Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

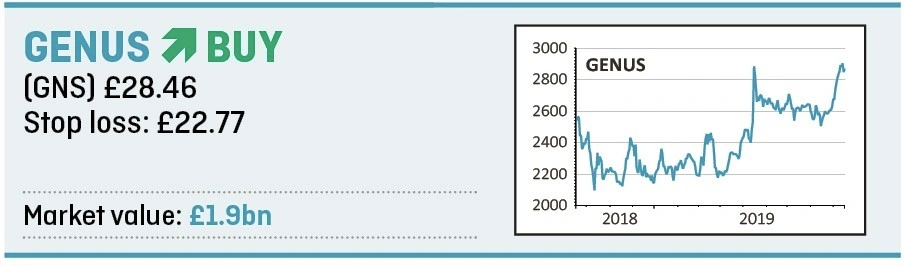

magazineDiscover the reason Genus shares are worth buying right now

Genus (GNS) provides farmers with superior genetics that enables them to produce higher quality animal protein more efficiently and sustainably.

The business serves over 50,000 customers in over 70 countries and employs almost 2,700 people, which includes over 100 who are PhD qualified.

An opportunity to exploit Chinese restocking of its pig herd represents a big source of potential upside and while the valuation isn’t cheap, at more than 30 times forecast earnings, patient investors should be rewarded with higher profits over the next few years.

AFRICAN SWINE FEVER PRESENTS UNIQUE OPPORTUNITY

China has historically produced and consumed over 50% of the world’s pork, but since the outbreak of African Swine Fever (ASF) the herd is expected to be culled by 50% in 2019 and production is expected to fall by up to 40% by 2020.

Genus reckons that this equates to around 15m tonnes of lost pork production, more than the entire global pork trade in 2018.

The production gap presents a unique opportunity for all animal protein sectors and will impact pork, beef and poultry for years.

Chinese officials have indicated that up to 80% of producers, primarily smaller ones, will ultimately not repopulate their herds, driving the industry towards larger scale, vertically integrated production.

Reduced supply has caused prices to rise to record highs in China, up nearly 80% since August 2018. From 2020 the remaining, larger, deep-pocketed farmers will be incentivised to restock herds.

This presents a significant opportunity for Genus to sell its genetics to build a higher yielding herd. The company wants to double capacity over the next two years.

Genus has historically spent heavily on research and development (R&D), and 2019 was no exception, up 13% to £54.7m, representing around 11% of revenue. A key strategic focus is to strengthen its proprietary differentiated offerings. This has transformed the business, such that management now describes itself as an agro-biotech specialist.

The continued spend on R&D has kept the company at the forefront of science and created valuable new revenue streams, while also keeping the competition at bay. For example royalty revenues increased by 7% in 2019, and total over £100m, representing around a fifth of total sales.

Another result of the company’s R&D efforts is the fast growing genetics product Sexcel, which saw volumes grow by 42% in 2019. Sexcel is unique in that it guarantees at least a 90% chance of producing female calves.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.