Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineHigher quality of earnings failing to support FTSE 100

Last week’s column looked at the quantity of FTSE 100 revenue, profit and dividends and drew comfort from how all three were expected to reach record levels in 2020, according to analysts’ consensus forecasts. Better still, those forecasts did not seem unduly aggressive, with the sales expected to rise by just 2%, pre-tax profit by 8% and dividends by 3% next year.

This week, our attention will turn to the quality of UK plc’s earnings. After spectacular collapses at Carillion, Patisserie Valerie and (former FTSE 100 member) Thomas Cook in the past two years, investors are more aware than ever of the importance of checking not just the quality of earnings but those profits’ provenance, how efficiently they are turned into cashflow and the support they provide to a company’s balance sheet.

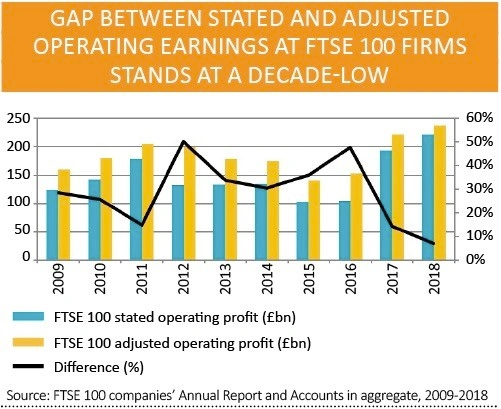

And one test that diligent investors can apply here is to look at the gap between statutory earnings and companies’ preferred profit metrics which can – cynically – be described as ‘earnings before bad stuff, or ‘EBBS’.

The good news is that the gap closed again in 2018 for the second decline in a row, when using operating profit as the main performance metric. The gap of just 7% is the lowest this decade.

The less good news is that the gap between stated and adjusted net income has opened up again – and that is despite some £8bn in capital gains on disposals (mainly from Whitbread (WTB), Unilever (ULVR) and Rio Tinto (RIO)) that flatter stated earnings. Whip those out and the net income ‘quality gap’ at the other 97 FTSE 100 firms rises to 32% from 22%.

For this column, operating profit is the real pumping, beating heart of a firm, so it is possible to draw encouragement from the closing of the ‘quality’ gap, even if it is not doing the FTSE 100 a huge amount of good. The index still trades some 10% below May 2018’s all-time high.

QUALITY STREET

It would be nice to think that the improved quality of operating earnings will come through in cash flow – and since it is cash flow that funds dividend payments this closure of the gap between statutory and adjusted operating profit could help to reaffirm the UK equity market’s credentials for yield-seekers.

However, it has to be admitted that there are three possible interpretations for the apparent improvement in earnings quality. The first is that companies are simply being more transparent, providing greater clarity to shareholders on the many moving parts which make up their business and enabling investors to get a better view of what is really going on under the bonnet.

The second is that companies are getting to the bottom of their bag of accounting tricks. If that is really the case, we may start to see a number of chief financial officers decide to look for pastures new or companies start to make more (big) acquisitions, as such deals can create fresh leeway for earnings adjustments as the target is integrated. It will be worth watching out for any trend here in the next 12 to 18 months.

The third that companies feel a lesser need to embellish their numbers as underlying trading improves. This seems unlikely, given the general belief that the global economy is slowing down, but it cannot be entirely dismissed.

ASSET ASSESSMENT

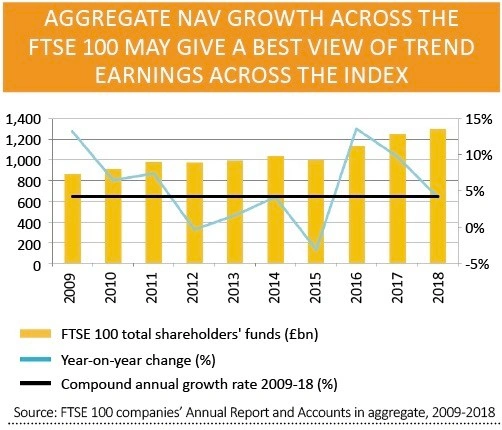

Over the long term, a company’s net asset value (NAV, or shareholders’ funds or shareholders’ equity) should rise broadly in line with profits. The share price should rise broadly in line with both, allowing for swings and roundabouts relating to where we happen to be in the economic cycle.

It is therefore interesting to note that NAV in aggregate across the FTSE 100 rose by 4% in 2018 – exactly in line with the ten-year compound annual growth rate (CAGR) shown in that metric since 2009.

That seems to make perfect sense. GDP growth plus a little inflation and maybe some productivity gains could well come to trend profit growth of around 4% in the post-financial-crisis world. And most investors might be quite happy to get a 4% capital gain a year, with a dividend popped in on top, in a world where yields on cash on bonds are not much better than zero.

So if finance directors and CEO are playing about with their numbers for any reason (to trigger bonuses or stock options or simply avoid the sack) over time the effect still washes out, at least according to the ultimate arbiter, which is NAV.

It is this figure, plus the gap between stated and adjusted earnings that investors need to watch. Firms where the difference has been consistently large include Marks & Spencer (MKS), Royal Mail (RMG) and Imperial Brands (IMB). All have performed badly and the first two have been relegated from the index.

Companies where the gap has begun to grow, albeit from low levels include Reckitt Benckiser (RB.), DCC (DCC), TUI (TUI), Sainsbury (SBRY), DS Smith (SMDS) and Bunzl (BNZL), so it will be interesting to see how the trend develops here in 2019 and beyond.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.