Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineBritish stocks ripe for a foreign takeover

Last year was a vintage one for mergers and acquisitions (M&A) with deals totalling more than $4trn, the highest figure since 2007 and the onset of the global financial crisis. This year is shaping up to also be a historic period for takeovers and we believe UK-listed companies are prime targets for foreign companies.

In 2018 mega deals worth $10bn or more grabbed the headlines. According to the MAN Institute, 30 transactions were announced in the first half of the year alone while mid-sized deals between $1bn and $5bn accounted for more than half of all transactions.

The low cost of debt, improving cash flows, high levels of cash both on corporate balance sheets and at private equity firms (which raised record amounts of funding in 2017), and a favourable tax regime in the US were all big factors.

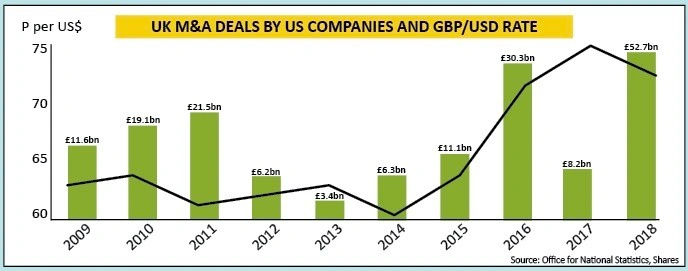

M&A activity in the UK hit a record last year with more than 600 deals involving foreign companies buying UK companies according to figures from the Office for National Statistics.

Of a total of £78.8bn of foreign investment, £52.7bn or two thirds came from the US, while £17.8bn or just under a quarter came from Europe.

Domestic M&A hit an all-time record last year with 960 deals done worth a total of £27.7bn.

Ten major UK M&A deals struck in the first half of 2019

Marsh & McLennan (US) buying JLT for £4.6bn

Berry Global (US) buying RPC for £3.3bn

Vinci (FR) buying majority stake in Gatwick airport for £2.9bn

City Developments (Singapore) buying the rest of Millennium & Copthorne it didn’t already own for £2.2bn

TDR Capital (UK) buying BCA Marketplace for £1.9bn

Saputo (Canada) buying Dairy Crest for £975m

Charter Court (UK) buying One Savings Bank for £800m

Macquarie Infrastucture (Australia) buying Kcom for £627m

Roper (US) buying Foundry for £451m

Asahi (Japan) buying a division of Fuller, Smith & Turner for £250m

OPTIMUM CONDITIONS FOR UK M&A

Conditions in the UK stock market are currently ideal for more corporate M&A activity.

The continued weakness of sterling makes UK assets relatively more attractive for foreign buyers as their purchasing power is increased.

Meanwhile UK companies have high levels of cash on their balance sheets, interest rates are still low should suitors want to borrow to do a deal, and valuations are low thanks to political uncertainty.

Most of this year’s domestic M&A has been small deals as companies look to bolt on small acquisitions to make up for lack of organic growth. Therefore although the number of transactions in the first half hit 460, the total amount spent was just £4.6bn.

Finally non-trade buyers like private equity firms have huge amounts of ‘dry powder’ in the form of funding for deals. According to research by financial data group Prequin, the amount of unspent cash available to private equity firms is close to $2.5trn, of which roughly a third was raised last year.

An interesting feature of last year’s M&A bonanza was the domino effect where one mega deal lead to another. For example, Barrick’s merger with Randgold, which created the world’s largest gold producer, spurred rival Newmont to bid for Goldcorp and reclaim the title shortly afterwards.

GLOBAL EARNINGS GOING CHEAP

It’s standard practice nowadays for managers of UK funds to flag up the fact that many FTSE 100 stocks are global players, with substantial overseas earnings, yet they are trading at a discount to their overseas rivals because they are quoted in sterling.

A case in point is British American Tobacco (BATS), the seventh-largest stock on London’s Main Market, which makes more than 90% of its sales outside the UK yet trades on just nine times this year’s forecast earnings.

By contrast US rivals Philip Morris and Altria – who also sell tobacco products worldwide – are trading on 14 times and 12 times this year’s earnings respectively.

While selling tobacco may not be a great business, which is one reason why we haven’t included British American Tobacco on our M&A target list, it’s probably fair to say that at least part of the ‘valuation gap’ is down to the stock being London-listed.

On the other hand AstraZeneca (AZN) generates more than 90% of its revenue outside of the UK, and it reports in US dollars, but it trades on 25 times current-year forecast earnings according to Sharepad, while US rival Pfizer trades on 15-times and Switzerland’s Roche trades on 16-times.

Selling prescription drugs is undoubtedly a better business than selling tobacco, hence AstraZeneca has better revenue growth and better operating margins than British American Tobacco, but the shares could hardly be said to be trading at a discount either to their historic valuations or to those of their peers regardless of the level of the pound.

