Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineFind out about how GlaxoSmithkline is changing

When new chief executive Emma Walmsley took over the reins of GlaxoSmithkline (GSK) in April 2017 she conducted a strategic review of the business. The upshot is that over the last year the company has been undergoing a complete change of direction to become a more focused specialised pharmaceutical outfit.

GSK is the fourth largest quoted company in the UK, representing just over 4% of the FTSE 100.

The company generates £30.8bn of annual revenues and employs over 100,000 people across 150 countries. Each year it spends nearly £4bn on researching and developing new drugs and currently has 44 new medicines in its pipeline.

Last year it delivered around 2.3bn packs of medicine, 770m vaccine doses and 3.8bn Consumer healthcare products.

UNDER NEW MANAGEMENT

Historically the firm had perused a diversification strategy around the three pillars of Pharmaceuticals, Vaccines and Consumer Healthcare.

In June 2018 GSK bought-out Novartis’ minority interest in its consumer healthcare business, so that it controlled 100%.

Then on 3 December 2018 GSK announced the sale of its Horlicks and other consumer nutrition brands by merging the unit with Hindustan Unilever for a total deal value of £3.1bn.

Just four hours later on the same day it announced the $5.1bn acquisition of US biotech firm Tersaro, Walmsley’s first as CEO.

This was a huge initial step designed to bulk up its oncology (cancer) pipeline and commercial capability.

Later in the same month, on 19 December GSK announced the spin-off its Consumer Healthcare division by joining forces with Pfizer and combining the two company’s respective healthcare franchises to create a business with circa £10bn of revenues. The plan is to demerge the new business from 2022.

The combined business will boast iconic brands such as Panadol, Sensodyne and Advil.

GSK’s FOUNDATIONS GO BACK OVER 300 YEARS

GSK is the result of the amalgamation of many different smaller businesses that would later come together through many mergers and acquisitions.

But it may be surprising to learn that the company’s humble beginnings go as far back as 1715 with the opening of a small apothecary shop in Plough Court, London.

Over the years its scientists have made Nobel Prize winning discoveries in their fields of expertise. The company developed the first treatment for leukaemia and gout, as well as HIV in the 1980’s.

In 2014 it produced the first vaccine candidate for malaria and is now embarking on a pilot implementation of the candidate vaccine involving 750,000 children in Ghana, Kenya and Malawi.

HOW DOES GSK MAKE MONEY

GSK’s financial metrics are typical for a pharmaceutical company, and reflect the unique characteristics of the underlying economics.

The biggest challenge is to discover new drugs and successfully bring them to market. The cost of employing thousands of highly qualified staff is also relatively high compared with other industries.

According to a study published in the Journal of Health Economics it costs around $2.6bn to find a new drug and achieve a commercial launch.

More than that, the probability of success is small. Of the entire drug compounds in clinical development, on average only 7% will eventually be approved for marketing.

Medical patents are usually granted for a fixed 20 years. But on average its takes between six to seven years to bring a new medicine to market, which reduces the available time to commercially exploit the invention to around 13 years.

Once a patent expires, revenue usually collapses due to the fact that there are a number of specialty generic pharma companies which have the scale and expertise to manufacture and distribute the product at a fraction of the price of the protected product.

This means that in order to be sustainable, companies like GSK need to have a lot of new medicines in development to replace the current crop of ‘star’ drugs when they go off-patent.

All of these factors have an impact on the business financials and are specific to pharma businesses like GSK.

The gross margin, (revenue minus direct costs), sometimes known as value-add, is relatively high compared with other sectors and at GSK it has averaged around 69%.

Effectively GSK buys raw materials like proteins and solvents for £3 and turns them into around £10 of sales (or £7 of ‘added value’). Saving lives is clearly a very valuable activity and this is reflected in high gross margins.

The low probability of bringing new drugs to market means that lots of drugs need to be developed in order to get just a few to the marketing stage. Therefore R&D is the life-blood of every pharma company and this is reflected in the £4bn of annual expenditure (13% of sales) that GSK incurs just to keep the drug pipeline healthy.

One could argue that GSK has been under-investing relative to its peers because according to consultancy EvaluatePharma, spending as a percentage of sales has averaged around 20% over the last decade for the pharma industry.

Once GSK gets a drug ready and approved to go to market, it needs to effectively market the drug into multiple territories around across the world and these costs are part of the selling and general administration charges, which represent around a third of revenues.

The company historically makes an average operating margin of around 29%.

