Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineHow to invest your PPI windfall

The deadline for payment protection insurance (PPI) claims may have just passed but judging by the new provisions revealed by the high street banks many of us waited until near the August deadline before applying for compensation.

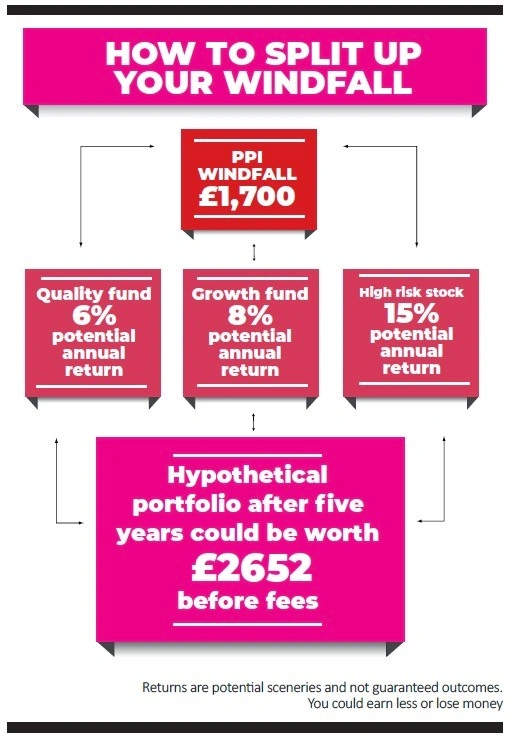

With the average compensation payment standing at £1,700 according to the Financial Conduct Authority, and sometimes running to several multiples of this figure, a PPI payout can represent a healthy windfall.

Not all of us were affected by PPI but perhaps you have had an unexpected gain from elsewhere, maybe a small inheritance or a premium bond prize.

In any of these circumstances, you might use this money to pay off a credit card or bolster your savings, but another option if your finances are otherwise healthy is to put the cash to work in the markets. We’ll now give you some suggestions for how to put your money to work.

WHERE TO INVEST?

Let’s assume you got bang on the average payout of £1,700, how might you invest this cash?

Shares has identified three potential avenues and you could vary your allocation based on your appetite for risk.

As a base case you could take £900 and put it in a fund with a quality bias which would be an appropriate core holding for the long-term.

If you already have some investments you may want to buy more of the favourite fund in your portfolio. Alternatively if you’re looking for ideas we suggest you look at Finsbury Growth & Income (FGT) and Liontrust Special Situations (B87GRQ1).

The remainder of your PPI windfall could be used to target higher risk but potentially higher reward investments.

You might want to think about splitting the remaining £800 equally between a growth-orientated fund and a stock which has the potential for significant upside via a turnaround effort or corporate shake-up. We have ideas for both later in this article.

HOW MUCH COULD YOU MAKE?

The returns you can achieve from investing are inherently unpredictable and you have to be prepared for things to go wrong.

However, let’s assume your approach broadly works out in order to make some assumptions about the kind of returns you could expect from our three-pronged PPI compensation portfolio.

It is important to have realistic expectations. A quality fund like Fundsmith Equity (B41YBW7), for example, has delivered annualised returns of 18.8% since inception but we don’t expect such levels of return from the brodader market in the near term.

Let’s assume the market gets a bit more difficult and your quality fund achieves 6% a year, more in line with historic averages from investing in equities.

As compensation for the greater risk, we’ll assume your growth-orientated fund achieves 8% a year. And finally we hope the individual stock delivers 15% — although it is important to stress this could easily lose you money if there are new setbacks to its business.

After five years, before any fees, you would be sitting on a portfolio worth £2,652, close to £1,000 more than your starting position under our assumed returns. There is no guarantee you will make such money, we’re simply trying to give you an idea of what might be possible.

RISKS VS REWARDS

Investors always face a balancing act between risk and reward. Someone wanting a high return might look at higher risk assets. Someone only wanting to invest in lower risk assets must be prepared to have lower returns.

To put that into some context, assets with lower risks include cash and developed market government bonds. Stocks are considered to be higher risk assets.

But even within the stock (or ‘equities’) space, different types of companies and sectors have different types of risks and so the returns are variable. For example, utilities enjoy fairly predictable returns whereas biotechnology stocks have unpredictable outcomes and so could see their share prices soar or collapse based on the results of a single drug trial.

THE QUALITY FUNDS

We suggest you look for a fund with a clear and easy-to-understand investment process and a good track record. The bulk of your returns are likely to be generated through capital gains with only a nominal amount coming from dividends.

Finsbury Growth & Income Trust (FGT) 876p BUY

Investors looking for a quality fund run by a very experienced manager should put their money to work with Finsbury Growth & Income Trust (FGT).

The investment trust follows the same style adopted by other funds run by asset manager Lindsell Train, namely a concentrated portfolio focused on high quality stocks that generate large amounts of cash, pay a growing stream of dividends and have the capability to adapt to changing market conditions.

Investee companies tend to be ones which are able to reinvest spare cash back into their business to make them more competitive such as London Stock Exchange (LSE). Other names in the portfolio include investment platform provider Hargreaves Lansdown (HL.).

The original version of this article featured Lindsell Train Investment Trust (LTI) instead of Finsbury Growth & Income. Apologies, we made an error and misread its share price which was £1,402 rather than £14.02 as we originally wrote.

