Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineIs Halfords a bargain or a value trap?

Specialist retailer Halfords (HFD) may be the market leader in various parts of the motoring and cycling sectors, but the company’s protracted struggles are reflected in a rock-bottom equity valuation.

Once the go-to place for car parts and bikes, Halfords is recovering from a failed strategy between 2008 and 2012 driven by cost cuts, low capital expenditure and share buybacks, with poor stock availability, staffing and service levels areas that needed to be addressed.

Current swirling headwinds include frail consumer confidence with weak spending on discretionary ‘big ticket’ items, not to mention weak sterling.

Building on some heavy investment over the past five years, there are positive early signs emanating from relatively new CEO Graham Stapleton’s strategy to ‘inspire and support a lifetime of motoring and cycling’.

Essentially, Halfords is becoming a service-led business, leveraging its brick and mortar store presence as an advantage over cheaper online competitors whilst tying its retail and autocentres businesses more closely together.

HOW DOES HALFORDS EARN MONEY?

Redditch-headquartered Halfords sells automotive, cycling and leisure products spanning engine fluids and car batteries and Dash Cams to bikes, cycle clothing and camping furniture.

At the last count, the retailer operated from 450 Halfords stores, 26 Performance Cycling stores trading as Cycle Republic, Tredz, Boardman and Giant, as well as 318 Halfords Autocentres garages.

Roughly two thirds of its sales come from motoring-related products and services with a third generated by cycling. Stapleton has outlined his strategy to compete in the fast-evolving retail market, one characterised by increasing competitive threats and a more demanding customer.

HOW IS HALFORDS ADAPTING?

Both the motoring and cycling markets have good long-term growth prospects, but generalists have parked their tanks on Halfords’ metaphorical lawn.

In response, Stapleton has chosen to accelerate investment in the business to become a much more differentiated ‘super specialist’ with a unique and more convenient services offer, able to lead in its core motoring and cycling markets whilst retaining customers for a lifetime.

Interestingly, the dynamics of Halfords’ markets are changing; cars are becoming more complex – think of the shift towards electric vehicles – meaning fewer people have the capacity to work on their cars themselves even for minor issues, and Halfords is also seeing a massive surge in the popularity of E-Bikes.

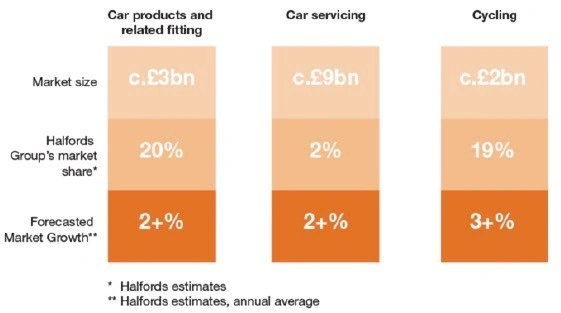

It is also worth noting that Halfords’ car servicing market share remains small at just 2%. That suggests scope for growth going forwards in a fragmented industry flush with less financially muscular independent operators. Stapleton’s strategy also has a greater emphasis on cost and efficiency and the retailer is refreshing its stores in order to make them fit for the future.

A CYCLE OF DOWNGRADES

Unfortunately, as broker Peel Hunt recently pointed out, Halfords has downgraded expectations ‘almost every time that it has spoken to the market in the last 18 months’.

Besides fragile consumer confidence and subdued spending, especially for discretionary big ticket purchases such as bikes and car technology products, Halfords’ faces margin headwinds from rising wages and sterling weakness versus the US dollar.

Bears will point out that Halfords is a particularly weather-sensitive retailer. Mild autumn and winter weather is unhelpful for car maintenance and car enhancements products, while summer downpours dampen cycling sales growth.

Analysts at Berenberg believe weakness in cycling is both structural as well as cyclical and have also argued the roll-out of Cycle Republic stores might cannibalise the current store estate.

EARNINGS STUCK IN REVERSE

In its latest trading update (4 Sep), the car parts-to-bicycles purveyor reported weaker than expected first half sales growth and downgraded full year profit guidance.

During the 20 weeks to 16 August, sales were constrained by cooler, wetter summer weather and weaker consumer confidence, with like-for-like sales declining in both the motoring and cycling categories.

Encouragingly however, electric bike sales continued to grow strongly, Halfords’ ‘3Bs’ – bulbs, blades and batteries – returned to growth and online sales ticked 8.4% higher with a very healthy 85% of Halfords.com orders collected in store.

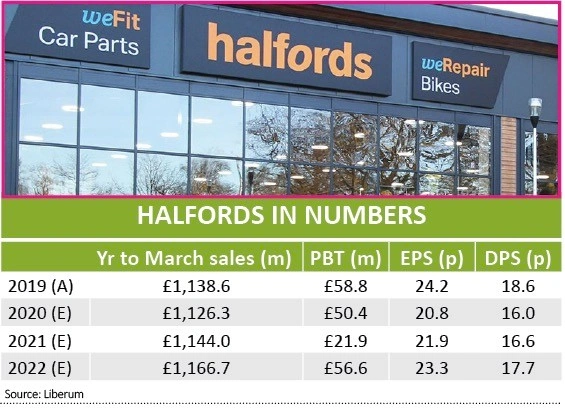

Focusing on improving gross margins and keeping a lid on costs, Halfords warned that subdued sales trends twinned with spending to stimulate growth would mean underlying pre-tax profit for the year to March 2020 weighing in ‘within the range of £50m to £55m’, a downgrade to estimates.

Peel Hunt recently downgraded its price target from 200p to 150p, arguing Halfords needs to ‘fundamentally rethink the way that it comes to market’.

Sellers of the stock, well-followed analysts John Stevenson and Jonathan Pritchard think Halfords is over-distributing given its gearing levels and believe ‘a cut of the dividend and a major strategic rethink are required here and without that the shares are only for the brave’.

Essentially, while Halfords’ high dividend yield looks is visually attractive, the payout could eventually prove unsustainable if sales remain subdued and profits decline further.

The shares have deep value appeal following a dire run and there are some promising early signs from Stapleton’s strategy, although further downgrades or even a dividend cut could be coming down the track. Given the risks, Halfords is one to watch for now.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.