Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWhich assets perform the best in bear markets

Worries about the possibility of a global economic slowdown appeared to gather pace last week when China posted its slowest growth since 1992.

This adds to existing concerns about a brewing trade war between the US and China, a US stock market seemingly running out of steam, yield curve reversion, economic decline in the EU’s Germany powerhouse, and what a potential Brexit deal might do the UK economy.

IT IS BECOMING INCREASINGLY EASY TO FEAR THE WORST.

The UK stock market has gone pretty much nowhere for three years, there have been corporate collapses and a flood of profit warnings this year, the IPO market seems to dried up entirely, yet many investors still feel hugely exposed to the possibility of a stock market collapse.

When stock markets go south it is hard to hide in equities. Superficially, global equities have performed well in 2019, led by the US market’s 24.6% increase, according to data compiled by Fidelity International. Global stocks are 20.6% ahead this year while even the UK market has put in a 14.4% rally.

Yet these seemingly impressive returns mask a strong rebound following the hefty market correction that echoed across global stock markets a year ago. Precious little in the way of real returns have been earned since.

If this adds to the sense of foreboding and investors find themselves reaching for the tin hats and stockpiling baked beans, it is worth looking at what various assets have done in the past when stock markets have slumped.

Fortunately, there are other asset classes that tend to either hold steady in a downturn or rise when equity markets suffer. While history can’t predict what will happen in the future, several assets have historically performed well in times of crisis, and appear to be leading the pack again.

WHAT DOES WELL IN BEAR MARKETS?

Fixed income has had a bad rap over the last few years, because it barely pays a yield in today’s low interest rate environment. But this is because demand has been high from investors increasingly keen on these risk-off assets. As the price of the underlying bond rises, so the yield falls.

The rally in fixed income bonds is understandable when you look at past bear market performance. In the teeth of the financial crisis bonds were one of the only asset classes not to lose investor’s money. In 2008 government bonds rose more than 53%, corporate bonds rallied close on 27% while emerging market debt also performed strongly, versus the 6.4% return on cash that year.

All other major asset classes went down in 2008, with equities leading the pack.

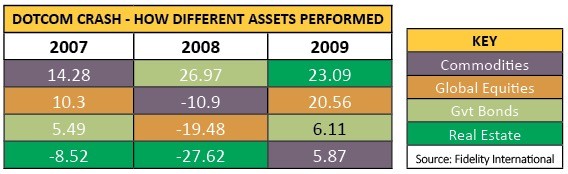

It was a not dissimilar story once the dot.com boom turned ugly in 2000, beginning a three year run for decent bonds returns, interspersed with periodic shows of strength for commodities and real estate.

Between 2000 and 2002 global equities endured three years of declines versus mid-single digit returns from cash.

It’s an instinctive reaction for investors to sell out of stocks and shift into cash when the markets are panicking about stock markets. Shifting to less risky investment options during times of uncertainty has its strategic merits, capping losses if relatively temporary market corrections evolve into more prolonged slumps.

GOING INTO CASH MAY NOT BE THE RIGHT MOVE

But there are important downsides to consider. It is nigh on impossible to know ahead of time how far or for how long a market downturn will last, or even when it will come.

‘Late cycle equity returns can be very strong,’ Michael Bell of JP Morgan Asset Management reminded clients in September.

Just as importantly, it is equally tricky to know when to get back into stocks and often they can often bounce back far quicker and faster than most investors can anticipate, meaning missing out on considerable recovery upside.

Global equities rallied more than 21% in 2003, the year directly following the 2002 nadir for stocks, when they crashed 26.8%.

The pattern was repeated straight after the worst of the financial crisis collapse, when in global equities rallied 20.6% in 2009. UK shares did even better (up 30%), while stock markets across Asia-Pacific and emerging markets soared 50%-plus as investors were swept up in a risk-on rally.

This underscores the advice of many of the world’s best investors over the years - that trying to time the markets is a mugs game.

‘Only liars manage to always be out during bad times and in during good times,’ said US financier Bernard Baruch.

Far better to invest for the long-run and and diversify your portfolio sensibly across equities, funds and asset classes. Focus on high-quality stocks, or funds that do, with strong market positions, that have highly valued products or services with decent pricing power, and with the balance sheet and cash flow strength to withstand temporary slowdowns.

These are the types of company that will be capable of emerging from spells of volatility equipped to take advantage when things stabilise.

Remember, equities have historically beaten all other asset classes in the past, when judged over a reasonable period.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.