Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineTaking advantage of an emerging markets opportunity

Emerging markets (EM) investing is far from risk-free, yet investors who shun this exciting asset class are missing out on some of the fastest growing opportunities in the globe today.

Indeed, EM countries are becoming the long-term winners in the current economic climate, a volatile backdrop that includes Brexit, trade wars and the early signs of global economic slowdown.

So posits a new study – The Changing Nature of Emerging Markets – by the Franklin Templeton-managed Templeton Emerging Markets Investment Trust (TEM).

Thirty years ago, emerging markets were a mixed collection of commodity exporters and low-cost manufacturers. Yet today, they play an increasingly important role in driving global growth.

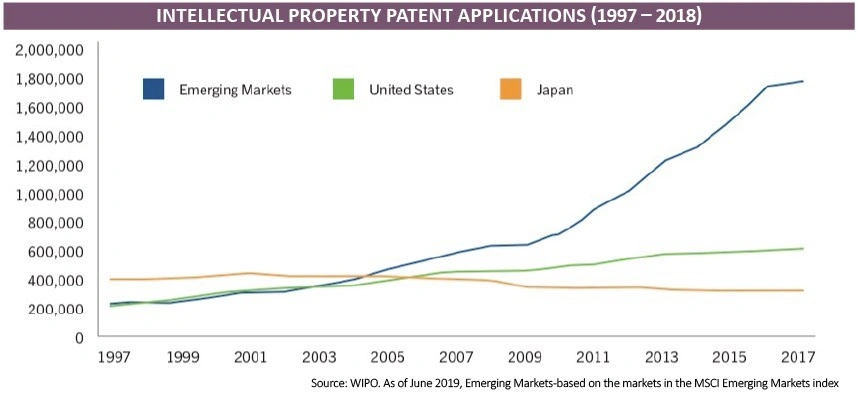

As TEMIT’s study highlights, the technological transformation and relative economic and political stability has driven a sharp rise in the proportion of high value-add exports coming from emerging markets, which are also playing a crucial role in renewable energy generation too.

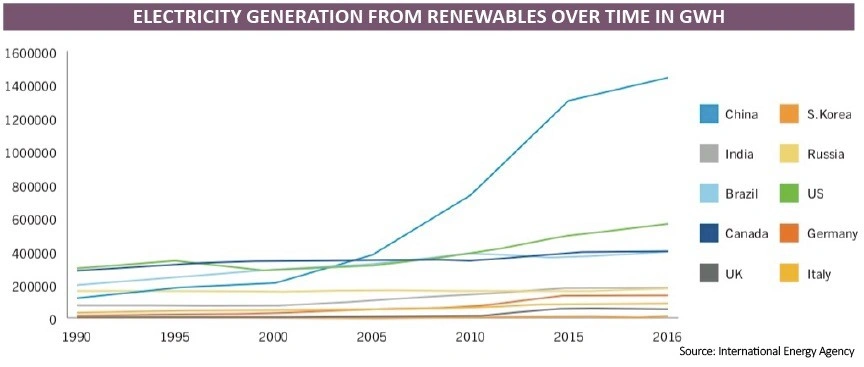

China produces more than 2.5 times the amount of renewable power that the US produces, while Brazil, India and Russia are all generating far higher levels of renewable electricity than the UK, Germany and Italy.

Chetan Seghal, TEMIT’s lead portfolio manager, explains: ‘Since we first began investing in emerging markets, the nature of these economies has changed dramatically. Yet unfortunately, first impressions tend to last, and some investors still associate emerging markets with the “stack it high, sell it cheap” models of the past.’

TEMIT’s research shows that UK consumers are far more exposed to high-tech and value-add products and services coming out of emerging markets than they realise. ‘It is encouraging to see recognition of this change beginning to take shape, particularly among younger consumers, with 50% of 18 to 39-year olds noting that they are increasingly interacting with emerging markets goods and services on a daily basis.’

