Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineLearning the lessons from Woodford woes

Investors have been rocked by the culmination of the woes facing one-time star fund manager Neil Woodford and more importantly those who put their faith in him.

Having seen the flagship equity income fund wound up, Woodford Investment Management has now resigned from LF Woodford Income Focus (BD9X6D5) and Woodford Patient Capital (WPCT) investment trust.

The latter is likely to bring in a new manager, while Income Focus, currently suspended, could be wound up, amalgamated with another fund or also see a different manager appointed.

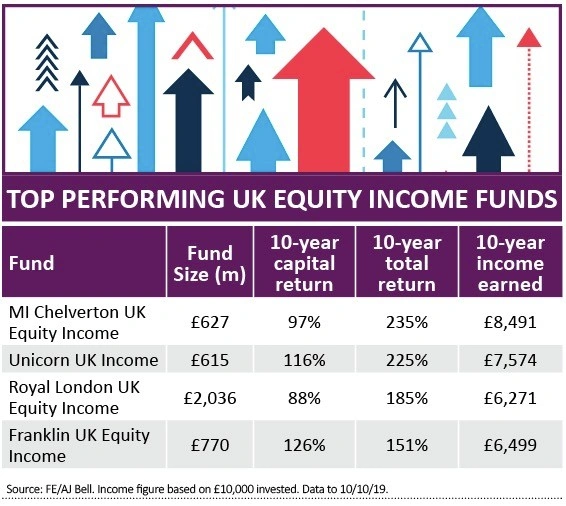

DON’T GIVE UP ON ACTIVE FUNDS

What lessons can be drawn from the sorry episode? The first thing to say is that what happened with Woodford should definitively not put people off from investing in the markets entirely or from using actively managed funds to do so.

However, there should certainly be a move away from the approach pursued by those who effectively entrusted all of their cash to just one or two very popular funds.

Dealing was suspended in LF Woodford Equity Income in early June after an increased level of redemptions. The problem was one of liquidity (or the ability to buy and sell). Woodford had invested in lots of unquoted assets which were then difficult to sell when he needed to hand investors back their cash.

Although Woodford attempted to rejig the portfolio towards more liquid assets the fund’s authorised corporate director, Link Fund Solutions, ran out of patience on 15 October and elected to wind up the fund.

Asset manager BlackRock has been appointed to sell the listed assets from the fund and broker Park Hill will handle the disposal of the illiquid assets with the first batch of money being paid at the end of January 2020.

The amount available for distribution to investors is unknown at the stage as it will depend on how quickly the assets can be sold at a fair price.

LEARNING THE LESSONS

Rather than being attracted by the cult of a star manager, you should look for funds which have a clear and consistent strategy and a track record of success over the long term. It is also worth investing in a portfolio of funds, rather than risking all your cash with just a single collective.

Make sure you understand what the person investing on your behalf is trying to achieve. Performance will always be variable, markets can be volatile and different investment styles can go in and out of fashion but if a fund is pursuing an approach which has proved profitable historically this provides a measure of comfort as an investor.

After all managers can always leave a fund, but if there is a well-defined game plan for their successors to follow there is more chance of long-term performance being maintained.

Woodford moved away from what had made him so successful at his previous employer Invesco Perpetual. Namely buying mainly large cap stocks whose income potential had been undervalued by the market.

One of his big calls was buying big tobacco stocks in the early 1990s when others were fearful aggressive US authorities would drive them out of business. He subsequently benefited from significant capital gains and a steady flow of dividends.

WATCH FOR A SHIFT IN STRATEGY

Since leaving Invesco in 2013 and setting up his own asset manager Woodford Investment Management, Woodford increasingly pursued a different more growth-focused approach which involved picking smaller and in some cases unquoted businesses. By early 2019 nearly 20% of the Equity Income fund was in companies which were not listed on a recognised stock market.

In hindsight the decision by the Investment Association to kick the fund out of its equity income sector for failing to meet yield requirements in March 2018 should have set alarm bells ringing.

The Woodford case also highlights the need to investigate the corporate governance and culture of the asset manager behind a fund.

With Woodford it appears there were a lack of checks and balances to prevent him from pursuing a strategy of investing unquoted assets, when the structure of open-ended funds always made this a big risk.

Just as many open-ended property funds found in the wake of the Brexit vote, if investors are selling or redeeming their holdings then assets need to be sold to pay these investors. But providing daily liquidity in this way is at odds with investing in assets which you cannot be bought or sold at the click of a button.

REGULATORY CHANGE

This brings us on to a conversation about the role regulation can play. The Financial Conduct Authority is bringing in new rules on liquidity, forcing certain funds to come up with detailed contingency plans for liquidity issues and to be clearer in explaining liquidity risks to investors.

It has proposed other changes, including different redemption conditions for large institutional investors. Relevant in the Woodford case because Kent County Council’s withdrawal from the Equity Income fund was effectively the straw which broke the camel’s back and led to the suspension.

The chief executive of investment trust industry body the Association of Investment Companies, Ian Sayers, says there should be a move towards ‘reliable redemption’. In practice this might would mean that as he observes, ‘funds with liquid portfolios could still offer daily redemption of an investor’s entire holding.

‘At the other end of the spectrum, for a fund invested in the most illiquid assets, the ability to redeem the entire holding might have to be subject to, say, a year’s notice.’

He adds: ‘I was very concerned to read that the FCA does not consider that how often funds suspend is a measure of success or failure. I doubt many investors in Woodford Equity Income Fund would agree.

‘This "normalisation" of suspension is perhaps the most worrying trend in recent months and perhaps reflects the fact that, under the FCA’s new rules, suspensions are likely to become more frequent, not less.’

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.