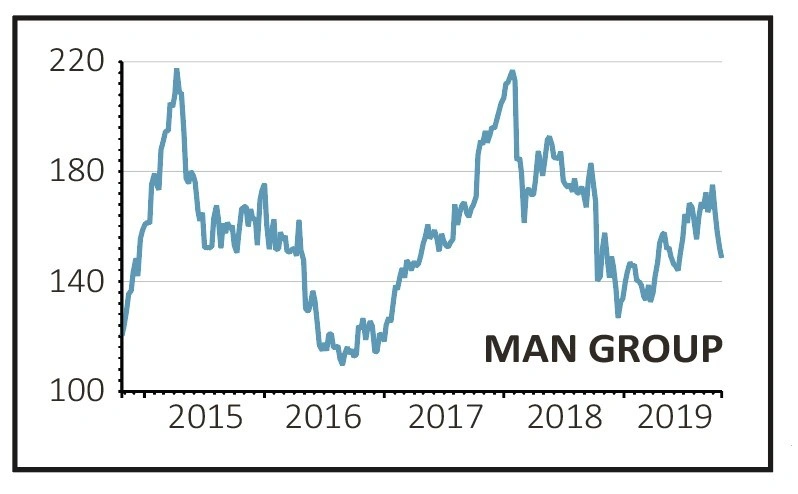

Hedge funds have been unkindly referred to as a compensation system rather than an asset class, given the high level of fees which they charge and their patchy record of beating the market.

In the beginning, hedge funds were indeed a useful hedge for investors as they weren’t highly correlated with markets. The ability to ‘short’ stocks and indices meant that when markets went down they made money, but over time their performance has become more correlated.

When stocks are going up that isn’t a problem, but when they go down the correlation often rises sharply so that just when investors need them to perform well they don’t.

As most hedge or ‘absolute return’ funds require a sizeable minimum investment – typically £100,000 although some demand as much as £500,000 – the easiest way for retail investors to get a slice of the action is to buy shares in Man Group (EMG), which offers exposure to the AHL and Numeric strategies as well as the GLG business.

PRIVATE EQUITY AND VENTURE CAPITAL

As the name suggests, private equity is primarily investment in privately-owned rather than publicly-owned companies, although recently private equity firms have shown quite an appetite for listed UK businesses no doubt due to their relative cheapness.

Deals this year include Advent’s £4bn acquisition of Cobham, TDR Capital’s £1.9bn acquisition of BCA Marketplace and £1.3bn acquisition of EI Group, and Thoma Bravo’s £3.1bn bid for Sophos (SOPH).

There are a handful UK-listed private equity firms, of which one of the biggest and best-performing is the Harbourvest Global (HVPE) investment trust. The £1.4bn fund owns of hundreds of private businesses in the US and across the globe through its holdings in other Harbourvest funds.

Its estimated net asset value (NAV) as of 30 September was £20.94 against a current price of £17.08 meaning its shares trade at a discount of almost 20%.

Investing in private equity through a listed investment trust has the advantage that shares can be bought and sold at will whereas the underlying investments are highly illiquid, and it offers diversification from listed equities.

However due diligence is needed when choosing a trust as performance and therefore discounts can vary dramatically.

Venture capital investing is similar to private equity but even higher-risk as the target companies are typically small start-ups and often have no profits.

Trying to calculate NAVs for early-stage businesses is fiendishly difficult, and unlike private equity funds liquidity in quoted venture capital vehicles is virtually nil so private investors are advised to give them a wide berth.

LESS OBVIOUS BUT LESS LIQUID ASSETS

It’s debatable whether fine art is a serious investment asset. The Fine Art Fund, which was launched in 2004, closed to new investors some time ago and there a few options for retail investors to participate. Also, art like beauty is in the eye of the beholder so values can be subjective.

Unless you have a copy of Leonardo da Vinci’s Salvator Mundi (market value $450m) stashed in the loft, pictures are better off hung on the wall than being used for investment.

Classic cars and watches have always been go-to investments for wealthy collectors and prices have soared in the last decade as low interest rates have forced high and ultra-high net worth individuals to find a return on their money.

As well as vintage Ferraris and Aston Martins, prices of more mundane cars such as 1970s and 1980s BMW and Mercedes sports saloons have raced ahead in the last decade.

A recent GQ magazine feature suggested that would-be collectors start buying original examples of the Fiat 500, Jaguar XJS and Porsche Boxster as investments to tuck away for the next decade. As well as rarity, originality and provenance are key considerations for collectors

In terms of watches, age and rarity don’t necessarily make a watch valuable. Generally speaking the maker and the intricacy of the movement are more important and many modern watches can sell for seemingly astronomical amounts.

However, the world’s most expensive watch – which was sold at auction two years ago – is actor Paul Newman’s 1960s Rolex Daytona. It was neither exclusive nor particularly complicated but due to its provenance it fetched a staggering $15.5m, or nearly £12m at today’s exchange rate, before the buyer’s premium.

Fine wine is another recognised investment field with single bottles from the top producers changing hands for tens of thousands of pounds. Like stocks, investors in wine need to be patient and ride out the cycles but with limited production and with older vintages running out there is constant demand for the best wines.

At the very top end of the market is Domaine de la Romanee-Conti, a Burgundy which costs almost ten times as much as some first-growth wines from the finest chateau in Bordeaux. Eye-wateringly expensive (Berry Bros currently has one bottle of the 2002 vintage on offer for over £21,000), it is almost exclusively for collectors.

Ironically though, the wine market isn’t that liquid although the volume and value of transactions is growing each year. Also, if you sell your wine through a merchant they will typically charge a hefty commission (15% is the bare minimum with some agents charging more than 20%) which can put quite a dent in your profits.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.