DIFFERENT FUNDS

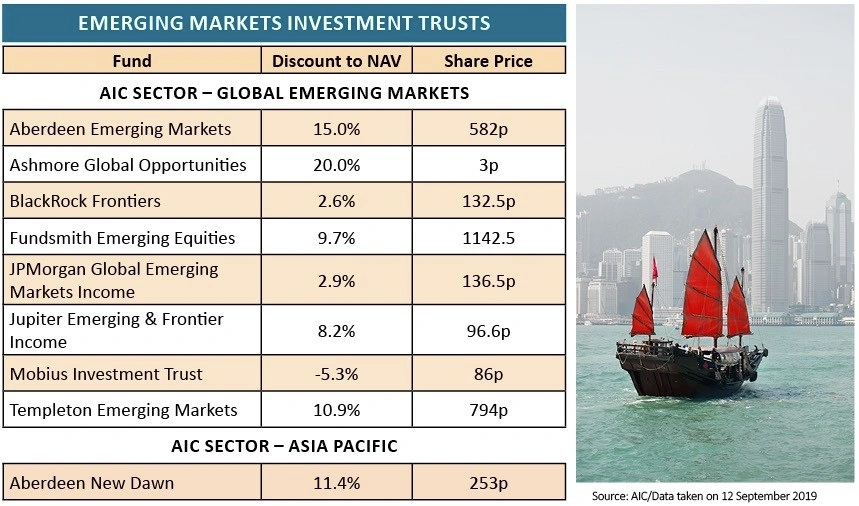

Investors seeking exposure to the asset class are well served by the Association of Investment Companies’ (AIC) Global Emerging Markets sector, trading at an average discount of 9.3% to net asset value.

The sector is home to trusts including Aberdeen Emerging Markets (AEMC) on a 15% discount, Ashmore Global Opportunities (AGOL) on an even wider 20% discount, the aforementioned Templeton Emerging Markets on a 10.9% discount and the Terry Smith-steered Fundsmith Emerging Equities (FEET) on a 9.7% discount to NAV.

Investors seeking a smoother ride could look to JPMorgan Global Emerging Markets Income (JEMI) which trades on a more modest 2.9% NAV discount. The trust is the sector’s best one-year performer in share price total return terms and generates a dividend income plus the potential for long-term capital growth from a diversified portfolio of income-yielding companies – for further illumination, see this week’s Great Ideas section.

DARING TO BE DIFFERENT

A relatively recent addition to the fold is Mobius Investment Trust (MMIT), launched in October 2018 and managed by eponymous emerging markets investing legend Mark Mobius alongside Carlos Hardenberg and Grzegorz Konieczny.

Seeking to deliver long-term absolute returns from emerging and frontier market equities, Mobius Investment Trust aims to put money to work with undervalued small companies with resilient business models.

Mobius Investment Trust has a two pillar approach to investing. The first is to buy companies at a discount to intrinsic value and the second pillar is to catalyse a re-rating through active engagement with its investee companies, dubbed ‘projects’ by the team.

Highly concentrated, with just 23 holdings across 10 countries as at 31 July – China (16.2%), India (15.1%), Brazil (13.4%) and South Korea (11.7%) being the largest country allocations, the trust has a high active share of 99.6% against the MSCI EM Index and 99.4% versus the MSCI EM Mid Cap Index.

‘We are looking at the long term and avoid being distracted by a lot of the short term noise,’ Hardenberg informs Shares. ‘Most of this noise is coming from the western nations and all of these things cause people to be very cautious.

‘The US dollar is the most favoured trade and emerging market currencies reflect a lot of pessimism, and almost capitulation.’ Hardenberg believes the only answer is to understand companies and what they will do over the next 10 years.

The Mobius investing team are obsessed by details on the stock level. ‘We try to understand the story, the people behind the business and the alignment of management interests. And we have very high active share, which means the fund looks very different and there is very low correlation between us and the index.’

Prospective investors are buying into the fortunes of the likes of Yum China, the operator of Pizza Hut, KFC and Taco Bell restaurants across the Middle Kingdom, not to mention Brazilian retailer Lojas Americanas and Indian IT firm Persistent Systems.

OTHER RELEVANT TRUSTS

Away from the Global Emerging Markets sector, investors can access country specialists or the likes of Aberdeen New Dawn (ABD), a denizen of the AIC Asia Pacific sector offering a play on Asia’s compelling structural growth.

Trading on an 11.4% discount despite its NAV growth, this capital growth-focused trust celebrated its 30 year anniversary in May 2019.

Since inception, Aberdeen New Dawn has returned roughly 1,840%, significantly outperforming its benchmark, with £1,000 invested at launch mushrooming into £19,400 today.

‘We’re long-term buy-and-hold investors,’ explains investment manager James Thom. ‘And our process is to find the highest-quality companies in Asia, build a portfolio from the bottom up and not overpay for those quality companies and then hold them for the long term.’

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.