Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineHow retailer Next is radically transforming its business

Leicester-based Next (NXT) has navigated through the tough retail environment by radically changing the shape of its business while maintaining a disciplined financial performance. The company has indicated that it expects more of the same over the

next decade.

Rather like a swan gracefully gliding on top of the water masking the frantic paddling going on beneath the surface, Next has presented a surprisingly smooth profit trajectory over the last 10 years, despite lots of change going on behind the scenes.

The company has navigated the move to online with relative ease because it had an existing mail order catalogue which it has migrated into a full online offering.

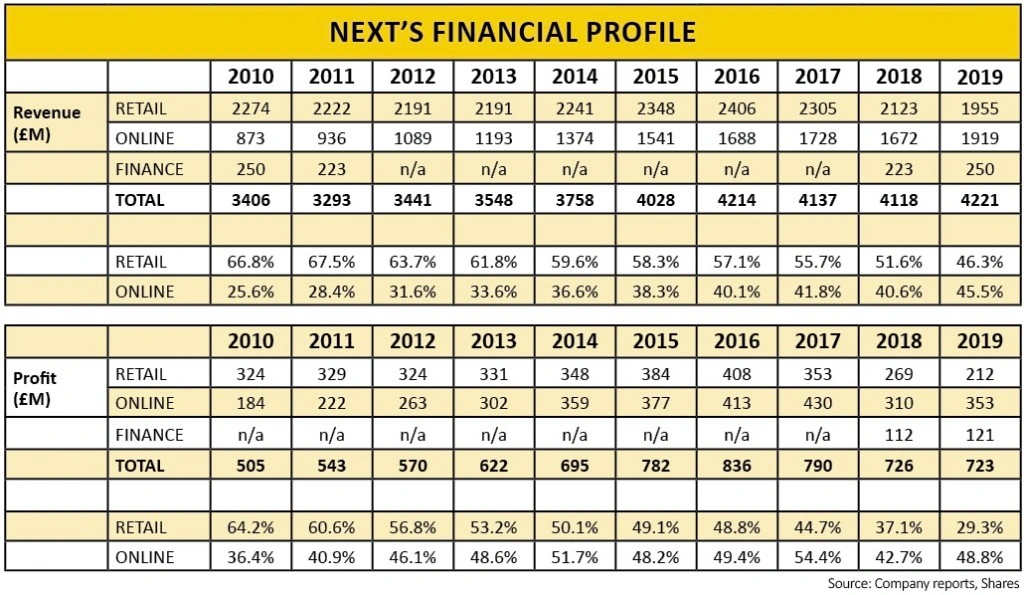

Online revenue has increased from 25% of group sales in 2010 to 45% today, while the land-based stores have seen their share fall from almost two-thirds to 46% over the same period.

The trend at the pre-tax profit level has been even starker, with online profit now dwarfing earnings made from the physical stores, representing 49% of total profit compared with 29% in 2010. That isn’t to imply that profit has suffered, it has grown at 4% a year over the last nine years.

Next has purchased and cancelled 37% of the shares outstanding over the last nine years which has had a very positive effect on earnings per share growth, with a compound annual growth rate (CAGR) of close to 10%.

The eagle-eyed reader will have noticed that adding up the online and physical stores’ share of revenue falls well short of 100%, and that is because Next has been developing other profit streams in recent years.

THE NEW SHAPE OF THE GROUP

Not only has the company moved more business online, it has also increased the proportion of business done overseas and developed from a single brand to a full multi-brand offering.

Today, 10% of Next’s revenue comes from selling third party brands, 9% of revenue is generated outside the UK and 6% comes from selling credit to customers.

The financing arm earns more profit than its size suggests, although with over £1bn of credit to its customers, it isn’t small either. Profit after financing costs represents 17% of the company’s total profit.

Although lots of high street firms have been suffering from the move to online and onerous rents, Next sees its stores as an asset to be optimised rather than a millstone around its corporate neck.

Of the 45% of online orders, half are delivered to a Next store for free collection as opposed to delivering to a customers’ home, which incurs a £3.99 charge. It can be more convenient as well as cheaper to collect from an existing store and these orders represent around a third of all orders by volume.

Shops are even more important in facilitating online returns, with over 80% of all returns going through them.

At the same time the company has been renegotiating more competitive rents when they come up for renewal. In 2018 it saw a 29% reduction on the leases that it decided to renew.

The average lease term is around six years. Management have conducted an in-house study to glimpse at the future and they believe that in 15 years’ time there will be fewer stores and much lower rent.