Major UK deals recently announced

Cobham (£4bn, buyer Advent, US private equity)

EI Group (£1.3bn, TDR Capital, UK private equity)

Entertainment One (£3.3bn, Hasbro, US industrial)

Greene King (£2.7bn, CKA, Hong Kong property investor)

Just Eat (£5bn, Takeaway.com, Dutch fast-food rival)

Merlin (£4.8bn, Kirkbi, Danish Lego owner)

FOR A FEW DOLLARS (OR EUROS) MORE

Moves in the exchange rate can make a big difference for corporate buyers in terms of their appetite for M&A. The sharp drop in sterling following the 2016 Brexit vote spurred a huge influx of M&A spending as the buying power of every dollar and euro was suddenly boosted.

If a company can move in and scoop up a rival or complementary business at a low price and then see a benefit as the target company rises in value in tandem with the currency it’s a win-win situation.

So any investor seeking stocks to buy as potential takeover targets, the goal is to find solid businesses with at least three quarters of their sales overseas, which thanks to the weakness of sterling or a short-term hiccup in trading are sitting at relatively attractive valuations for trade or financial buyers.

However, given the amount of money already chasing these kind of companies and the number which have already been snapped up, compiling the list isn’t easy.

WHICH COMPANIES ARE FLOATING OUR BOAT?

Rather than just looking for companies which look cheap, we have screened the FTSE 350 for what we consider to be good companies which are either cheap due to the weak pound, or are trading at depressed levels due to temporary factors like a cyclical downturn or a company-specific problem which can be solved without too much drama.

We have also identified a group of companies which look cheap relative to the value of their assets and which could appeal to non-trade buyers looking for a purely financial return over the medium term.

A couple are turnaround stories and some have net cash on their balance sheets – which makes them even cheaper for a buyer as they can pocket the money.

The FTSE 250 performance looks a lot different in dollar terms

Performance since start of 2016:

In sterling: +11.7%

In dollars: -8.4%

About half of the FTSE 250 index contains UK-focused companies. The data shows that the index has become 8.4% cheaper in dollar terms, raising the prospect of good firms being taken over by foreign entities.

FIVE TAKEOVER TARGETS TO BUY NOW

AGGREKO 790.4p

Market value: £2bn/$2.5bn

Net debt: £784m/$964m

Power-equipment rental firm Aggreko (AGK) is a truly global operation, doing business in weird and wonderful places across the globe from Bangladesh to Burkina Faso.

Its core business is providing power where it’s needed, when it’s needed, to keep the lights on. It has large exposure to the US, especially the energy sector, and is always busy during hurricane season when traditional power sources are knocked out.

In its heyday it enjoyed returns on capital employed (ROCE) of over 20%. Today returns are more like 10%, but thanks to cost-cutting and a dwindling proportion of sales to the utility sector – which is low-margin and where some of its customers are cash-strapped – it is targeting a mid-teens ROCE in 2020.

The balance sheet is better than it was, although net debt is close to £800m, and it is a capital-intensive business with new projects typically requiring an upfront investment.

It has invested heavily in more eco-friendly equipment, and the trend towards greener energy in emerging markets, where there is large structural power deficit, means there is still significant growth potential.

This looks like a classic takeover target for a foreign entity – a solid business going cheap.

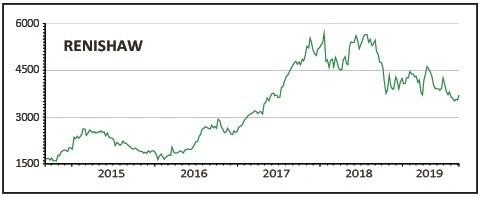

RENISHAW £36.64

Market value: £2.6bn/$3.2bn

Net cash: £105m/$130m

Precision-measurement manufacturer Renishaw (RSW) earns 95% of its revenue outside the UK, operating across 81 locations in 36 countries.

Its tools are used in a range of industries from electronics and healthcare to transport, contributing to the development of products from smart phones to dental implants and jet engines.

Headwinds in the Asia-Pacific region (43% of sales), especially smart phones, led to a profit warning in late March since when the company has lost over 10% of its market value.

Renishaw has been through similar ‘bumps in the road’ before and the quality of the business usually shines through. Return on capital employed is currently 15% but has averaged more than 20% over the last five years.

The weakness of sterling means that a US buyer could acquire the company for 50% below the peak price seen in January 2018. Meanwhile earnings per share are slated to grow by 11% and 15% for the next two years according to analyst forecasts compiled by Reuters.

The firm is majority-owned by its two founders, both in their late 70’s with no family members involved in the senior management, so a bid at the right level could succeed.