THE DRUGS THAT WILL DETERMINE GSK’s FUTURE SUCCESS

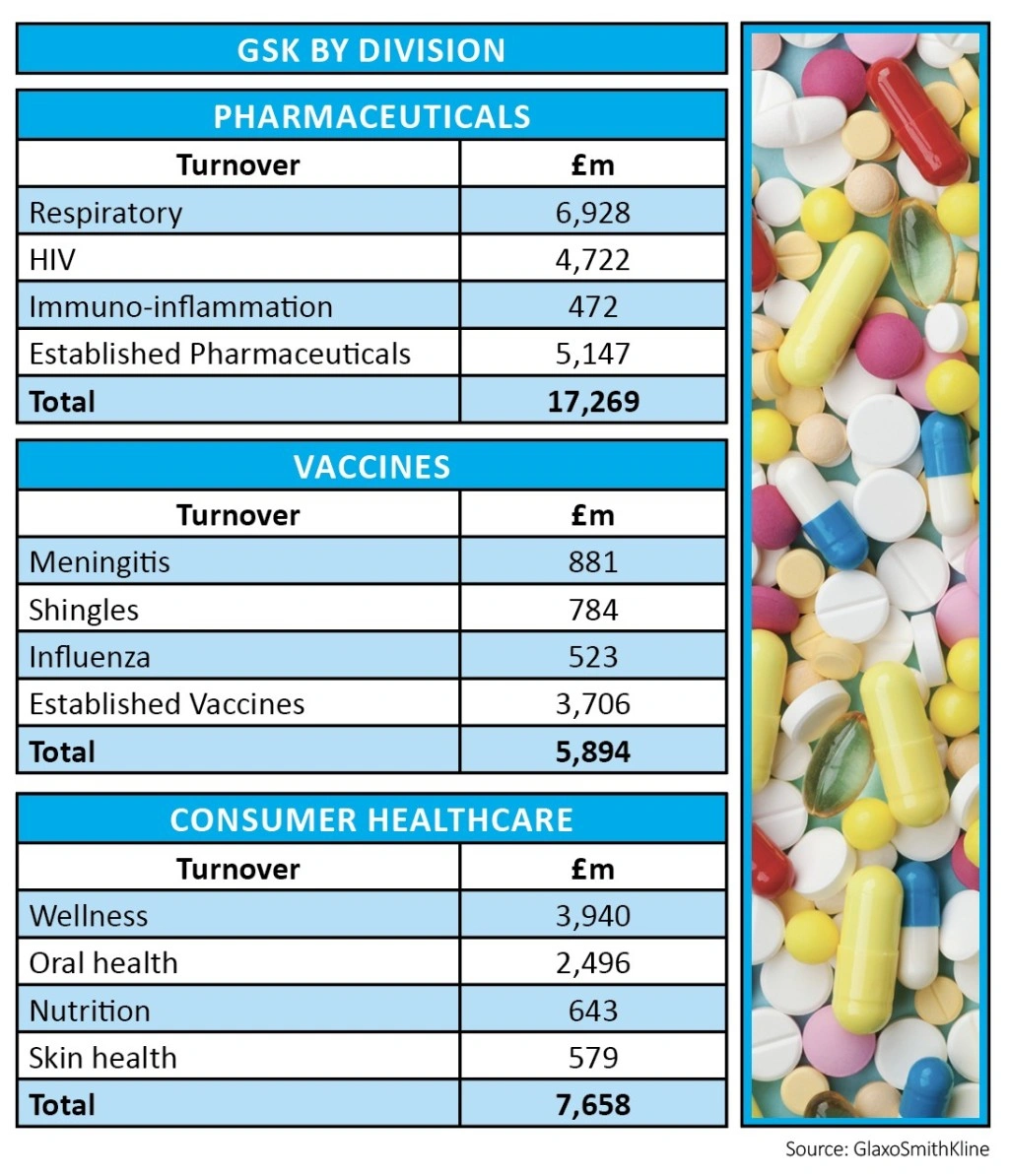

The Pharmaceuticals division generates £17.3bn of revenues split between respiratory products contributing £6.9bn, HIV products contributing £4.7bn and established products including Immuno-inflammation with £5.7bn. The Vaccines division has £5.9bn of sales.

Currently the drug with the largest annual sales is Advair, (£3.1bn) which is used to treat chronic bronchitis but now faces generic competition in the US. Although the company has been reducing the price of the drug to minimise the impact, it expects to lose up to a £800m of Advair revenues this year.

There are three drugs which analysts believe hold the key to GSK’s future.

The company’s shingles vaccine, Shringrix has seen rocketing sales recently, so much so that GSK can’t produce enough of it to meet demand. In 2018 the vaccine notched up sales of £784m, from just £22m in 2017 and ultimately the consensus estimate is for the vaccine to achieve peak annual revenues of £1.5bn to £2bn.

As we mentioned earlier GSK is one of the pioneers in treating HIV and they have a strong franchise in this field. The company is pinning its hopes on a novel two-drug regime (Juluca) for the treatment of HIV, compared with the normal treatment which uses three medicines to suppress the virus. Sales are still under £100m but there are expectations that the drug could reach peak annual sales of £4bn to £5bn.

BETTING ON CANCER DRUGS

GSK has big ambitions to rebuild its oncology division through increased R&D, acquisition and licensing. The $5.2bn acquisition of Tersaro brought a strong pipeline of drugs including ovarian cancer drug Zejula, a rival to AstraZeneca’s (AZN) Lynparza.

Analysts at Jefferies reckon that Zejula will achieve peak annual revenues of $550m.

It made another bold move when it signed a $4.2bn licensing deal with Merck KGaA for a cancer immunotherapy programme. The two companies are planning an ambitious development with eight trials planned before the end of the year.

GSK virtually exited the cancer market when it sold its products to Novartis in 2015, but with the two big oncology deals in 2019 and the separation of consumer healthcare division in 2020, the company has a renewed focus on cancer treatments.

GOOD MANAGEMENT EXECUTION IS KEY

Analysts believe that the strategic rationale for the demerger within the next three years makes a lot of sense. The thinking is that a standalone consumer company will be able to support higher debt levels, given that the established brand portfolio throws-off good cash flows.

This will allow the GSK to effectively de-leverage the remaining pharma and vaccine divisions as the debts will move into the demerged business. Not only will this facilitate further investment in growth, but with good execution, permit the company to maintain the dividend.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.