The way that management looks at the industry, it’s not a question of how much physical space they need, it’s a question of reducing rent and rates so that an adequate return can be made from each store.

AGGREGATION PLATFORM

The internet has drastically lowered barriers to entry in the retail industry. Challenger firms like Sosandar (SOS:AIM) do not need to own any stores, warehouses or distribution networks to launch and develop their brand.

Seeing opportunity rather than threat, Next is leveraging its assets to build an aggregation platform by offering clients access to its 8m square feet of mechanised warehousing with its capability of handling flat-packed, hanging, palletised and furniture items.

In addition to offering a flexible distribution infrastructure, the company can offer third parties other services such as digital marketing, access to 4m UK customers, finance and credit services as well as access to 1.3m overseas customers.

LABEL is the company’s third party business and it makes over £400m of revenue and delivers £66m of profit. Management are consciously taking a long-term view in developing this business, implicitly accepting that in the brave new internet world, power lies with originators of products who can choose their route to market.

LABEL grew its revenue by 29% last year and its partners now include All Saints and River Island. Over the last five years the compound annual growth rate of sales has been close to 30% per year.

Half of the third party branded sales is sold on a commission basis, which has lower margins, but encourages its partners to generate higher revenue growth. The next step is to offer third party brands that are only available in partners’ own warehouses.

OVERSEAS STRATEGY

In overseas markets Next is a challenger brand and offers its whole UK range at similar prices to the home market.

It benefits from low barriers to entry, allowing Next to expand quickly and efficiently through third party platforms. The online overseas business generates £360m of sales and delivers £59m of profit per year.

Overseas revenue has grown at a 23% CAGR over the last three years, while the customer base has increased by 25% over the past 12 months to 1.3m.

THE FINANCING ARM

Next has been advancing credit to customers for a number of years and today the activity represents a significant 17% slice of the company’s total profit.

In the year to 31 January 2019, the average value of outstanding debtors was £1.14bn which generated £250m of interest income and £121.2m of net profit.

This is a very credible result and management estimates that the business earns a 10% to 11% return on capital.

Bad debts ran as high as 8.5% of average debtors back in 2010 but have only averaged 3.6% in the past five years. At the same time the number of active customers has been on a positive trend since 2016.

Recently the company introduced next3step, which allows customers to spread payment over three months. It is currently recruiting 2,000 new customers a week.

Nextpay app allows credit customers to pay for goods in the retail stores the same way as a physical payment card and has been downloaded over 1,400 times a week, mainly by existing customers.

OTHER BUSINESSES

The company has franchise partners that operate in 32 countries through 199 stores, and which generate £52.2m of income, most of which is pure profit. Next also directly owns six stores in Czech Republic, Slovakia and Sweden which generate £10m of revenue a year.

Lipsy is a wholly owned subsidiary with its own independent management team, based in London. It sells product through a number of different channels, including Next online and retail. Although small, the unit grew its operating profit to £11m last year, an increase of 129%. Management forecasts an increase of 40% in the current year.

ACCELERATING CHANGE, MORE TO COME

Helpfully Next’s management provide what they call their 15-year stress test, which attempts to outline the future shape of the business. The company assumes that the physical stores will continue to see 10% like-for-like sales decline a year and that wages will fall at the same pace.

Rents are assumed to fall by 5% a year after 2022, and the company has also assumed it will keep some of the loss-making stores so that they can continue to facilitate the collection of online orders and returns.

Next online is projected to grow by a CAGR of 4.8%, while UK LABEL is expected to grow at a CAGR of 8.4% and overseas is expected to grow at a CAGR of 12.2%. The finance arm is expected to grow at a CAGR of 4.7%.

If the projections work out as planned the online business will be generating almost £4bn of revenue, while the number of stores will fall from 509 to 270 across the UK.

The third party LABEL business will almost be as big as the current Next retail business and the revenue from overseas will be close to £2bn, larger than the online revenue generated in the UK today.

As management points out, it’s highly likely that many of the assumptions about sales and costs will prove to be incorrect.

Nevertheless, the exercise demonstrates that a radical restructuring of the company’s cost base is possible over time, while continuing to produce significant cash flow. The company expects the business to generate an additional £12bn of cash over the next 15 years.

SHARES SAYS: Next is one of our top picks for 2019 and we rate it as one of the best stocks to own on the London market.

At £61.34 it trades on 13 times forecast earnings for the year ending January 2021. It is forecast to pay 175.07p in dividends that financial year, meaning the shares offer a 2.9% prospective yield.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.