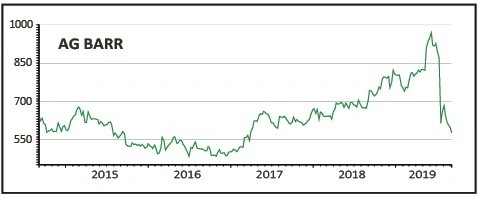

A.G. BARR 570.3p

Market value: £650m/$800m

Net cash: £22m/$27m

Shares in Scotland-headquartered soft drinks group A.G. Barr (BAG) have fallen by a third since a mid-July profit warning, leaving the maker of iconic tipple IRN-BRU, Strathmore, Rubicon and cocktail mixers name Funkin looking vulnerable to a takeover bid.

Beverages industry watchers may recall that a £1.8bn merger with rival Britvic (BVIC) was announced in 2012, but the deal fell apart a year later.

The key takeaway is that big-time consolidation can happen in this sector and a bid for A.G. Barr is not beyond the realms of possibility given the current weak share price.

This is a business that could well be on the watch list of overseas acquirers with a liking for quality.

A.G. Barr’s shares lost their fizz following a punishing earnings alert this summer, which was blamed on a strategy shift from a heavy focus on driving volume last year to prioritising value now.

Also at play were disappointing spring and early summer weather, most notably in Scotland and the north of England, and short-term challenges around its Rockstar energy and Rubicon juice drinks.

Yet Shares remains bullish on the long-term earnings potential of A.G. Barr, whose competitive advantage lies in a portfolio of differentiated soft drinks brands, well-invested manufacturing assets and strong cash generation, the latter enabling the company to fund a progressive dividend and supportive share buybacks.

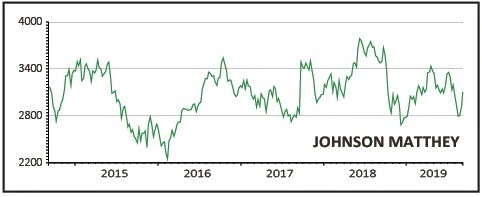

JOHNSON MATTHEY £30.78

Market value: £6bn/$7.4bn

Net debt: £866m/$1.1bn

Investors have a love-hate relationship with catalytic converter-supplier Johnson Matthey (JMAT), piling into the stock when it’s in vogue and piling out when it fails to meet expectations.

Right now sentiment is at a low ebb after the company disappointed the market with its full-year results in May despite a big increase in revenue and earnings.

The big story isn’t so much catalysts any more as the New Markets division which is working on a new type of battery technology for electric vehicles.

ELNO, or enhanced lithium nickel-oxide, could transform the firm’s fortunes if it can get it into commercial production and ready for the market by 2022 as planned.

Sales of electric vehicles are estimated to hit over $550bn by 2025 compared with $55bn this year which means the opportunity set is huge.

The July trading update said that this year’s results will be ‘second half-weighted’, which didn’t go down well with investors, but given the ups and downs of the last five years and the current rating of 13 times earnings it’s hard to see the shares falling much further.

For a car-maker seeking next-generation battery technology, or even a rival supplier, Johnson Matthey looks ripe for the taking.

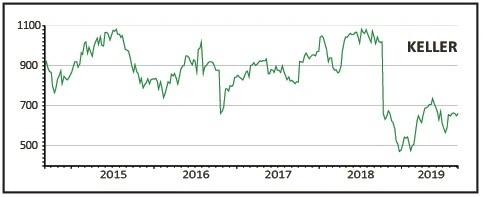

KELLER 665.76p

Market value: £475m/$585m

Net debt: £420m/$517m

Ground works engineering specialist Keller Group (KLR) is the world’s largest player in a fragmented market, with around a 5% of the share. It operates in over 40 countries through 22 business units, and generates only 3% of its revenue from the UK.

Just over half of group revenue comes from the US market, another third from Europe, and the rest from Asia. Late last year the company saw its shares crash 30% on news that it was reviewing its Asian business, citing deteriorating conditions, notably in Malaysia.

The company decided to start restructuring the troubled Asian business as well as the reorganising the US business, integrating seven individually branded businesses into one Keller brand.

The underlying drivers of the business, growing urbanisation and infrastructure spending, continues to provide growth opportunities for the group.

At the first half results reported on 29 July, the company reported an increased momentum during the second quarter, offsetting the weak start to the year.

For the full year Keller expects revenue to be broadly flat and an improvement in margin to drive growth in profits.

Current analyst expectations pencil in 12% growth in operating profit to £108.4m and 15% growth in earnings per share to 91.12p.

Keller ticks the box on several levels in terms of our search for potential takeover targets. It earns a lot of earnings overseas, which are more attractive due to the weakness of sterling and the company suffered a one-off earnings hiccup, cheapening the shares further.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.