Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineSirius Minerals’ shareholders need to make a big decision

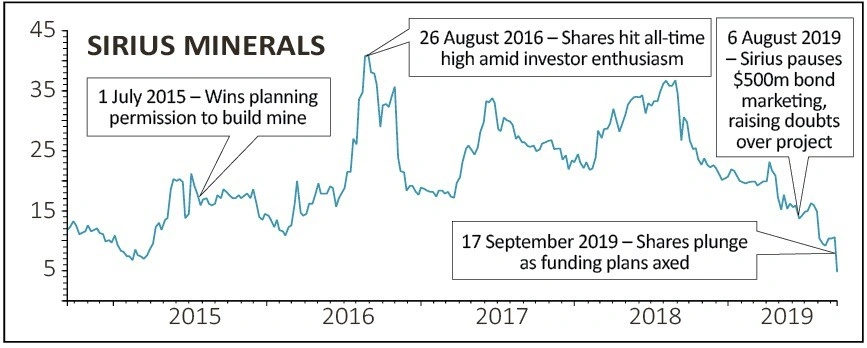

Potash miner Sirius Minerals (SXX) has stunned the market after being forced to cancel plans to raise $500m through a bond sale, meaning there is now great uncertainty over the future of its polyhalite mine in North Yorkshire. Its shares halved on the news (17 Sep) to 4.92p.

A stock popular with many retail investors, Sirius Minerals was meant to be a poster boy for UK mining and engineering with myriad economic benefits.

We will now explain exactly what’s happened, what’s next, and what it means for shareholders.

WHAT’S HAPPENED?

Sirius has scrapped a bond issue, money which was crucial to getting another $2.5bn via a revolving credit facility (RCF) from investment bank JP Morgan, and in turn that funding was vital to get the mine up and running.

According to Sirius, feedback from potential bond investors was that the money could be raised if warrants were attached to the bond.

A warrant is basically an extra sweetener to entice investors. They would normally be able to buy shares in the issuing company at a fixed price until a specific expiration date.

Going down this path would have raised the effective yield for Sirius’ bond above 15%, breaking an earlier condition set by JP Morgan. The bank subsequently declined Sirius’ request for a waiver of this condition.

Sirius now intends to terminate the RCF agreement with JP Morgan.

WHY HAVE THE SHARES FALLEN SO MUCH?

Having pulled the bond issuance, where Sirius goes from here is undecided. But what is certain is that $3bn that was meant to continue funding the project is now gone, at least for the time being.

Sirius has therefore had to slow down operations at the mine in order to preserve some of its remaining cash.

Getting the cash, in the eyes of some in the market, was meant to be a sure thing by now. So the fact it admits it won’t get the money and currently has no idea how additional funds will be obtained has been a shock to investors, triggering widespread selling.

Certainly JP Morgan hasn’t been helpful, and Sirius painted the picture in its statement that the bank almost straitjacketed the firm, only allowing Sirius to borrow money if the bond was broadly distributed (instead of concentrated on a few big investors) and didn’t have a yield over 15%, evidently difficult for Sirius in the current environment.

Shore Capital analyst Yuen Low highlights that for all its positive noises, ‘when push came to shove’ support from the UK Government was nowhere to be seen.

When it paused the bond offering in August, Sirius talked to the Government about $1bn in funding if, and ‘if’ being the key word here, it couldn’t refinance the RCF it had with JP Morgan.

In addition, that Government funding would’ve only kicked in after another 18 months of building work at the mine and a further $2bn being invested. The Government went away, mulled it over, and then said no. This has also failed to reassure investors.

WHAT HAPPENS NEXT?

Sirius will take up to six months to conduct a strategic review, looking at all available options.

In the meantime, work at the mine will slow down because the company doesn’t have the cash to continue at the current pace.

Sirius says one way forward could be bringing in a strategic partner. This could potentially be a large corporate in the same or a similar sector who takes up a large stake in a company in exchange for upfront cash.

They would invest for strategic reasons instead of purely to make a return on that specific investment. They use their expertise to help the company grow, and if it’s a success, then it’s easier for them to acquire all of the company later on.

Sirius says it previously identified strategic partners as a way to bring cash into the project and support its case to get investment banks to lend it money, and now intends to look at this again.

However history suggests that finding a strategic partner in mining is often harder than companies think, so that option is by no means a certainty.

SHARES’ VIEW

We have to hold our hands up and admit we got it wrong on this occasion. We highlighted Sirius on 1 August as being an attractive stock to buy following recent price weakness.

At the time commentary from analysts implied there was no reason to doubt the bond issuance and that Sirius’ shares had the potential to soar once the financing was done.

Arguably we failed to properly take into account the company’s history in trying to raise finance, as well as the clear risks in the sector and investors’ appetite towards miners that aren’t generating any revenue at present.

Let this be a reminder of the very high risks of investing in the mining industry, even in the UK, as well as the big risks of investing in any company attempting to clear a major financial hurdle.

Anyone still holding the shares should know there’s no guarantee of a positive solution – and six months is a very long time to wait for news from a market perspective.

Our view is that the risks are now so high for the company given the scale of the necessary funding requirement that it is best to sell the shares and claw back any money you can, rather than risk everything by clinging on in hope.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.