Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWhat the sharp move out of momentum into value means for your portfolio

On a normal, relatively quiet Monday afternoon on 9 September, some shares experienced a sharp move with no associated corporate news flow attached. As it later turned out, the same thing was happening to stocks with similar characteristics across global stock markets. Momentum was suddenly out of favour and investors rapidly switched to value trades.

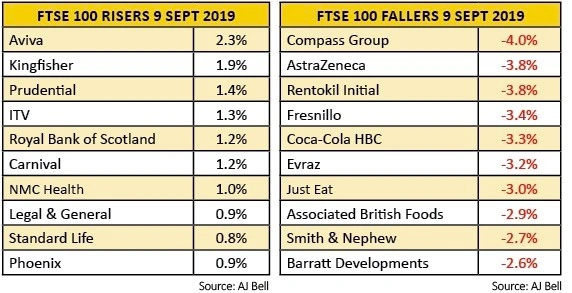

Below is a snapshot of the biggest risers and fallers from that afternoon. All of the losers have outperformed the market over the last year, while all of the gainers have underperformed. Before the rotation, one set was ‘loved’ and trading on high earnings multiples, while the other was ‘hated’ and trading on low multiples.

On closer inspection the winners/losers have something in common, from a quantitative perspective, at least.

Shares in international catering firm Compass Group (CPG), which set an all-time high as recently as 4 September of £21.49, have been in demand because of the relatively high predictability of the company’s earnings and low volatility of its shares.

On the other side of the table is home improvements company Kingfisher (KGF), one of the poorest performers over the last year; in fact, its shares registered a new eight-year low in August of 186.7p. This type of business has been shunned by investors because of the unpredictability of its earnings and its cyclicality and low quality.

In times of economic uncertainty, as well as political turmoil, investors tend to favour companies that offer more visible, predictable earnings, partly because their share prices tend to be less volatile. For the same reasons investors tend to have a low appetite for companies whose earnings are less predictable and can be hurt by a sluggish economy.

QUANT INFLUENCES

One factor that explains the reversal of fortunes for the two companies on that Monday afternoon was the actions of a group of investors who call themselves ‘quants’. In total over $1trn of assets are managed using quantitative techniques, double the level just nine years ago.

Some of the biggest quant firms in the world like Renaissance Technologies don’t hire finance professionals but instead look to take on talented graduates with advanced degrees in data science and statistics.

Their role is to find hidden patterns in the movement of stock and commodity prices by applying complex statistical techniques, in order to exploit price anomalies.

One of the most successful quant strategies historically has been the momentum factor. This simply states that stocks tend to maintain their recent price trends into the future. Winning stocks continue to be winning stocks and vice-versa. At least, that is, until they don’t.

Rather like stretching an elastic band to the point where it snaps back, the huge outperformance of quality stocks and underperformance of value reached a tipping point, and ‘snapped’ back hard.

POOR BREADTH

Breadth measures the number of rising stocks compared to falling stocks and a healthy market normally has lots of companies participating in the rising trend and the winning/losing stocks rotate.

What has been unusual about the market since the financial crisis is that the rising market has been driven by relatively few shares, underlining the risk-averse stance taken by investors. Quality and momentum has been the only game in town for many years.

The underperformance of value has been so stark that some people had begun to utter what famed investor John Templeton described as the most dangerous words in the world of investing, ‘this time it’s different’.

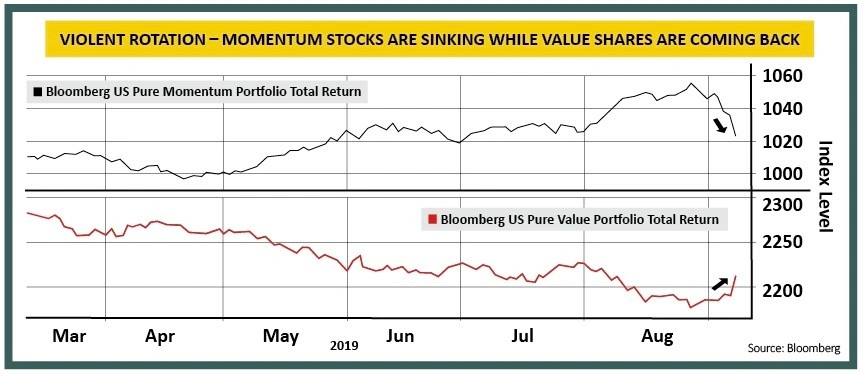

Then Monday happened and remarkably, months of outperformance were wiped out in just two days.

The speed of the snap back caught the markets by surprise. According to investment bank JP Morgan, value stocks saw one of their biggest single-day rallies ever, relative to momentum stocks and represented a ‘five standard deviation event’.

Standard deviation simply measures how far the most extreme points are from the average. Five standard deviations are so rare an event that in theory they only happen every 30 years.

And this wasn’t just a UK phenomenon, it happened across other stock markets too. The quant team at investment bank Nomura described the ‘momentum shock’ in the US market as the second largest drawdown in history, going back to 1984.

SHORT INTEREST

The biggest winners on 9 September also had something else in common; some of them were heavily ‘shorted’. Fund managers short stocks that they believe will fall in price because the business is in trouble or will continue to underperform. They profit from any reduction in value of the stock.

Kingfisher is one of the most heavily shorted stocks in the UK, with around 5% of its shares held short according to shorttracker.com. It’s likely that some of the move in Kingfisher was related to investors closing their short positions in order to control risk.

IF THE UNWIND CONTINUES, WHICH STOCKS ARE MOST AT RISK?

We have created a screen to find the stocks most at risk to further mean reversion as well as some value stocks which might benefit if the rally continues.

We screened for those stocks within the FTSE 350 which ranked high on momentum and quality, while also ranking poorly on value. This group of shares lost 2.3% on average over the week.

We also screened for those stocks with the opposite characteristics, scoring high on value and low in momentum and quality. This group of shares rose by 4.7% on average.

Interestingly, there are three names out of 15 on the high momentum list that have, so far at least, held up relatively well.

Electric equipment maker Halma (HLMA), oil and gas engineering specialist Rotork (RTRK) and promotional products specialist 4imprint (FOUR) have not succumbed to the momentum tantrum.

While these names have some characteristics of high quality shares, they may eventually be at risk of short term selling if the reversal from momentum continues.

On the ‘poor value’ list every single share posted a positive return over the week, with Charter Court Financial Services (CCFS) and Centrica (CNA) the standout performers, up 14.2% and 8.2% respectively.

DOES IT HAVE FURTHER TO RUN?

The consensus view seems to be that investors will continue to abandon investing in more risky, cyclical businesses like banks and airlines while the economic backdrop is not supportive and inflation remains subdued.

In a low growth world, where over $15trn of bonds yield negative interest rates, buying growth and quality at any price may seem more sensible than buying cyclical businesses at a seemingly low price.

It would seem that more sustainable economic growth and higher interest rates are required to tempt investors away from so called predictable growth companies.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.