We still rate Lindsell Train Investment Trust as a good one to own but the share price error means it no longer works in our calculation for how to invest £900 from a £1,700 PPI payout. That £900 wouldn’t even buy you a single share.

Finsbury Growth & Income is run by the same people, has a similar style and its lower share price means you could buy many shares with your £900 allocation.

Liontrust Special Situations (B87GRQ1) 419.36p BUY

A perfect buy and forget option, Liontrust Special Situations (B87GRQ1) is run by Anthony Cross and Julian Fosh, who are both AAA-rated by financial information company Citywire.

Over 10 years, it has delivered a total return of 300%, a performance bettered only by three other funds out of the 178 available in its category.

Investing predominantly in UK stocks, the fund aims to identify high quality businesses with strong growth characteristics, taking advantage of areas outside of the largest companies. It is concentrated in nature, holding anywhere between 40 and 60 stocks.

The managers look for firms which have a durable, competitive edge so they can sustain profits for an extended period of time – which they believe translates to strong share price growth.

THE GROWTH FUNDS

Many growth funds invest in smaller companies which have greater capacity to expand than larger businesses. You should expect nearly all your returns to come from capital gains than dividends. Investing in this category of fund involves taking on more risk in the hope of achieving more substantial returns.

Invesco Perpetual UK Smaller Companies (IPU) 522p BUY

By putting your money to work with this trust you benefit not just from the fact smaller businesses have more capacity for growth than their larger more mature counterparts but also a management team which have bags of experience investing in smaller businesses. Co-managers Jonathan Brown and Robin West are a genuine duo, teaming up for site visits and company meetings.

Unlike most small cap funds, this investment trust offers capital growth and income, yielding 3.6% and paying dividends quarterly.

While the trust has the word ‘smaller’ in its name, its portfolio does include several stocks with market caps of more than £1bn.

Brown and West look for businesses with a track record rather than start-ups. They are focused on businesses with self-help potential, a successful roll-out strategy and exposure to secular growth trends. Names in the portfolio include defence firm Ultra Electronics (ULE) and vets outfit CVS (CVSG:AIM).

Merian Global Equity (B1XG7h7) 400.0p BUY

Formerly called Old Mutual Global Equity, over the past decade Merian Global Equity (B1XG97H7) has been second only to Fundsmith Equity in terms of performance with a 292% total return.

Admittedly it didn’t have the best of years in 2018, and to an extent this year as well with performance decent but still slightly below its benchmark. However, its long-term track record is reassuring.

Where it has excelled in the past and – given the way the nature of investing is heading – where it could easily excel in future, is through the systematic way it deploys investors’ money.

The fund’s main manager, Ian Heslop, has effectively built his name in the investment world by developing algorithms to help him and his team find the best opportunities, the idea being that it avoids the biases fund managers may intrinsically have.

HIGHER-RISK STOCKS

Many investors like to look for companies whose share prices have been hit by specific issues in the hope these can be resolved and the shares bounce back. Scenarios might include temporary financial pressures caused by the loss of a contract, regulatory threats, a market slowdown or margins being squeezed by cost inflation.

Buying these stocks means having faith in the management being able to resolve problems quickly otherwise you could see the value of your investment fall before any chance of rebounding. These should be treated as high-risk situations and you should not invest any money you might otherwise need.

One could argue that PPI compensation is essentially free money so it doesn’t matter if your investment goes wrong. However, that doesn’t mean you should make reckless stock decisions. You should still undertake the same level of thorough research you make with all other investments and fully understand what could go wrong if you bought the shares.

XP Power (XPP) £24.4O BUY

The power switching equipment engineer is seeing demand recover. This follows a lacklustre first half linked to slowing sales into the stock-piled semiconductor industry.

A recent third quarter trading update showed improving order flow and a book-to-bill ratio of 1.04-times after dipping below one previously. This implies that future sales contracts are once again running ahead of current orders, a sign of growth.

XP Power’s real attraction is its engineering excellence and it typically works with customers on long-term power system projects that require custom output voltage combinations, unique control or status signals and specific mechanical packaging for optimal performance and integration.

It has a strong balance sheet, an outstanding operating track record and attractive, growing dividends. The risks come from an acceleration of the slowdown in the global economy, and the demand bounce from semiconductors industry could take longer than hoped.

Xaar (XAR) 49.3p BUY

The Cambridge-based inkjet printhead technology designer will be hoping new chief executive Stuart Mills can bring much needed stability after two years of hell. End markets have dried up as capital budgets of customers shrank leaving legacy equipment sales in the lurch while new kit has failed to fill the gap. That’s led to profit margins being battered and multiple profit warnings, the most recent just last month, when Xaar said it would have to write down the value of its assets and delayed the date of its first half results. This makes the share price chart resemble a ski resort black run, smashing the company’s market value from about £350m to just a tenth of that today. But Xaar has been a market leader in its field for years and we believe there is some very good underlying technology.It is vulnerable to a takeover particularly while the pound is so depressed.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Big News

- Woodford Equity Income wind-up shakes fund industry to its core

- Could debt concerns at rival help Domino's Pizza?

- Shareholder dissent remains muted

- First glimpse at how stocks could react to positive Brexit deal

- TUI and Jet2-owner Dart capitalise on Thomas Cook ‘game-changer’

- UK dividend growth under threat